Featured Authors

Armen Panossian

Armen Panossian

Head of Performing Credit and Portfolio Manager

Danielle Poli, CAIA

Danielle Poli, CAIA

Managing Director, Multi-Asset Credit Product Specialist and Head of the Product Specialist Group

THE GREAT DEBATE

“The debate rages on regarding whether today’s inflation will prove permanent or transitory. There’s a great deal riding on the answer since higher inflation would doubtless lead to higher interest rates and thus lower asset values. But in my view, it’s impossible to know the answer.”

– Howard Marks, Thinking About Macro

The third quarter of 2021 presented economic forecasters with a host of surprises: natural gas prices spiked by over 30% in one month, the 10-year Treasury yield recorded one of its biggest one-week jumps of the year, and the U.S. economy created less than 200,000 jobs in September – the month when Americans were supposed to flood back into the labor force. Credit investors should consider this backdrop before attempting to answer the question currently dominating market discussions: how long will inflation remain elevated?

As Oaktree co-founder Howard Marks recently wrote, no one fully understands – let alone can predict – inflation dynamics. However, the topic is too vital to be ignored, as persistently high inflation would likely force the Federal Reserve to increase interest rates faster than investors currently expect. So we believe it’s important to view this debate with objectivity, flexibility and a large dose of humility.

TEAM TRANSITORY

Fed Chair Jay Powell and many others believe that U.S. inflation – which is currently running above 5% – will only remain elevated for a short period of time before falling back near the central bank’s 2% target. This group makes a number of compelling arguments.

First, while the inflation rate is high, it isn’t accelerating significantly. In the 12 months through September, the Consumer Price Index rose by 5.4%, roughly the same rate as in the previous three months. Importantly, the month-over-month increases recorded in July, August and September averaged 0.4% compared to 0.9% in June.

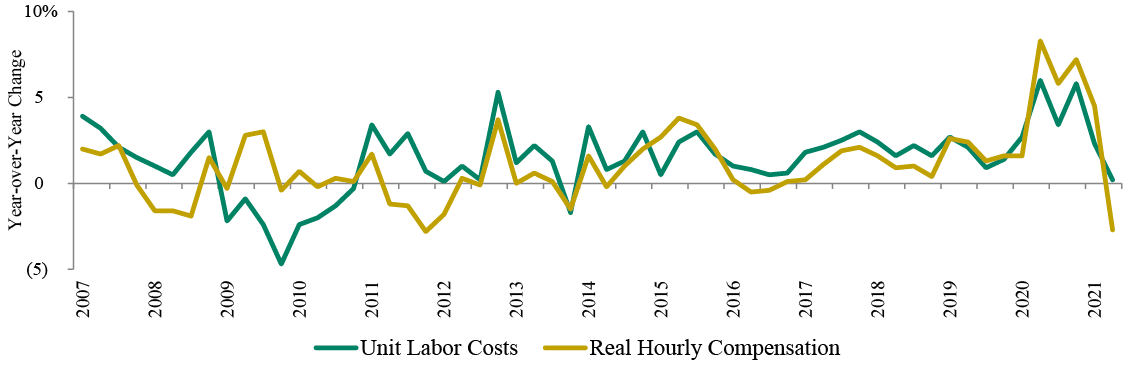

Next, wage increases don’t appear to be strong enough to sustain high inflation. In order for prices to continue rising rapidly, consumers need to have more money to spend moving forward. While many workers have seen their wages increase in 2021, this growth hasn’t kept up with inflation. Thus, real wages have actually declined. Additionally, the year-over-year increase in unit labor costs – a measure of productivity-adjusted compensation per unit of output – was only 0.2% in 2Q2021 versus 2.3% in 1Q2021 (see Figure 1). This metric has been highly correlated with inflation for at least the last 60 years.1 This doesn’t sound like the recipe for an inflationary spiral.

Figure 1: Real U.S. Hourly Compensation and Unit Labor Costs

Source: U.S. Bureau of Labor Statistics

Also, consumption may slow despite the roughly $2 trillion in excess savings households amassed during 2020.2 Spending on durables spiked in 2020,3 indicating demand was likely pulled forward. Consumers may therefore buy fewer big-ticket items, such as refrigerators and cars, in the coming months. While spending on services may increase, such expenditures likely wouldn’t be enough to offset a substantial decline in durables purchases.

Consumers may also be loath to dip into their savings now that the economic recovery appears to be slowing. While economic data was mixed during the third quarter, the vast majority of surprises were on the downside. And consumer sentiment has fallen sharply, nearing a decade low in August, due to the spread of the Delta variant, rising inflation, and fears that the job market may be souring.4

Finally, secular disinflationary forces, such as an aging population, technology and globalization, remain in place, even if the latter may look different moving forward. This all suggests that sustaining +2% inflation over more than a few quarters will be challenging.

NOT SO FAST

Despite all of the above, we believe dismissing the risk of persistently high inflation is unwise, partly because of the unique nature of the last 19 months. Before 2020, the world had never purposefully shut down a significant percentage of the global economy and then tried to restart it. No one knows how long it will take for jammed supply chains to become unstuck and the labor force to be reconstituted. And the U.S. has never increased its money supply by roughly 30% in less than two years.5 Caution is warranted when using historical data to predict the long-term implications of such unprecedented actions.

