Link para o artigo original:https://www.oaktreecapital.com/insights/insight-commentary/market-commentary/the-roundup-top-takeaways-from-oaktrees-quarterly-letters-december-2023-edition

In 2023, credit markets have experienced dramatic swings in investor sentiment, unexpected geopolitical events, and the second consecutive year of rising interest rates. In the current installment of The Roundup,1 Oaktree experts consider where opportunities and risks are emerging in various asset classes and what normal may mean in this unsettled environment.

1

Market Outlook:

What’s Normal?

Howard Marks

Co-Chairman

When thinking about interest rates and inflation, it’s useful to ask, “What’s normal?” During the period from 2009-20, “normal” for central banks was wanting something that was just out of reach. In that period, most central banks wanted 2% inflation, but they struggled to get it. Try as they might – with interest rates near zero (or, in some countries, below zero) – they just couldn’t keep inflation at that level.

As we know, inflation in many countries surged well above 2% in 2021 and 2022. The Federal Reserve first said this spike was abnormal and would therefore be “transitory,” but central bankers eventually had to give up on that position. They then began to hike interest rates aggressively to bring down inflation. This certainly seems to be working. But it’s important to remember that inflation is mysterious, unpredictable, and challenging to manage.

What does this mean for investors in 2024? I’ve long said I don’t put much stock in macro forecasts – especially my own – but let’s assume that inflation does come down near the Fed’s 2% target and stays there for a while. Does that mean we’ll return to a pre-pandemic world with interest rates near zero?

I’d say “no.” Interest rates don’t decline just because they’re not being raised, so returning to 2% inflation doesn’t necessarily mean a significant interest rate cut is imminent. Additionally, a return to consistent sub-2% inflation seems unlikely, especially given trends like slowing globalization and rising union influence. Finally, the current level of interest rates is much closer to the long-term historical average than what most investors working today are used to. I imagine when inflation has been fully conquered, rates will be lower than they are today, but not back near zero.

Considering all this, what are my expectations for the investment environment in 2024 and beyond? I’ll repeat what I wrote last December in Sea Change:

… if you grant that the environment is and may continue to be very different from what it was over the last 13 years – and most of the last 40 years – it should follow that the investment strategies that worked best over those periods may not be the ones that outperform in the years ahead.

2

Liquid Credit:

Recession 2.0

While the U.S. economy has proven to be more resilient than many anticipated, growth could slow in the coming year, given that the fed funds rate is above 5%, excess savings are dwindling, and inflation still exceeds the Fed’s target. But even if these trends do push the U.S. economy into a recession, we expect that the impact on leveraged credit markets will be different from what we’ve seen in the past.

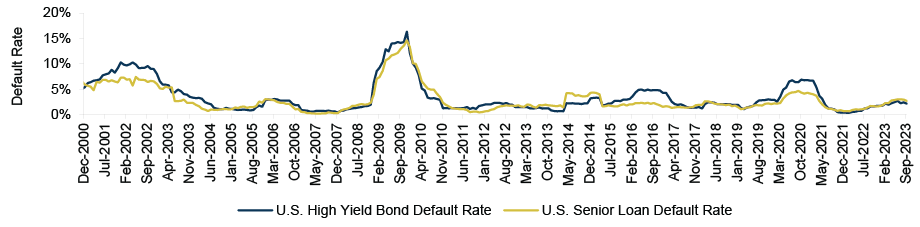

First, we think default rates for liquid credit are unlikely to hit the double-digit levels seen in many previous recessions. One reason is that defaults in both the leveraged loan and high yield bond markets rose during the pandemic to roughly 4.0% and 6.5%, respectively.2 (See Figure 1.) Thus, defaults were likely “pulled forward,” meaning many companies that had particularly weak fundamentals going into the pandemic have already defaulted. This trend is especially relevant in the high yield bond market.

If this recession does arrive, it will be one of the most well telegraphed in history. This head start could help to limit defaults, as companies will have had more time than usual to engage in proactive cost reduction programs. For example, many highly levered companies have already begun to reduce capex and advertising spending to free up cash for debt service. While growth may be impaired if companies are forced to redirect cash away from value-creating initiatives, this is an equity problem, not a debt problem.

