Link para o artigo original : https://www.lordabbett.com/en-us/financial-advisor/insights/markets-and-economy/some-positive-signs-for-high-yield-credit.html

Insight • September 7, 2022

Some Positive Signs for High Yield Credit

By Stephen Hillebrecht Director, Product Messaging

By Stephen Hillebrecht Director, Product Messaging

Bond investors have faced a number of challenges in 2022, as the highest U.S. inflation readings in four decades led to higher U.S. Treasury yields across the curve, resulting in negative returns for most high-grade fixed income classes. Meanwhile, fears of an aggressive policy response by the U.S Federal Reserve (Fed) caused an uptick in the probability of a recession, and wider credit spreads across corporate credit.

The combination of higher risk-free yields and wider credit spreads led to a 14.0% loss for U.S. high yield bonds (as measured by the ICE BofA U.S. High Yield Index, herein referred to as the benchmark index) through the first six months of the year which, outside of the 26% decline in 2008, would represent a return far worse than any calendar year going back to the index’s inception in 1987.

Investors responded by exiting the asset class. Using U.S. mutual fund flow data as a proxy for investor demand, high yield bond funds experienced roughly $47 billion in outflows in the first half of the year, the worst six-month stretch for flows on record. (All fund-flow data from Lipper.) On the one hand, this is to be expected: in previous recessions, high yield spreads typically widened to north of 900 basis points (bps)—well above the low 300s level of the index at the start of 2022—as compensation for the probability of increasing defaults. However, there are several counterpoints to this being a typical recession for high yield.

The Fundamental Backdrop

We have seen two consecutive quarters of negative GDP, which many have accepted to be the definition of a recession. However, the labor market remains strong, with the U.S. economy adding an average of about 500,000 jobs per month over the past 12 months, and average hourly earnings increasing 5.2% over the past year. Consumer balance sheets remain strong, based on BofA data suggesting median savings and checking balances are 40% above pre-pandemic levels.

That backdrop suggests that any recession is likely to be relatively mild and short-lived. And while a slowing economy presents challenges to high yield credit, the asset class is entering this period in very healthy condition. After a bout of elevated defaults during the COVID-induced economic shutdown, which led to the disappearance of many weaker credits, surviving issuers took advantage of open credit markets to refinance debt, extend maturities, and shore up their balance sheets. High yield bond defaults over the 12 months ending August 31 remain below 1.0%. While that is likely to increase as the economy slows, the asset class is starting the last four months of 2022 in a good position:

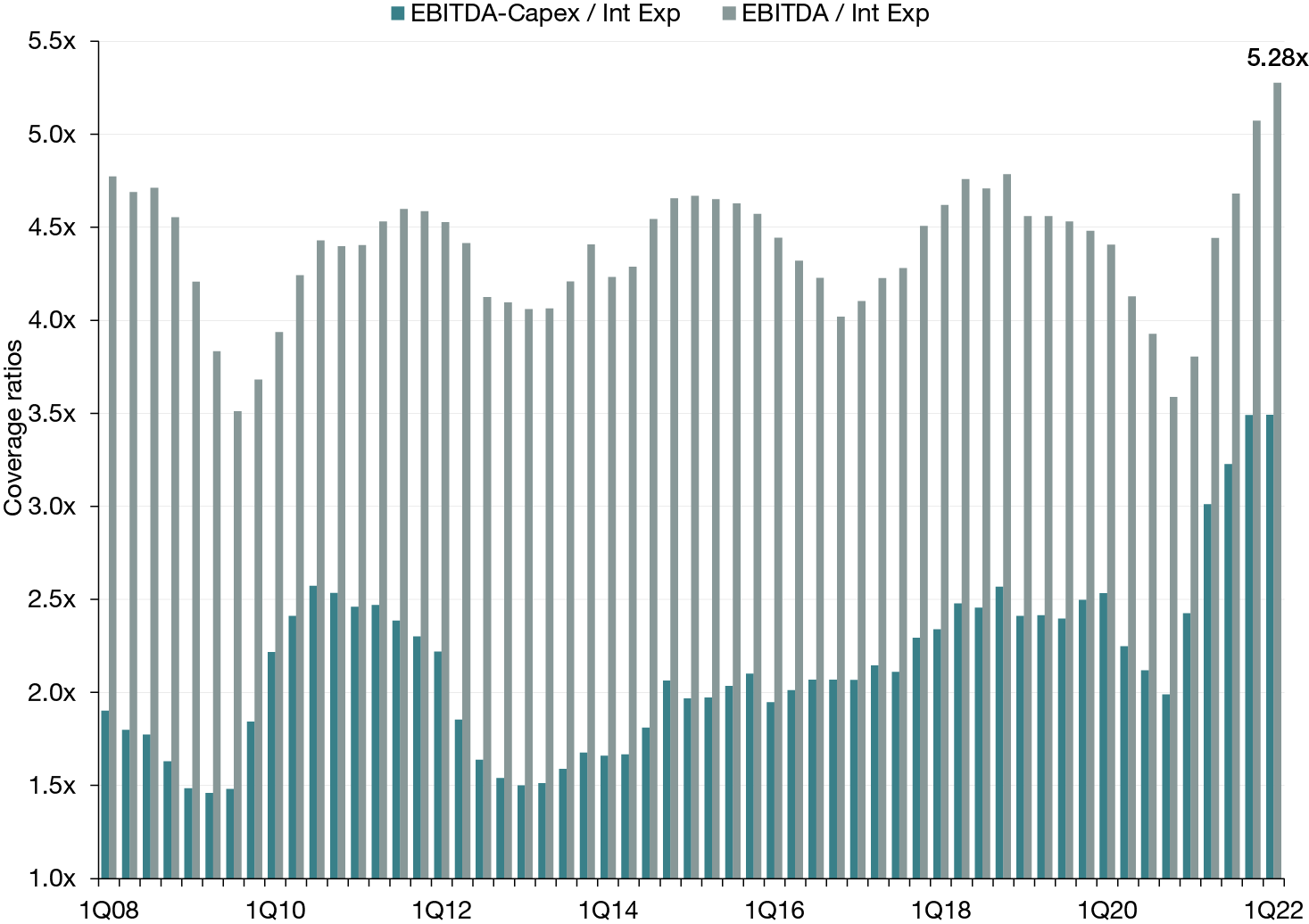

· High yield issuers’ credit metrics were solid, with a net interest coverage ratio (EBITDA/interest expense) of 5.3x, the highest on record (see Figure 1).

Figure 1. High Yield Balance Sheets Are Well Positioned for a Slowing U.S. Economy

Past performance is not a reliable indicator or guarantee of future results. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment.