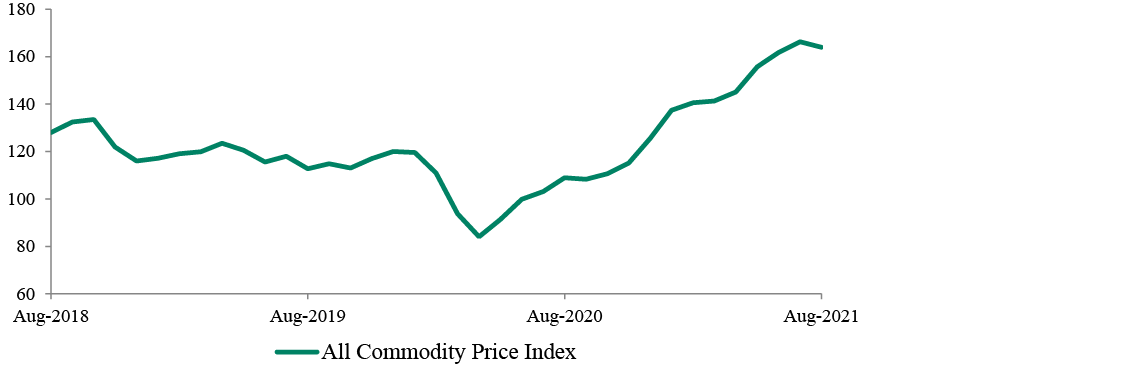

Additionally, surging commodity prices may make many goods more expensive and impact the inflation outlook. The commodity price index has risen by over 30% from the pre-pandemic level (see Figure 2). If Americans keep having to pay more at the gas pump and the grocery store, their inflation expectations will likely continue rising. Consumers already believe inflation will be 5.3% in one year and 4.2% in three years6 – well above market expectations for long-term inflation indicated by the 2.4% breakeven rate at quarter-end.7

Finally, the debate about wage inflation is far from settled. Executives at many large and small U.S. businesses continue to report substantial problems with labor shortages and wage pressure. While wage data might not entirely support these executives’ claims, investors should be cautious about ignoring on-the-ground evidence. This is particularly true at a time when economic data is extremely noisy.

Figure 2: All Commodity Price Index

Source: International Monetary Fund

Note: 2016 = 100; includes both fuel and non-fuel price indices

WHAT NOW?

The probability that inflation will be transitory appears to be higher than the alternative, but probability isn’t certainty. And inflation risk and interest rate risk remain greater than they’ve been in years.

We believe credit investors trying to identify relative value in this uncertain environment should keep a few key points in mind.

(1) The U.S. economy is still growing at an above average rate.

While the economy is unlikely to expand by 7% in 2021 as some economists were anticipating earlier in the year, predictions of stagflation seem premature. The U.S. could still easily report GDP growth of 5% this year, and it’s reasonable to assume growth will remain above the country’s long-term 2% average through 2022. This level of economic activity might not be ideal for equity investors who are pricing in more optimistic expectations, but it should continue to support debt issuers’ fundamentals.

(2) Default rates have continued to fall.

The default rates on U.S. high yield bonds and loans have decreased by over five and three percentage points, respectively, in 2021.8 And the total amount of defaulted U.S. leveraged credit is on track to be the smallest since 2007.9 This is unsurprising, as many businesses raised far more liquidity than they needed in 2020, and companies don’t default when holding large amounts of cash. Additionally, many companies have refinanced their debt since the onset of the pandemic, extending maturities and lowering interest expenses.

Still, the last time default expectations were this low was 2007, underscoring the difference between forecasts and reality.

(3) Rising prices are a global concern.

Europe and the UK are both struggling under the weight of surging gas prices and supply-chain problems. The UK – which is also suffering from Brexit-related shortages – reported higher inflation in August than many anticipated, and inflation expectations are now loftier than they’ve been in over a decade. This prompted the Bank of England to signal that it will soon tighten monetary policy. European high yield bond and loan investors, who have been benefiting from the region’s economic recovery, may have become too complacent about the risks posed by rising prices.

Additionally, emerging market central banks are struggling to maintain price stability while also supporting recovering economies. And a few, including those in Brazil and Mexico, have already increased interest rates.

(4) China’s struggles create risks and opportunities.

The Chinese government might be able to handle the China Evergrande Group’s debt crisis, but the company’s difficulties could signal bigger problems ahead for the world’s second-largest economy – including a slowdown in growth. This would pose a substantial risk to commodity-producing countries, as China is often one of their main export markets.

Fears surrounding China weighed on emerging markets debt and global convertibles in the third quarter. However, this situation might generate opportunities for investors who can identify companies that are being marked down primarily because of their geography, not their fundamentals.

(5) Technical issues continue to generate buying opportunities in structured credit.

Collateralized loan obligations (CLOs) – the largest buyers of leveraged loans – have been created at a rapid pace in recent months. The tremendous supply has caused prices of CLOs to be weaker than one would expect based on fundamentals. This is particularly true for sub-investment-grade tranches: yield spreads have remained fairly steady even as the default rates for the underlying loans have fallen. If interest rates continue to rise, demand for these floating-rate assets should increase.

(6) Investors might consider exchanging liquidity for additional potential return.

Investors trying to earn a reasonable return in a low-rate environment have often had to accept additional credit risk or use leverage, strategies that carry significant risk, especially in an uncertain market environment. However, investors with flexibility and a long-term time horizon might potentially earn additional return without dramatically increasing risk by investing in less liquid asset classes like private credit. This large and diverse market covers a range of industries and borrower types, including public companies, entrepreneur-owned businesses and sponsor-backed firms. We believe structuring expertise can be a significant advantage in this market, as it can potentially enable investors to earn excess return, especially in situations that many managers have neither the background nor the skillset to tackle.