Next, we expect that the leveraged loan market will record a higher default rate than the high yield bond market – an uncommon occurrence historically. Borrowers in the loan market are more likely to have both floating-rate coupons and deteriorating fundamentals. Additionally, we anticipate that recovery values in the loan market over this cycle will be well below the long-term historical average of 65%, due to the elimination or weakening of loan covenants in prior years and the growing prevalence of loan-only borrowers.3

Finally, even if default rates remain well below their recessionary averages, the total dollar amount of defaulted debt may be higher than in previous recessions given that the global supply of potential distressed debt has more than quadrupled since the Global Financial Crisis.4 Therefore, we believe opportunistic investors will likely have an expansive investment universe, even if default rates remain in the mid-single digits.

In short, leveraged credit markets have evolved. Moving forward, we believe the most successful investors will be those with the flexibility, dynamism, and skill to keep up.

Figure 1: Elevated Default Rates in 2020 May Have “Pulled Forward” Defaults

Source: Par-weighted trailing-12-month default rates based on JP Morgan Research, as of September 30, 2023; including distressed exchanges

3

CLO Equity:

Cash Cow

While the prospective returns of CLO equity – the unrated junior tranche of a collateralized loan obligation – are comparable to those of private equity or private debt, the liquidity profiles are quite different. Investors in private instruments typically have to wait 5-7 years before receiving distributions, but CLO equity generates cash immediately and provides quarterly distributions.

This benefit may be especially valuable today. Many institutional investors with allocations to private equity are receiving fewer distributions than they expected, as restrictive capital markets have made it challenging for private equity investors to exit at acceptable valuations. We anticipate that this trend will persist given the increased likelihood of higher-for-longer interest rates, as they’re liable to continue having a dampening effect on capital markets activity.

Of course, a CLO equity investor could see distributions decline if the CLO fails to meet certain tests – and the manager fails to correct the issue – or if the underlying loan portfolio suffers defaults or losses. And default rates in the leveraged loan market could reach 4% in the U.S. and Europe in 2024, according to Fitch Ratings.5

However, this would mean that 96% of all leveraged loans would be performing, i.e., servicing their debt and paying off their maturities in full and on time. Moreover, default forecasts for the entire loan market shouldn’t be confused with the likelihood that specific managers will experience defaults and losses.

It’s also notable that the dramatic nature of the recent interest rate spike – more than 500 basis points in roughly 1.5 years – has made the vulnerabilities among many overleveraged companies readily apparent. That means skilled CLO managers creating portfolios today should be able to easily avoid these ailing credits while benefiting from the negative sentiment that is weighing down the prices of loans taken out by companies with stronger fundamentals.

CLO equity investors can therefore potentially earn an attractive cash-on-cash return while waiting for loan markets to return to par. At a time when liquidity is being squeezed, we believe the benefit of this cash component isn’t just large – it’s king-sized.

4

High Yield Bonds:

High Conviction

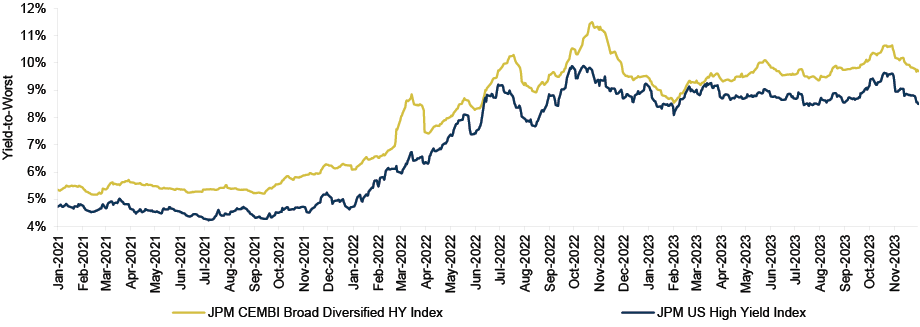

High yield bond investors are currently able to earn yields above 8.0% at a time when credit fundamentals in the asset class are solid and the Federal Reserve appears to be near the end of its interest-rate-hiking cycle. Thus, we believe the arguments in favor of high yield bonds are becoming increasingly more persuasive.