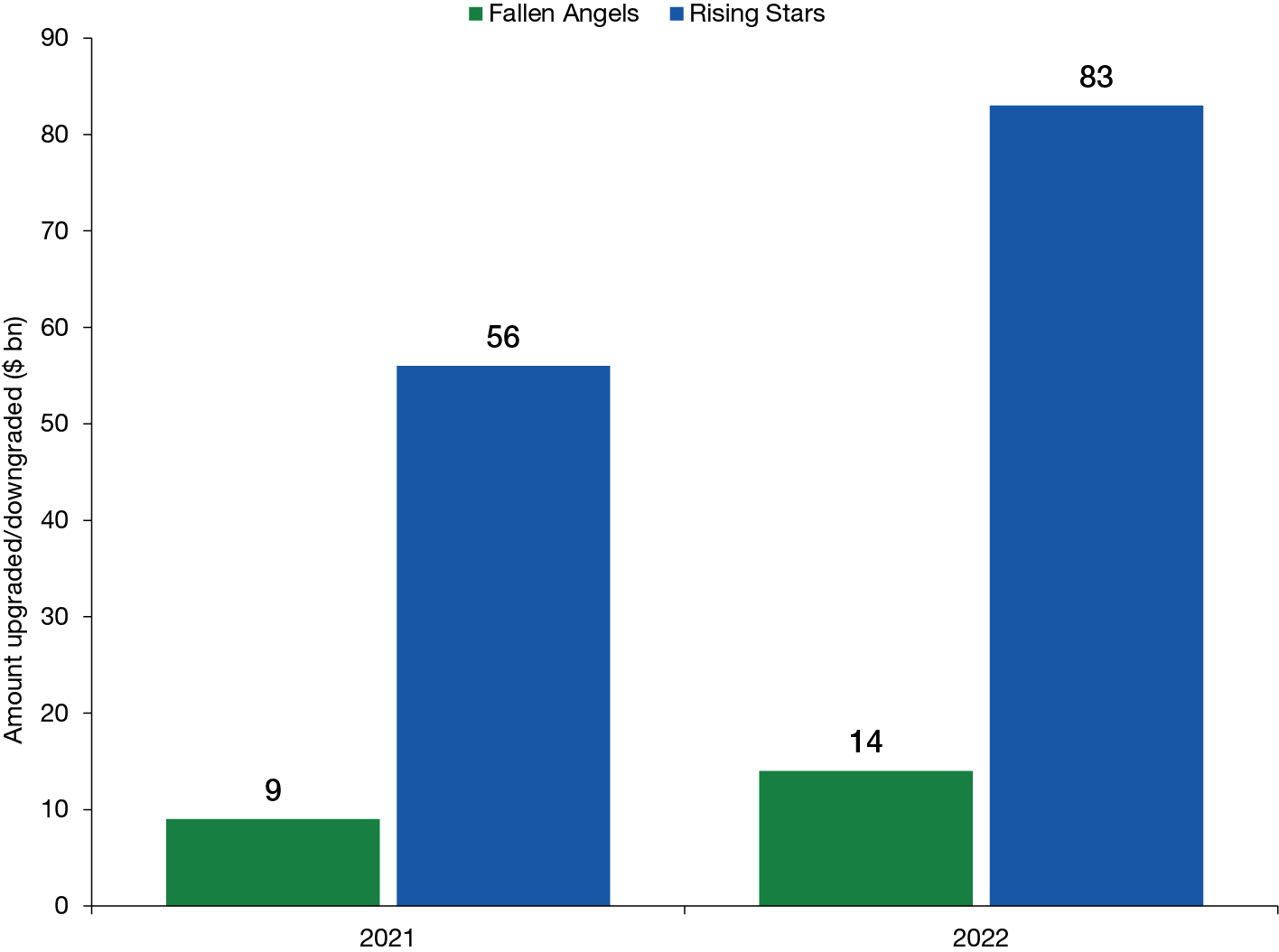

· The number of “rising stars” (high yield issuers that have been upgraded to investment grade) in 2022 has also set a new calendar year record in only eight months (see Figure 2).

Figure 2. Rising Stars Have Already Reached a Calendar-Year Record in 2022

Past performance is not a reliable indicator or guarantee of future results. For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment.