MOVE FORWARD, BUT WITH CAUTION

As Howard recently reiterated, “it’s one thing to have an opinion, but something very different to assume it’s right and bet heavily on it.” We believe certain macroeconomic outcomes are more likely than others, but we don’t position our portfolios so that our success depends heavily on our assumptions proving accurate. At this uncertain moment, we think this stance may provide us with downside protection and enable us to take advantage of the mistakes made by those who sincerely believe they know what the future holds.

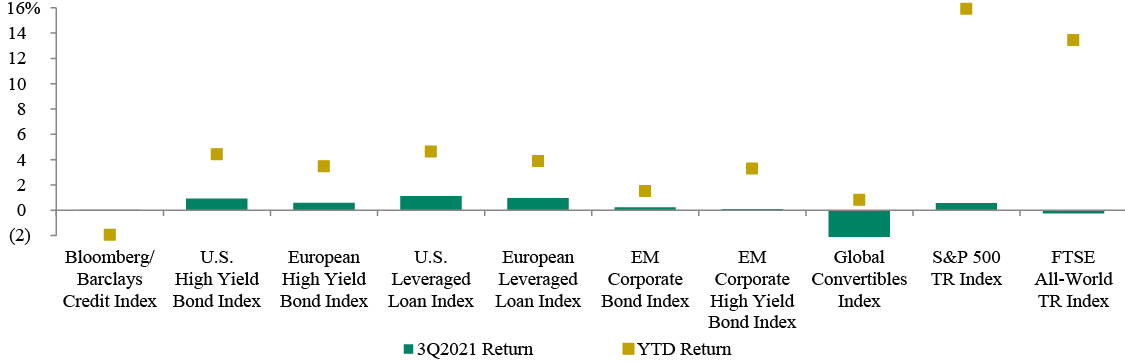

ASSESSING RELATIVE VALUE

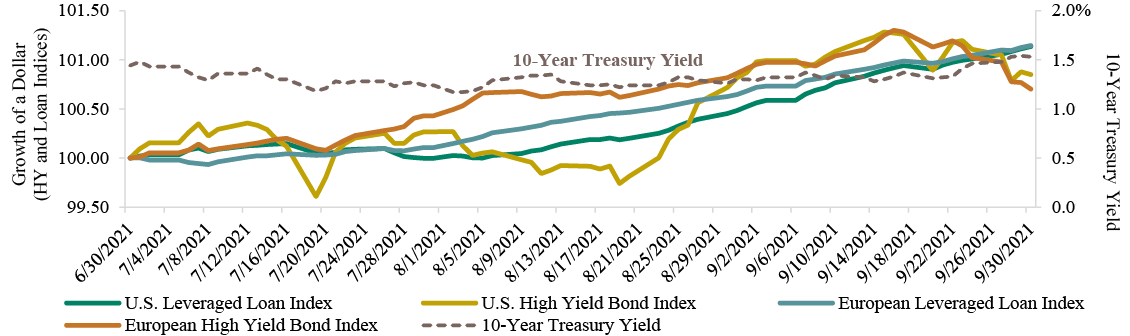

PERFORMANCE OF SELECT INDICES

As of September 30, 2021

Sources: Bloomberg Barclays, Credit Suisse, FTSE, ICE BofA, JP Morgan, S&P Global, Refinitiv10

DEFAULT RATES BY ASSET CLASS

Sources: Bank of America, Credit Suisse, JP Morgan11

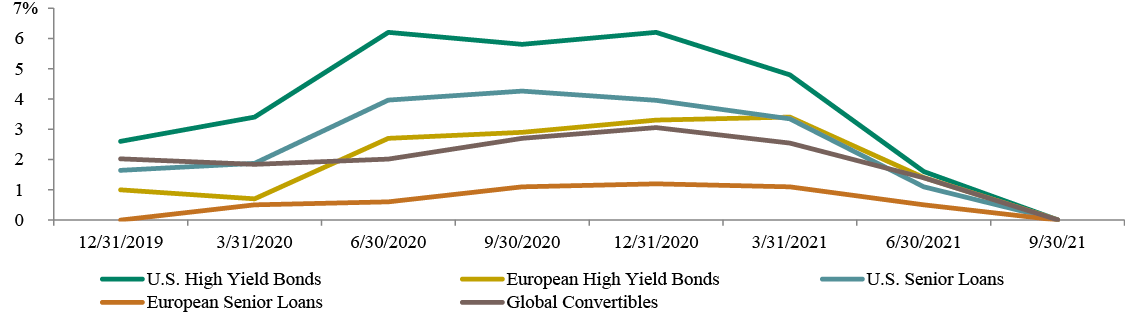

VOLATILITY: HIGH YIELD BONDS VS. LOANS

Sources: Credit Suisse, Bank of America, U.S. Treasury

STRATEGY FOCUS

HIGH YIELD BONDS

Market Conditions: 3Q2021

U.S. HIGH YIELD BONDS

Return: 0.9%12

Issuance: $108.5bn13

LTM Default Rate: 0.9%14

-

The riskiest category – CCC-rated bonds – underperformed higher-rated groups: This reversed the pattern seen in the previous two quarters; macroeconomic concerns likely drove this shift.15

-

Rising interest rates weighed on fixed-rate assets: BB-rated bonds were more negatively affected than lower-rated bonds because of the former’s longer duration.

