Link para o artigo original:https://www.lordabbett.com/en-us/financial-advisor/insights/investment-objectives/the-case-for-credit–part-3–a-history-of-excess-returns.html

The Case for Credit, Part 3: A History of Excess Returns

By

By

Read on for the details, but in summary we find:

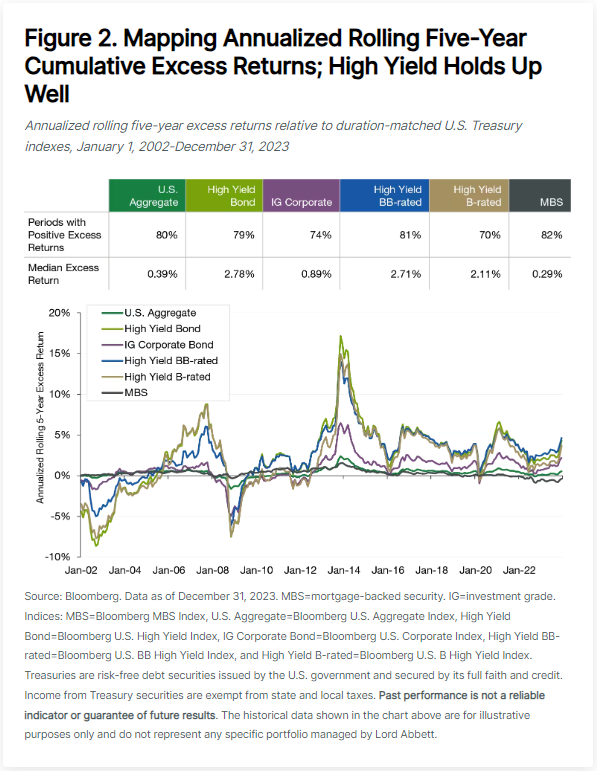

- Corporate credit’s cumulative excess return over time makes a powerful statement for the benefits of this asset class compared to a U.S. Aggregate Index benchmark approach. And more credit exposure has historically been better: the median annualized excess return of high yield at 278 basis points (bps) dominates investment grade at 89 bps.

- The consistency of these benefits is also surprising. Over rolling five-year periods, non-Treasury fixed income has experienced positive excess returns close to 80% of the time.

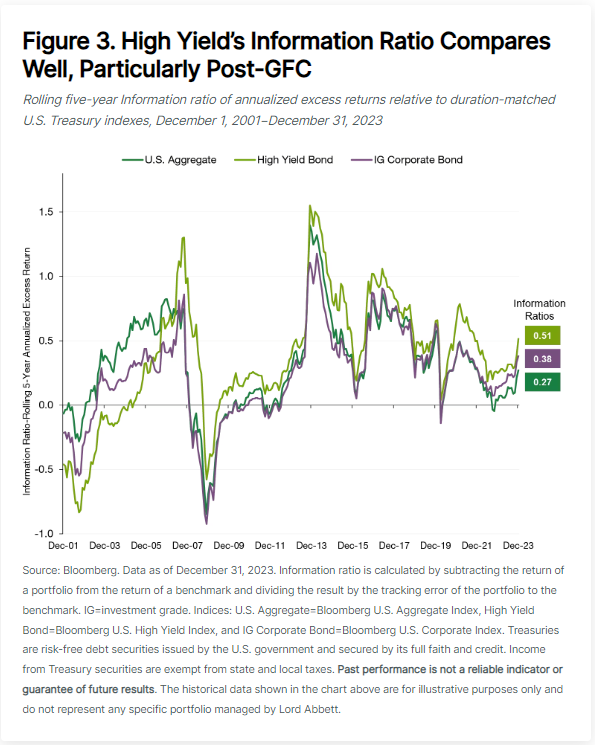

- Information ratios using excess returns similarly touts the benefits of credit. Specifically, high yield’s excess return information ratio relative to a duration-matched Treasury index exceeded that of the U.S. Aggregate Index relative to a duration-matched Treasury index 100% of the time on a rolling five-year basis, starting from late 2005—the first rolling five-year measurement period ended as of December 31, 2009—through 2023.

Why Consider Excess Returns?