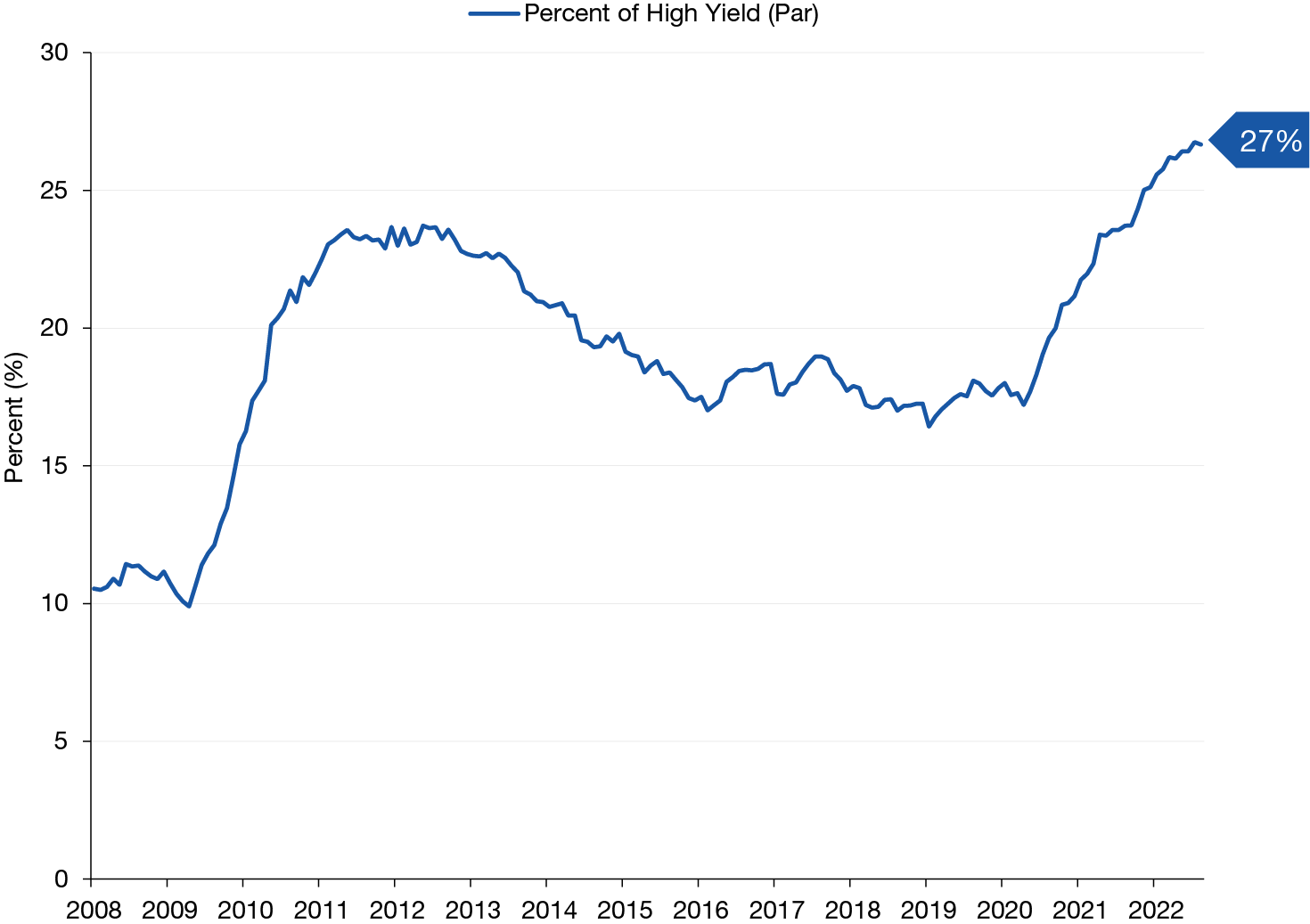

Figure 4. Secured Bonds Now Account for More than One-Quarter of the High Yield Benchmark

· On that note, recoveries in the case of default in 2022 are also at record levels of 65%, versus the long-term average of 40%. While this is based on a very small number of defaults, this may be another data point supporting limited downside in adverse conditions, particularly with the average dollar price in the high yield index now roughly $87.

Given all those factors, one can make the case that spreads may not widen as much, and defaults should not increase as much, as they have in previous recessions.