-

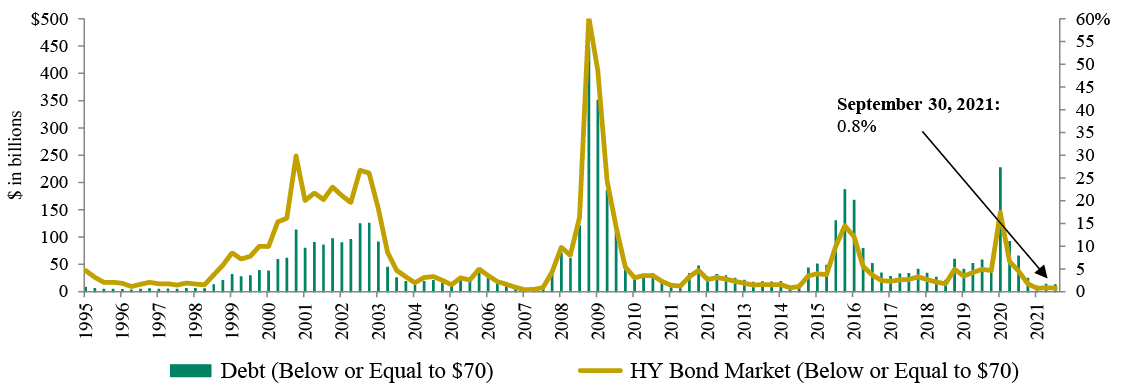

Distress has been very low: Under 1.0% of the market was trading at or under 70 cents on the dollar at quarter-end (see Figure 3).16

EUROPEAN HIGH YIELD BONDS

Return: 0.6%17

Issuance: €20.2bn18

LTM Default Rate: 0.7%19

-

The riskiest bond category outperformed: CCC-rated bonds were the asset class’s top performers.20

-

Coupons have been the major return driver in the U.S. and Europe: Most high yield bonds are trading near par.21

-

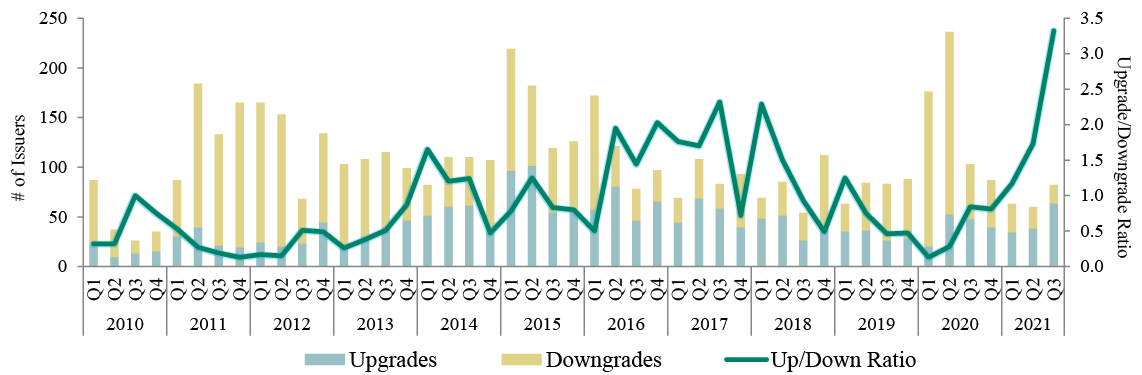

Fundamentals have improved: Credit rating upgrades are significantly outpacing downgrades in both regions (see Figure 4 for details about European issuers).

Outlook

Opportunities

-

The default environment remains benign: High yield bond investors appear to be adequately compensated for default risk, as default rate expectations for 2021 are below 1% in both the U.S. and Europe.22

-

Low interest rate sensitivity is an advantage: Investors normally seek to shorten duration when interest rates are rising. Duration in high yield bonds is significantly lower than that of investment grade bonds.

-

Near-term maturities are negligible: The 2020–2021 wave of refinancings enabled many issuers to extend maturities and reduce interest payments.

Risks

-

Elevated inflation increases the risk that central banks will tighten monetary policy more quickly than anticipated: Lower-rated corporate issuers might struggle to roll over debt in this scenario. The risk is higher for U.S. issuers.

-

Rising inflation and supply-chain problems may weigh on companies’ earnings: Some firms may have trouble passing on high costs to customers.