Consider how much the U.S. high yield bond market has changed since the end of 2021. At that time, the average yield on B-rated bonds was just 4.7% versus 8.7% as of November 30, 2023.6 With the yield in the asset class approximately 200 bps above the ten-year average, investors now have the opportunity to earn attractive returns on a contractual basis.7

Importantly, while yields have moved up, we haven’t seen a comparable decline in credit quality in high yield bonds. In fact, roughly half of the market is currently rated BB (the level just below investment grade), which is near a ten-year high.8 Some fundamentals in the asset class have declined modestly in recent months, but the average debt-to-EBITDA ratio of 4.0x remains below the long-term historical average, and the average interest coverage ratio is still elevated at around 5.0x.9

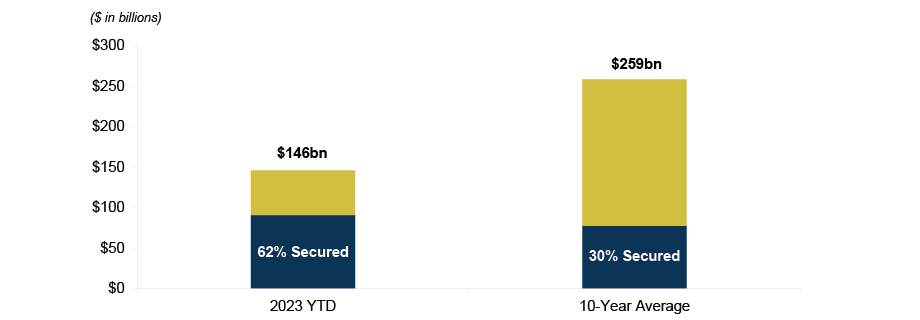

Moreover, even though the pace of new issuance has been sluggish in recent quarters, average quality has been strong, as relatively few lower-rated deals have come to market. We’ve also seen an unusually high percentage of secured bonds, which provide more downside protection in the event of a restructuring compared to unsecured notes. (See Figure 2.)

Finally, while investors have flocked to floating-rate instruments in recent years due to concerns about rising interest rates, we believe this preference may shift if it becomes clear that interest rates are unlikely to continue climbing. So even though the jury may be out on exactly what will happen in the macro environment, we believe the case for investing in high yield bonds keeps getting stronger.

Figure 2: Secured Bonds Represent Almost Two-Thirds of 2023 U.S. High Yield Bond New Issuance

Source: JP Morgan, as of October 31, 2023

5

European Real Estate:

Mind the Gap

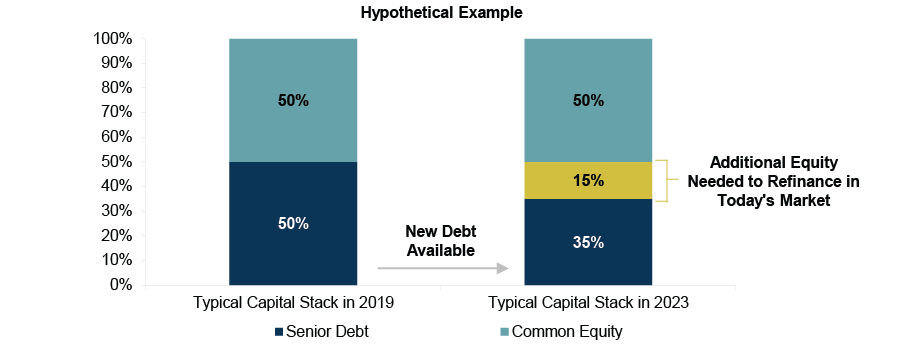

The European real estate market is facing an expansive debt funding gap, due to a looming maturity wall, declining valuations, and European banks’ unwillingness to increase their exposure to the asset class. We believe this situation will create attractive opportunities for alternative providers of capital and potentially transform the European real estate financing market.

Over $500 billion of real estate debt is due to mature between 2023 and 2025 across the UK, France, and Germany.10 Much of this debt will require refinancing. However, few traditional lenders are willing to provide funding at levels sufficient to meet this need, primarily because of rising interest rates, declining real estate valuations, and deteriorating interest coverage ratios in existing real estate portfolios.

In short, the risk calculus has changed for many lenders. We estimate that the average loan-to-value ratio across the European real estate market was near 50% in 2019 and the all-in cost of debt was roughly 3.0%.11 Since then, the all-in cost of debt has more than doubled to around 7.5%. Due to this and other sectoral challenges, we believe that today’s lenders will be willing to lend at only 35% of 2019 acquisition valuations. This results in a roughly 15% debt funding gap – or to put it in dollar terms, a gap of approximately $155 billion between 2023 and 2025 across the UK, France, and Germany. (See Figure 3.)