In addition, while the greater prevalence of rising stars is an indication of the positive fundamental trends in credit, it has also set up a potentially supportive technical factor, as approximately $90 billion in face amount of high yield bonds has exited the benchmark index. With year-to-date supply of high yield bonds declining by about 75% versus last years’ pace, the total size of the index has decreased by about $130 billion, or 8.2%, from its peak last October. So, despite the large outflow from mutual funds, reduced supply paired with a large number of calls, maturities and tenders have reduced the amount of high yield bonds outstanding, creating a positive technical tailwind.

Into the Second Half of 2022

As the calendar turned to July, following the worst six-month period of outflows from high yield bond mutual funds on record, the high yield index jumped 6.0% in July, the best month of performance for the benchmark index since 2009, highlighting the risk to timing the market. Spreads peaked above 600 bps in late June and then tightened by 175 bps over a six-week period, one of the fastest such periods of tightening on record. Money came back into the asset class, with over $7.5 billion flowing back into high yield funds in the last two weeks of July. All of that was reversed in the late August, with the category witnessing over $9.5 billion in outflows over a two-week period following Fed Chairman Jerome Powell’s speech in Jackson Hole, Wyoming, on August 26, which brought on renewed fears of aggressive monetary policy.

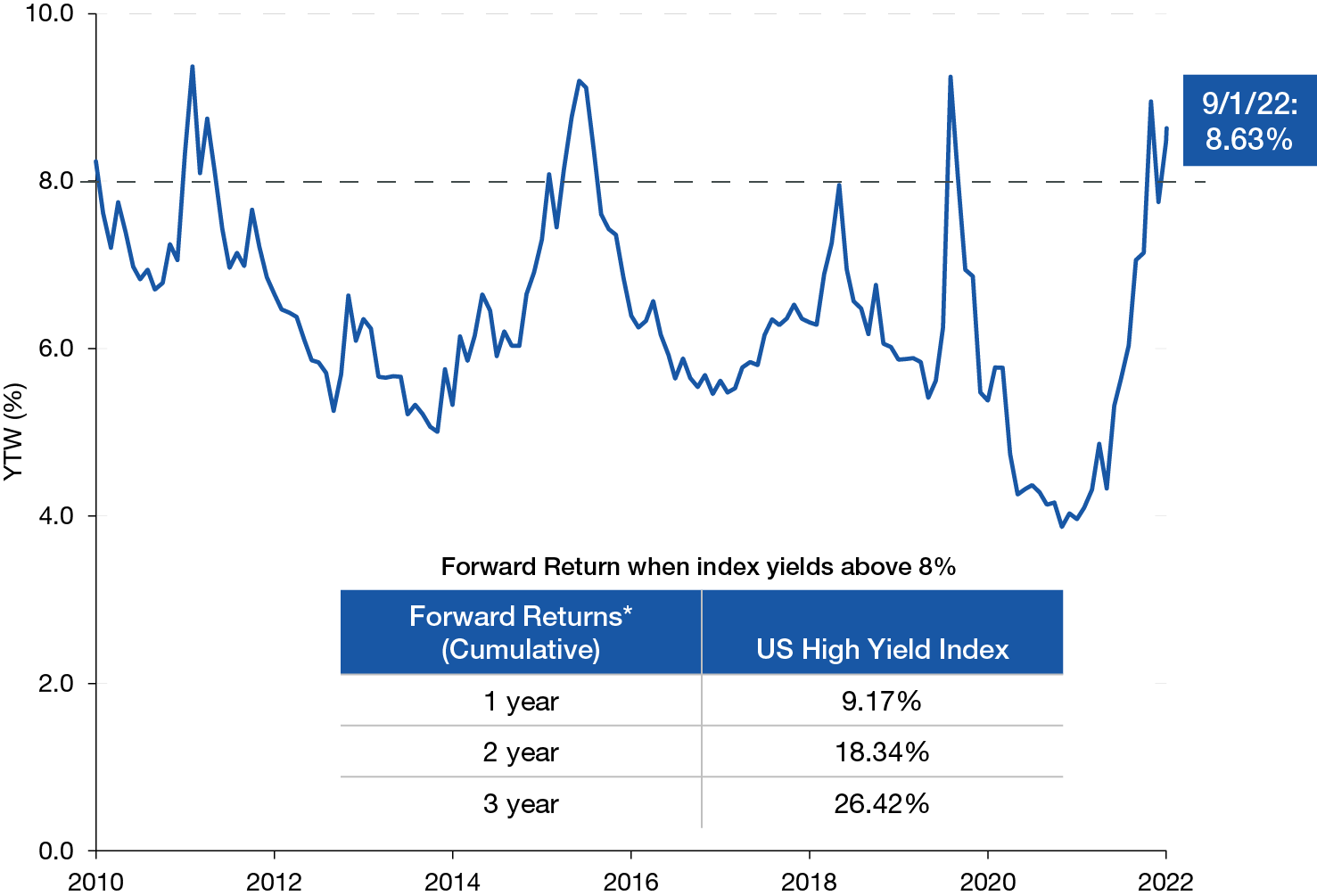

Recent events illustrate how many investors try to time the market and tactically allocate in and out of high yield. But the risk-off environment in recent weeks has caused high yield spreads to widen back out above 500 bps, pushing the average yield back up to 8.6%, a level that has historically been an attractive entry point for forward returns (see Figure 5).

Figure 5. Elevated Yields May Present an Attractive Entry Point for High Yield

Source: ICE Data Indices, LLC. Past performance is not a reliable indicator or guarantee of future results. It is important to note that the high-yield market may not perform in a similar manner under similar conditions in the future. The historical data shown in the chart above are for illustrative purposes only and do not represent any specific portfolio managed by Lord Abbett or any particular investment. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