Figure 3: Distress in U.S. High Yield Bonds Is Low

Sources: ICE BofA, JPMorgan, Credit Suisse

Figure 4: Upgrades Outpace Downgrades Among European High Yield Bond Issuers

Sources: Moody’s, Bloomberg

SENIOR LOANS

Market Conditions: 3Q2021

U.S. SENIOR LOANS

Return: 1.1%23

Issuance: $160.6bn24

LTM Default Rate: 0.7%25

-

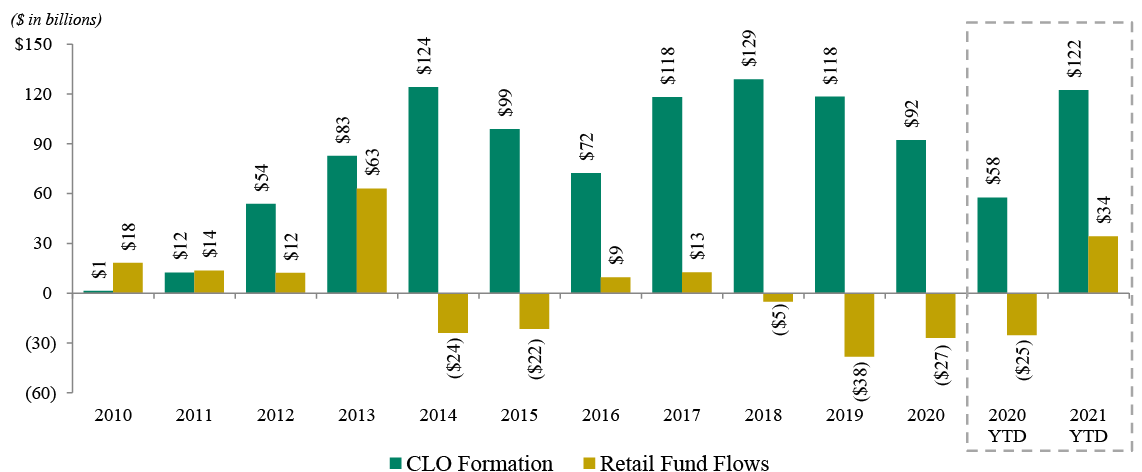

Robust CLO formation continues to boost loan performance: $45.9 billion in new CLOs priced in 3Q2021 (see Figure 5).26 A similar trend was seen in Europe.

-

Retail demand remains very strong: Mutual funds and ETFs recorded 10 consecutive months of inflows through September; inflows in the quarter topped $8.0 billion (see Figure 5).27

-

Loans outperformed most other sub-investment-grade asset classes: Volatility was lower than in high yield bonds, especially when interest rates began to rise.

EUROPEAN SENIOR LOANS

Return: 1.0%28

Issuance: €24.8bn29

LTM Default Rate: 0.1%30

-

Fundamentals have improved: CCC-rated bonds only represented 5.4% of the index at quarter-end, down from the recent peak of 8.3%.31

-

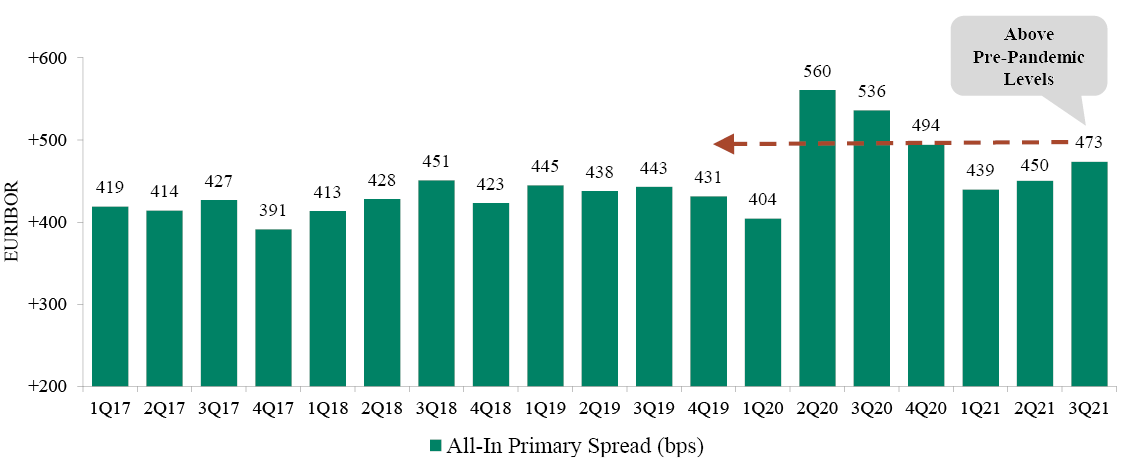

Yield spreads remain attractive: They are wider than the pre-pandemic level (see Figure 6).

Outlook

Opportunities

-

Rising interest rates should benefit floating-rate assets: Investors will likely try to shorten duration if inflation remains elevated and central banks begin tightening monetary policy.

-

Healthy demand will likely remain a tailwind: Demand from CLOs in the U.S. and Europe should support loan prices, as should strong retail demand in the U.S.

-

The default environment remains benign in both regions: The U.S. trailing-12-month default rate is the lowest since February 2012.32

Risks

-

Elevated loan prices may limit return potential: Around 30% of U.S. senior loans were trading above par at quarter-end.33

-

The supply/demand dynamic could degrade loan quality: Borrowers may be able to take on excessive leverage and borrow with weak covenants because of the strong demand for loans and the benign default environment.

-

Debt could become more difficult to service as economic recoveries lose momentum: Leverage remains above pre-pandemic levels in the U.S. and Europe.