Concerns about refinancing risk are magnified in Europe because it has far less access to the residential mortgage-backed securities and commercial mortgage-backed securities markets than its U.S. counterpart. The European real estate market has historically relied almost entirely on bank debt, making it more vulnerable when banks rein in lending.

With traditional lenders sidelined, we expect private credit will be called upon to fill the liquidity gap in Europe. These investors will have the potential to generate attractive risk-adjusted returns while also gaining market share in an arena long dominated by one class of lenders. Thus, this gap is one everyone should keep an eye on.

Figure 3: Rising Borrowing Costs Have Created a Significant Funding Gap in European Real Estate

Source: Hypothetical example; based on Oaktree calculations and observations in the market, as of November 30, 2023

6

Life Sciences Lending:

It’s (Very Much) Alive

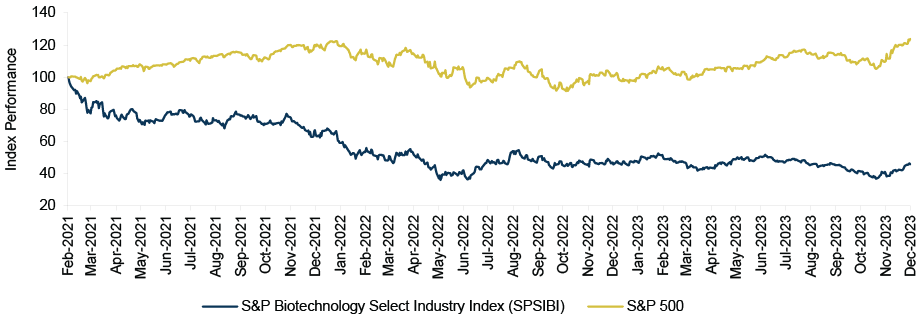

Biotech stocks are currently experiencing their third consecutive year of negative performance – the longest bear market in the industry’s history – with the S&P Biotechnology Select Industry Index (SPSIBI) down 55% from its peak in February 2021.12 (See Figure 4.) Consequently, over 230 stocks in the SPSIBI are currently trading at levels that leave the respective issuers with negative enterprise values – a new record.13 This public market weakness is creating attractive opportunities for providers of alternative financing – like private credit – and helping to bring the industry’s M&A market back to life.

Biotech valuations soared during the pandemic, but they’ve since come back to earth, due to (a) the reversal of some pandemic-era spending trends; (b) regulatory changes; and (c) rising interest rates, which have caused investors to eschew companies with limited free cash flow generation and elevated research and development needs. However, biotech companies still require significant financing, as they need to meet patient demand for existing products while also continuing to develop and commercialize new drugs and devices. Biotech firms are therefore seeking non-dilutive financing, such as private credit, at unprecedented levels.

These depressed valuations also appear to be helping rejuvenate the biotech M&A deal market. During the pandemic – when biotech valuations were at sky-high levels – life-sciences-focused private equity firms and large pharmaceutical companies mostly chose not to pursue M&A deals. But both groups have recently returned to the market with ample capital to deploy. Healthcare M&A deal volume has risen to roughly $180 billion in 2023, and nine of the last ten major transactions have been pursued by multiple parties, highlighting the growing appetite for biotech deals among sponsors.14 This is creating more demand for private debt financing, given the challenges borrowers are facing in public debt markets.

In 2024, we expect to see already-healthy investment pipelines expand for direct lenders with life sciences expertise, especially if the signs of life in the biotech deal market become even more pronounced.

Figure 4: Biotech Stocks Have Weakened Significantly Since 2021

Source: Bloomberg, as of December 8, 2023

7

Emerging Markets Debt:

Getting More for Less

Emerging markets debt prices have been volatile in 2023, while issuer fundamentals have remained fairly robust on average. EM debt markets have also become less competitive: net outflows from EM-dedicated retail funds since the beginning of 2022 have eclipsed $55 billion, and crossover investors have increasingly abandoned EM debt for developed market opportunities offering positive real yields.15 This has created an attractive opportunity for EM investors who target dislocated credits.

