Link para o artigo original: https://www.lordabbett.com/en-us/financial-advisor/insights/investment-objectives/q-a–views-on-the-credit-markets-through-a-multi-sector-lens.html

Q&A: Views on the Credit Markets Through a Multi Sector Lens

The investment environment has evolved since the beginning of the year. We asked Lord Abbett Partner & Co-Head of Taxable Fixed Income, Steven Rocco, for an update.

By Steven F. Rocco Partner & Co-Head of Taxable Fixed Income

By Steven F. Rocco Partner & Co-Head of Taxable Fixed Income

Partner and Co-Head of the Lord Abbett Taxable Fixed Income team, Steven Rocco, discusses the macroeconomic factors influencing the fixed-income markets today and provides an update on credit portfolio positioning based on the opportunities and risks that may be ahead.

Q: How were you thinking about the markets at the start of the year, and what are your thoughts today, given developments in the macroeconomic landscape?

A: I think about the macro environment in terms of probabilities and regimes. Looking back to the end of 2023 into 2024, the interest-rate regime was more one of an economic soft landing, which was clearly good for risk assets. Our view coming into 2024 was that we would be in more of a reflationary regime, which, in recent periods, seems to have come to pass. And I define reflationary regimes as a reacceleration of inflation with strong, steady growth. The growth that we’ve seen in the U.S. has been particularly resilient. We are also seeing an uptick in growth outside of the U.S., particularly in manufacturing in Europe. It’s early, but China also had a strong first quarter, which certainly plays into global growth expectations. That turn in manufacturing, while the consumer has been strong, has led to this reacceleration in pockets of goods inflation, while, at the same time, inflation on the service side has remained sticky.

I think a soft-landing scenario is still possible. Slowing growth and a reflationary regime that we’re in now could persist. The risk is if we head into what I call an inflationary regime. An inflationary regime was simply 2022. And that’s a period when inflation is rising, and the central banks are fighting it. Right now, we don’t have the central banks fighting it. So, ultimately, that’s good for risk. But depending on if you’re in a soft landing or reflation, you may need different types of exposure.

Leveraged credit should do well, in our view, in a reflationary regime. Sectors such as high yield bonds and floating-rate securities generally should do well over fixed-rate securities. You may also want to consider leaning a bit to short duration across strategies.

Moving to a period of a potential regime shift back into inflation could be a challenge. It is one thing for the markets to anticipate seven rate cuts in 2024, which was the case at the beginning of the year, but currently markets are pricing in about two. The recent volatility in the markets has partly been caused by this change in U.S. Federal Reserve (Fed) expectations, now with some possibility of a rate hike entering some investors’ probability distribution. We currently believe that the Fed will keeps rates steady. I haven’t removed soft landing from my probability distribution, but I think I have a higher probability on reflation.

Q: What is your view on credit within a fixed-income allocation, and which sectors may provide opportunities ahead?

I think the challenge here is that we recognize that credit spreads are tight. It’s not a market where you want to be at a maximum risk level in any of these asset classes. However, within high yield, a large segment of bonds is still priced at a discount, not because of credit stress, but because the prevailing interest-rate environment has changed materially since issuance of these bonds. As issuers continue to follow the prudent practice of addressing upcoming maturities well in advance, we note that the overall index spread level does not capture the potential accelerated pull to par—a bond’s price moves toward face value or par, as it approaches maturity due to early refinancing. So, we think the yield-to-maturity (and credit spreads) quoted in many headline indexes isn’t properly capturing this effect. We believe this represents an opportunity in the short end of the high yield market in particular.