Figure 5: U.S. CLO Formation and Retail Inflows Are Among the Highest in 10 Years

Source: JP Morgan

Figure 6: European Senior Loan Yield Spreads Remain Attractive

As of September 30, 2021

Source: Credit Suisse Western Europe Leveraged Loan Index (EUR hedged)

EMERGING MARKETS DEBT

Market Conditions: 3Q2021

EM Corporate Bond Return: 0.3%34

EM Corporate High Yield Bond Return: 0.1%35

-

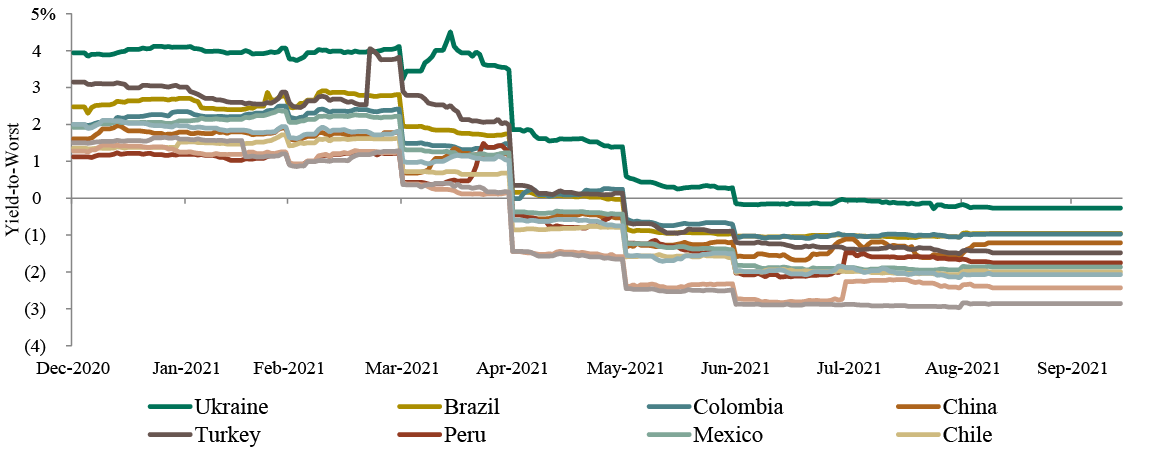

Corporate bond real yields are negative in most EM countries: Rising inflation has eroded value in the asset class. This underscores the disadvantages of an index-based approach to EM debt investment (see Figure 7).

-

Defaults have spiked in China: The year-to-date default rates for Chinese high yield bonds and property bonds are 5.2% and 6.7%, respectively, which are both record highs.36 If the China Evergrande Group defaults, the above rates would increase by 7.7 and 12.7 percentage points, respectively.37

Outlook

Opportunities

-

Recent weakness emanating from China might create buying opportunities: Concerns about an economic slowdown in China could lead to a selloff in EM debt. In this scenario, the debt of EM companies with strong fundamentals could trade at attractive prices.

-

Issuers that can generate consistent cash flow should be well situated even if market conditions deteriorate: Such companies should be able to meet their debt service obligations even if the global economic recovery slows or central banks accelerate their interest-rate-hiking schedules.

Risks

-

Weakness in China may negatively impact commodity-exporting countries: China is the world’s largest consumer of most commodities, so prices of these raw materials would likely decline if the country’s growth were to slow. Iron ore prices fell by around 45% in 3Q2021 partly because of concerns about reduced Chinese demand.

-

EM countries could suffer if developed market central banks aggressively tighten monetary policy: EM government debt burdens increased from 34% in 2012 to 62% in 2020.38 Rising global interest rates would dampen economic activity and make it more expensive for countries to roll over debt.

-

Slowing growth and rising inflation in the U.S. could weigh on EM debt prices: A negative reversal in U.S. financial conditions has historically caused EM yield spreads to widen.39

Figure 7: Emerging Markets Corporate Bond Real Yields Are Now Negative

Source: Bloomberg

GLOBAL CONVERTIBLES

Market Conditions: 3Q2021

Return: -2.1%40

Issuance: $25.0bn41

LTM Default Rate: 0.8%42

-

Weak global equity markets weighed on convertibles’ performance in September: This trend accelerated when interest rates began rising late in the month.

-

Chinese equities performed very poorly: The Hang Seng Index fell by 14.1% during 3Q2021. Markets were rattled by Chinese regulatory announcements, an energy shortage, and the China Evergrande Group debt crisis.

-

Low exposure to traditional value sectors negatively impacted performance: Energy and financials – sectors that performed well during the third quarter – are underrepresented in convertibles.

Outlook

Opportunities

-

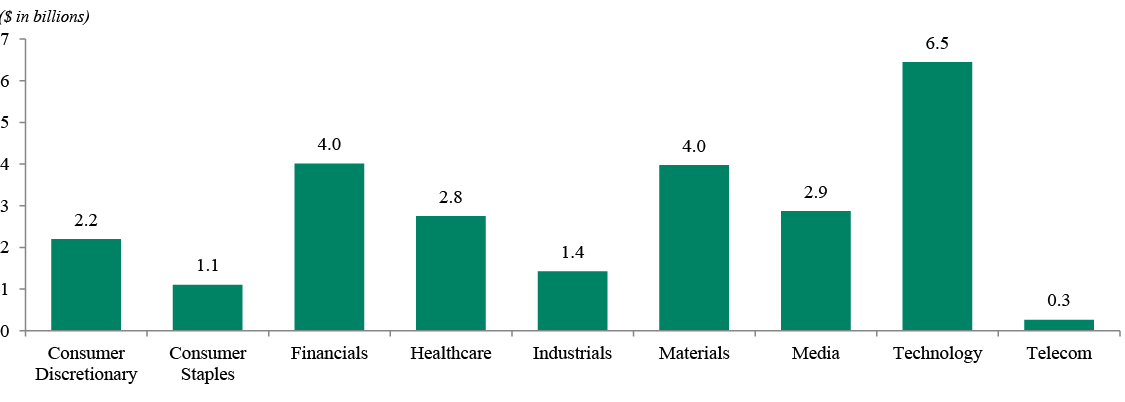

Issuance has been robust and well diversified across sectors: A broad opportunity set should help investors who are seeking to locate value under challenging market conditions (see Figure 8).