As informações aqui contidas estão sendo fornecidas pela GAMA Investimentos (“Distribuidor”), na qualidade de distribuidora do site. O conteúdo deste documento [e informações neste site] contém informações proprietárias sobre LORD ABBETT e o Fundo. Nenhuma parte deste documento nem as informações proprietárias do LORD ABBETT ou DO Fundo aqui podem ser (i) copiadas, fotocopiadas ou duplicadas de qualquer forma por qualquer meio (ii) distribuídas sem o consentimento prévio por escrito do LORD ABBETT. Divulgações importantes estão incluídas ao longo deste documento e que devem ser utilizadas exclusivamente para fins de análise do LORD ABBETT e do Fundo. Este documento não pretende ser totalmente compreendido ou conter todas as informações que o destinatário possa desejar ao analisar o LORD ABBETT e o Fundo e/ou seus respectivos produtos gerenciados ou futuramente gerenciados. Este material não pode ser utilizado como base para qualquer decisão de investimento. O destinatário deve confiar exclusivamente nos documentos constitutivos de qualquer produto e em sua própria análise independente. Nem o LORD ABBETT nem o Fundo estão registrados ou licenciados no Brasil e o Fundo não está disponível para venda pública no Brasil. Embora a Gama e suas afiliadas acreditem que todas as informações aqui contidas sejam precisas, nenhuma delas faz qualquer declaração ou garantia quanto à conclusão ou necessidades dessas informações.

Essas informações podem conter declarações de previsões que envolvem riscos e incertezas; os resultados reais podem diferir materialmente de quaisquer expectativas, projeções ou previsões feitas ou inferidas em tais declarações de previsões. Portanto, os destinatários são advertidos a não depositar confiança indevida nessas declarações de previsões. As projeções e/ou valores futuros de investimentos não realizados dependerão, entre outros fatores, dos resultados operacionais futuros, do valor dos ativos e das condições de mercado no momento da alienação, restrições legais e contratuais à transferência que possam limitar a liquidez, quaisquer custos de transação e prazos e forma de venda, que podem diferir das premissas e circunstâncias em que se baseiam as perspectivas atuais, e muitas das quais são difíceis de prever. O desempenho passado não é indicativo de resultados futuros.