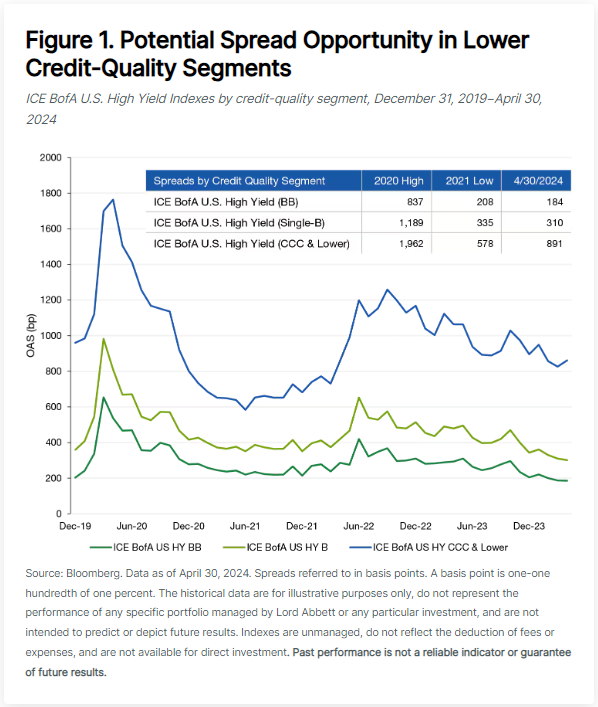

While we think high yield could outperform investment-grade bonds, we believe floating-rate, high yield could provide an even better opportunity. We do think being on the front end of the curve, such as in short-term securities, is better than being on the long end of the curve, and we find opportunities in floating-rate securities in the securitized sector. We also see opportunity in lower credit-quality instruments, such as single B-rated and CCC-rated credits, as we think spreads have more room to compress in those ratings segments (see Figure 1). Meanwhile, we still look to avoid some rate-sensitive parts of the high yield market. In an inflationary environment, issuers linked to commodities, like energy and base metals, tend to do well. While spreads may be tight, high nominal economic and earnings growth favor the continued performance of the high yield market.

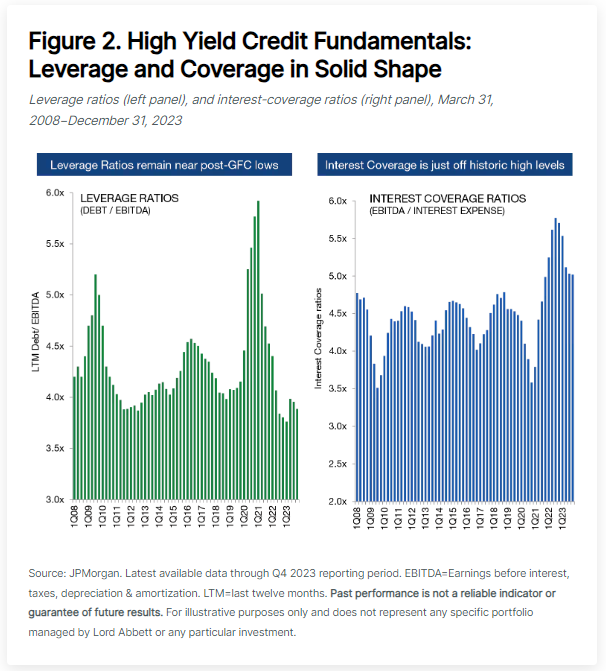

High yield issuers’ balance sheets have been in pretty good shape (see Figure 2). Leverage sits near a post-Great Financial Crisis (GFC) low, and although interest coverage ratios have ticked down slightly, they are still at healthy levels relative to historical measures. Clearly, the evolution of interest coverage will be interesting, as low-coupon bonds are replaced over time with higher-coupon bonds. That will likely move slowly however, and the question is will the numerator of earnings and cashflow move faster than the denominator of interest expense— in other words, will strong earnings growth enable a company to pay interest expense more easily? Ultimately, we think coverage should remain stable, given our positive earnings outlook.

We are also bullish on Europe and the European economic cycle that is coming to pass. Germany’s economy also seems to be turning. At the same time, the European Central Bank has more room to consider rate cuts, and cutting into a reacceleration there is very bullish for risk assets.

Q: What would be a description of an overall theme today for multi-sector credit investing, given the current investment landscape, along with the outlook for interest rates and economic growth?

I think you want to be balanced in this environment and have the flexibility of a multi-sector credit approach. We’ve seen rapid narrative shifts in this market from hard landing to soft landing to now maybe no landing. My view is we’re shifting back and forth between this soft-landing regime and a reflation regime, with a higher probability in reflation. However, that can change with a couple of data points that put the view back to soft landing, and that is also good for risk. My probability of a rate hike is very, very small, but it is in a probability distribution now, and it wasn’t in January. But overall, we think a good environment for both investment-grade and high yield credit may persist, particularly if we continue to see a lack of widespread, late-cycle, credit-destructive behavior by companies themselves.

About the Author

Essas informações podem conter declarações de previsões que envolvem riscos e incertezas; os resultados reais podem diferir materialmente de quaisquer expectativas, projeções ou previsões feitas ou inferidas em tais declarações de previsões. Portanto, os destinatários são advertidos a não depositar confiança indevida nessas declarações de previsões. As projeções e/ou valores futuros de investimentos não realizados dependerão, entre outros fatores, dos resultados operacionais futuros, do valor dos ativos e das condições de mercado no momento da alienação, restrições legais e contratuais à transferência que possam limitar a liquidez, quaisquer custos de transação e prazos e forma de venda, que podem diferir das premissas e circunstâncias em que se baseiam as perspectivas atuais, e muitas das quais são difíceis de prever. O desempenho passado não é indicativo de resultados futuros.