-

Falling prices could create buying opportunities: Global equity markets have sold off even though earnings in many major economies remain fairly strong. Value-oriented investors may be able to identify bargains in this environment.

Risks

-

Increasing risk in China could be a significant headwind: Investors may worry that China’s economy will slow due to shifting government priorities. Fear of contagion could cause wider selloffs in emerging market equities.

-

Growth companies could underperform: Convertibles are highly exposed to growth-oriented stocks, which may decline in value substantially if interest rates keep rising.

Figure 8: Issuance in 3Q2021 Was Well Diversified Across Sectors

Source: Bank of America

STRUCTURED CREDIT

Market Conditions: 3Q2021

U.S. CLO Issuance: $45.9bn43

European CLO Issuance: €11.4bn44

-

Corporate

-

CLO issuance has been extremely robust: August set a new monthly record, with $18.5 billion of issuance in the U.S. YTD issuance totals $126.5 billion in the U.S. and €27.0 billion in Europe.45

-

The default environment has remained benign: Improving economic fundamentals have caused defaults and default expectations to decline.

-

-

Real Estate

-

New issuance volume is very high: Non-agency CMBS issuance in September was $20.8 billion, a post-2008 monthly record.46 Single-Asset Single-Borrower (SASB) issuance is on track to reach an all-time high in 2021.47

-

The economic recovery is supporting commercial real estate fundamentals: The 30-day delinquency rate has continued to decline.

-

Outlook

Opportunities

-

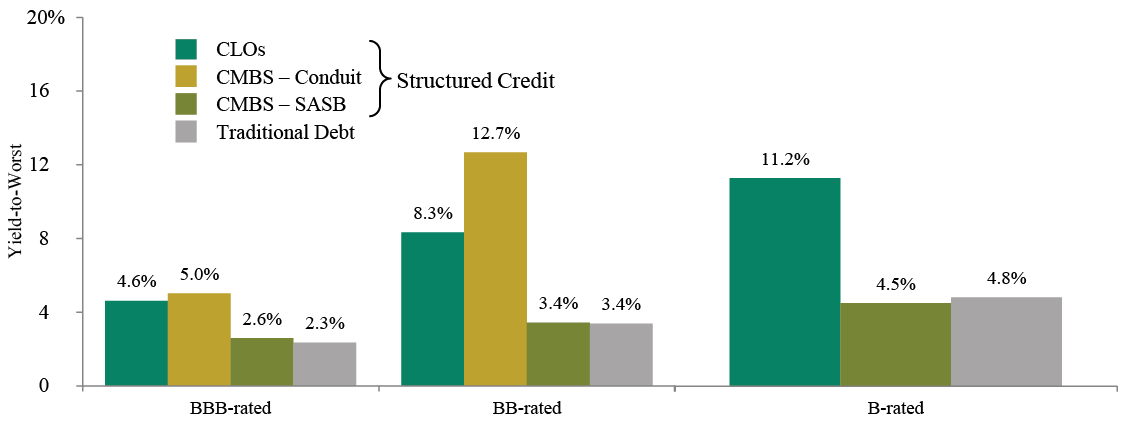

B-rated CLO debt tranches have many sources of potential value: These instruments have attractive structural and credit enhancements as well as low sensitivity to interest rates increases (see Figure 9).

-

The CLO issuance glut may continue limiting spread tightening: Yield spreads have remained fairly stable even as default rates for the underlying loans have declined.

-

CLO credit ratings will likely improve: We expect upgrades to outpace downgrades though year-end, barring an unexpected event that causes a sharp reduction in credit quality.

-

The primary market may offer attractive real estate debt opportunities: Investors may be able to earn higher yields even as underlying credit-quality improves.

Risks

-

The transition from LIBOR to SOFR48 could impact yield spreads: If issuance remains robust despite this change, yield spreads in the secondary market might widen.

-

Uncertainty about the future of offices may weigh on CRE prices: The Delta variant delayed many companies’ return-to-office plans. It’s unclear if hybrid working or full-time remote work will continue moving forward.

Figure 9: Structured Credit Offers Higher Yields Than Traditional Debt

Sources: Bloomberg Barclays Index Services, FTSE Global Markets, Credit Suisse, JP Morgan

Note: The traditional debt alternative represents a similarly rated asset class for each rating category: the Bloomberg Barclays Investment Grade Corporate Bond Index (BBB ratings), the FTSE High Yield Cash-Pay Capped Index (BB rating) and the Credit Suisse Leveraged Loan Index (B rating).

PRIVATE CREDIT

Market Conditions: 3Q2021

-

The definition of “middle market” has expanded: It’s increasingly common for U.S. businesses to borrow over $1 billion from middle-market direct lenders.

-

Borrowers may have the upper hand: Mounting competition to finance high-quality U.S. businesses has caused coupons to fall, leverage multiples to rise, and terms to become more borrower-friendly in much of the direct lending market.