In the third quarter, the average EM high yield bond price fell to the lowest level since late 2022. The asset class has rallied since then, but the average price remains below 90 cents on the dollar, and average yields are near 10%.16

Importantly, the yield differential between EM and U.S. high yield bonds is wider than the historical average, even though the credit metrics of EM companies are generally stronger. (See Figure 5.) EM high yield bond issuers have an average net-debt-to-EBITDA ratio of 2.1x, nearly half that of their U.S. counterparts, and higher discretionary free cash flow.17

True, the EM default rate is expected to be 7% at the end of 2023, but nearly half of the defaulted debt has been in one area – the Chinese property sector18 – and, looking forward, EM defaults aren’t expected to reach the peaks seen in previous downcycles. Moreover, today’s offshore EM creditors typically have greater confidence that they’ll be able to enforce their claims and secure reasonable recoveries compared to investors in the past, as corporate dispute resolution has become more standardized in many EM countries in the last decade.

We believe this situation favors bottom-up, long-term investors who can withstand the volatility and take advantage of the attractive bargains on offer.

Figure 5: EM High Yield Bonds Continue to Offer a Yield Premium Vs. Their U.S. Counterparts

Source: JP Morgan, as of November 30, 2023

ENDNOTES

- 1The content is derived from or inspired by ideas in 3Q2023 letters or other materials sent to clients in 4Q2023; the text has been edited for space, updated, and expanded upon where appropriate.

- 2JP Morgan North America Credit Research. Par-weighted default rates as of December 31, 2020.

- 3JP Morgan North America Credit Research.

- 4Includes BBB-rated debt and below-investment-grade debt; Bloomberg, Credit Suisse, ICE BofA, Preqin, Cliffwater, as of March 31, 2023; for middle-market direct lending data: Preqin, as of June 2022.

- 5Fitch Ratings, as of October 2023.

- 6ICE BofA Single-B US High Yield Index.

- 7ICE BofA Single-B US High Yield Index, as of November 30, 2023.

- 8JP Morgan.

- 9JP Morgan. 3Q23 High Yield Credit Fundamentals. December 12, 2023.

- 10PGIM 2023 Global Outlook: Finding Value After the Great Reset, 2023.

- 11All statistics in this paragraph based on Oaktree calculations and observations in the market, as of November 30, 2023.

- 12As of December 8, 2023.

- 13CapitalIQ, as of November 3, 2023.

- 14JP Morgan, Bloomberg, Dealogic, FactSet, as of November 2023.

- 15JP Morgan, EPFR Global, Bloomberg Finance L.P.

- 16JP Morgan, Oaktree Capital Management, as of September 30, 2023. JP Morgan Corporate Broad CEMBI Diversified High Yield Index for all data referring to EM high yield bonds in this section unless otherwise specified. The emerging markets debt section focuses on dollar-denominated debt issued by companies in emerging market countries, as of October 31, 2023.

- 17JP Morgan.

- 18JP Morgan, excluding Russian bonds as these bonds are no longer in the investable universe.

NOTES AND DISCLAIMERS

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2023 Oaktree Capital Management, L.P.

Informações sensíveis e divulgação

Este memorando expressa as opiniões do autor na data indicada e tais opiniões estão sujeitas a alterações sem aviso prévio. A Oaktree não tem a obrigação de atualizar as informações aqui contidas. Além disso, a Oaktree não faz nenhuma representação, e não se deve assumir que o desempenho dos investimentos passados é uma indicação de resultados futuros. Além disso, onde quer que haja potencial de lucro, também existe a possibilidade de prejuízo. Este memorando está sendo disponibilizado apenas para fins educacionais e não deve ser usado para qualquer outro propósito. As informações contidas neste documento não constituem e não devem ser interpretadas como uma oferta de serviços de consultoria ou uma oferta de venda ou solicitação de compra de quaisquer títulos ou instrumentos financeiros relacionados, em qualquer jurisdição. Certas informações contidas neste documento sobre tendências econômicas e desempenho são baseadas ou derivadas de informações fornecidas por fontes terceirizadas independentes. A Oaktree Capital Management, L.P. (“Oaktree”) acredita que as fontes das quais tais informações foram obtidas são confiáveis; no entanto, não pode garantir a exatidão de tais informações e não verificou de forma independente a exatidão ou integridade de tais informações ou as suposições nas quais tais informações se baseiam. Este memorando, incluindo as informações aqui contidas, não pode ser copiado, reproduzido, republicado ou postado na íntegra ou parcialmente, em qualquer formato, sem o consentimento prévio, por escrito, da Oaktree.