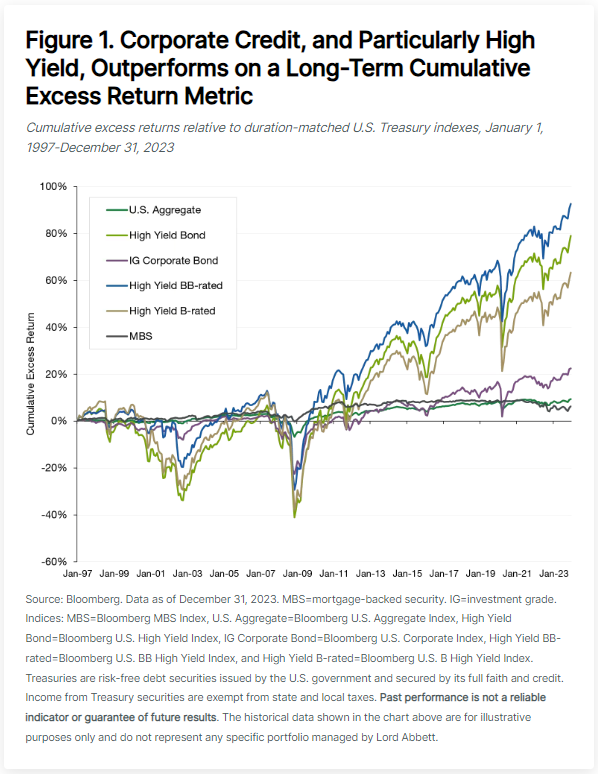

Investors often focus on asset-specific benchmarks for credit markets, but less so on the performance of credit versus a duration-matched Treasury index alone. The latter approach simply strips out the tailwind of risk-free yields—Treasuries are considered risk-free securities—in generating total returns, as well as the performance impact of any ensuing moves in interest rates. This allows us to consider the merits of credit exposure on its own. Investors can then separately make distinct decisions on overall duration posture through portfolio rate overlays that are independent of the characteristic durations of preferred credit asset classes. As a reminder, portfolio overlays are additional investment vehicles or securities that are added to a portfolio to adjust a specific investment objective, such as interest-rate or currency exposure. In Figure 1, we start by tracking the long-term cumulative excess return of various fixed-income indices, including the generic fixed-income catch-all, the Bloomberg U.S. Aggregate Index.

While there are plenty of takeaways to note, perhaps most powerful is the lead that high yield corporates have enjoyed over higher-rated slices of fixed income. Additionally, within high yield, BB’s performance gap over B’s may initially strike as surprising, given the latter’s higher starting yields.

But this outperformance raises an important question for investors: is credit’s long-term advantage due to several short periods of excellent performance, or is it consistent over time? In Figure 2, we present the annualized rolling five-year excess returns for the same indexes. Essentially, we are breaking down the cumulative performance of Figure 1 into five-year periods of time instead and displaying the annualized excess return over rolling periods.

Here it’s clearer that there have been some periods of time when various credit asset classes have indeed underperformed a duration-matched Treasuries portfolio, most notably in and through the stressed environments of the “Tech Wreck” from the early 2000s and of course, the Great Financial Crisis (GFC). But as noted in the table in Figure 2, generally we see all forms of credit exposure outperforming Treasuries (i.e., positive excess returns) close to 80% of the time. Yes, agency MBS serving up positive annualized excess returns in 82% of rolling five-year periods edges out high yield at 79%, but just barely. But the median annualized excess returns of investment grade (89 bps) and high yield (278 bps) appear to be superior alternatives versus agency mortgages, or the U.S. Aggregate Index itself, with a similar proportion of positive excess return periods.

Corporate Credit’s Information Ratios Compare Favorably Too

Finally, we can compare information ratios across asset classes considering duration-matched indexes of Treasuries (matched to the duration of each asset class) as the benchmarks in the calculation. In Figure 3, we track the rolling five-year information ratio of annualized excess returns for investment grade, high yield, and the U.S. Aggregate Index. Clearly, the directional trends will mimic what we observed in Figure 2. But the benefit in this analysis is the ability to better capture how investors are being compensated for the underlying volatility of those excess returns by asset class.

Again, high yield credit compares particularly well. Over the entire period shown, high yield’s information ratio exceeded that of the U.S. Aggregate Index 75% of the time. More notably, starting the measurement period post-GFC (which would include the five-year period ended as of December 31, 2009, as the starting point through December 31, 2023) shows high yield’s information ratio exceeding that of the U.S. Aggregate 100% of the time.

Summing Up

We believe the current nominal-yield environment will produce a fruitful set of opportunities for years to come. Treasuries may colloquially be considered risk-free assets. But our work here suggests that credit, and corporate credit in particular, can provide compelling portfolio benefits for investors over the long term—over shorter periods through time, as well as when adjusted for the volatility of those returns versus duration-matched Treasuries alone.

About the Contributors

As informações aqui contidas estão sendo fornecidas pela GAMA Investimentos (“Distribuidor”), na qualidade de distribuidora do site. O conteúdo deste documento [e informações neste site] contém informações proprietárias sobre LORD ABBETT e o Fundo. Nenhuma parte deste documento nem as informações proprietárias do LORD ABBETT ou DO Fundo aqui podem ser (i) copiadas, fotocopiadas ou duplicadas de qualquer forma por qualquer meio (ii) distribuídas sem o consentimento prévio por escrito do LORD ABBETT. Divulgações importantes estão incluídas ao longo deste documento e que devem ser utilizadas exclusivamente para fins de análise do LORD ABBETT e do Fundo. Este documento não pretende ser totalmente compreendido ou conter todas as informações que o destinatário possa desejar ao analisar o LORD ABBETT e o Fundo e/ou seus respectivos produtos gerenciados ou futuramente gerenciados. Este material não pode ser utilizado como base para qualquer decisão de investimento. O destinatário deve confiar exclusivamente nos documentos constitutivos de qualquer produto e em sua própria análise independente. Nem o LORD ABBETT nem o Fundo estão registrados ou licenciados no Brasil e o Fundo não está disponível para venda pública no Brasil. Embora a Gama e suas afiliadas acreditem que todas as informações aqui contidas sejam precisas, nenhuma delas faz qualquer declaração ou garantia quanto à conclusão ou necessidades dessas informações.

Essas informações podem conter declarações de previsões que envolvem riscos e incertezas; os resultados reais podem diferir materialmente de quaisquer expectativas, projeções ou previsões feitas ou inferidas em tais declarações de previsões. Portanto, os destinatários são advertidos a não depositar confiança indevida nessas declarações de previsões. As projeções e/ou valores futuros de investimentos não realizados dependerão, entre outros fatores, dos resultados operacionais futuros, do valor dos ativos e das condições de mercado no momento da alienação, restrições legais e contratuais à transferência que possam limitar a liquidez, quaisquer custos de transação e prazos e forma de venda, que podem diferir das premissas e circunstâncias em que se baseiam as perspectivas atuais, e muitas das quais são difíceis de prever. O desempenho passado não é indicativo de resultados futuros.