-

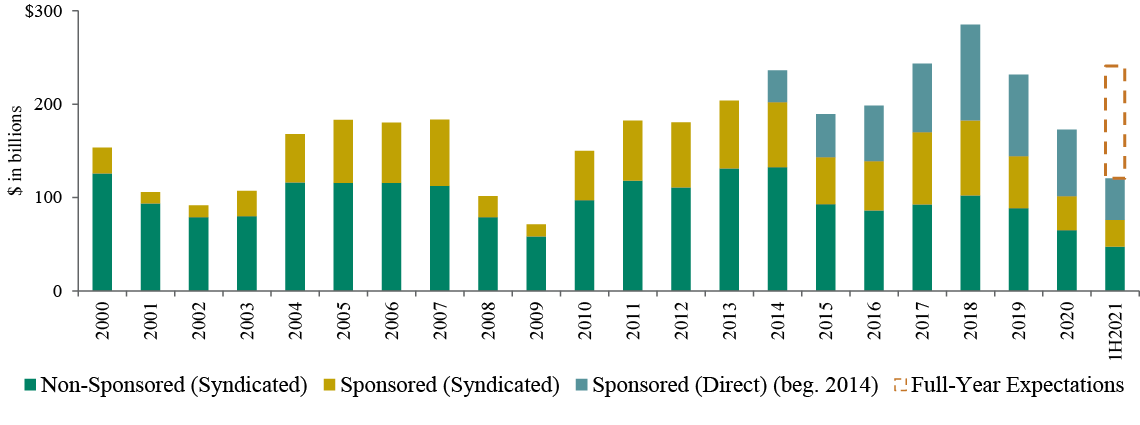

Middle-market loan volume has increased: The 2021 total is on track to reach pre-pandemic levels (see Figure 10).

-

Sustainability-linked loans (SLLs) are becoming more widely used in Europe: The terms of these loans incentivize borrowers to reach predetermined sustainability targets. Global SLL issuance topped $120 billion in 2020.49

Outlook

Opportunities

-

Deal flow should surge through year-end: This is due to ongoing improvements in businesses’ performance and investors’ abundant liquidity.

-

Fast-growing life sciences and software companies may access capital through direct lending markets: We expect significant lending opportunities will develop in these industries, driven by technological advancements and sizable research & development requirements.

-

Europe’s non-sponsor-backed market continues to offer attractive new direct lending opportunities: European borrowers outside the sponsor-backed market have traditionally had to rely on banks or informal sources of capital, but these borrowers may now turn to direct lenders as bank lending declines.

Risks

-

Businesses may continue to struggle with supply-side challenges: Shortages of labor and key inputs could impede growth and weigh on companies’ earnings – especially businesses that can’t pass rising costs onto customers.

-

Competition is intensifying: Over $25 billion of U.S. private debt capital was raised in 2Q2021.50

-

Debt-servicing costs in Europe could increase: Elevated inflation could force central banks to raise interest rates more quickly than investors anticipate. Borrowers with floating-rate liabilities might struggle to service their debts.

Figure 10: Middle-Market Loan Volume Is Recovering

Source: Preqin

Note: Full-year expectations are based on the rate of issuance in the first half of 2021.

ABOUT OAKTREE’S PERFORMING CREDIT PLATFORM

Oaktree Capital Management is a leading global alternative investment management firm with expertise in credit strategies. Our Performing Credit platform encompasses a broad array of credit strategy groups that invest in public and private corporate credit instruments across the liquidity spectrum. The Performing Credit platform, headed by Armen Panossian, has $48.7 billion in AUM and approximately 190 investment professionals.51

ENDNOTES

1 Rosenberg Research, September 30, 2021

2 Federal Reserve Bank of Kansas City

3 U.S. Bureau of Economic Analysis

4 University of Michigan Consumer Sentiment Index

5 Board of Governors of the Federal Reserve System (US); M2 is used to represent money supply

6 Federal Reserve Bank of New York

7 Federal Reserve Bank of St. Louis, as of September 30, 2021; the breakeven inflation rate is derived from 10-Year Treasury Constant Maturity Securities and 10-Year Treasury Inflation-Indexed Constant Maturity Securities.

8 JP Morgan; default rate over the last 12 months through September 30, 2021

9 JP Morgan

10 The indices used in the graph are: Bloomberg Barclays Government/Credit Index, Credit Suisse Leveraged Loan Index, Credit Suisse Western European Leveraged Loan Index (EUR Hedged), FTSE High-Yield Cash-Pay Capped Index, ICE BofA Global Non-Financial HY European Issuers ex-Russia Index (EUR Hedged), Refinitiv Global Focus Convertible Index (USD Hedged), JP Morgan CEMBI Broad Diversified (local), JP Morgan Corporate Broad CEMBI Diversified High Yield Index (Local), S&P 500 Total Return Index, and FTSE All-World Total Return Index (Local).

11 Trailing-12-Month Default Rate

12 FTSE High Yield Cash-Pay Capped Index

13 JP Morgan; gross issuance

14 JP Morgan

15 FTSE High Yield Cash-Pay Capped Index

16 JP Morgan

17 ICE BofA Global Non-Financial High Yield European Issuer, Excluding Russia Index (EUR hedged)

18 S&P Global Leveraged Commentary & Data; gross issuance

19 Credit Suisse

20 ICE BofA Global Non-Financial High Yield European Issuer, Excluding Russia Index (EUR hedged)

21 FTSE High Yield Cash-Pay Capped Index; ICE BofA Global Non-Financial High Yield European Issuer, Excluding Russia Index (EUR hedged)

22 JP Morgan

23 Credit Suisse

24 JP Morgan; gross issuance includes refinancings and resets; $142.5bn net of repricings

25 JP Morgan; excludes distressed exchanges

26 JP Morgan; excludes refinancings and resets

27 JP Morgan

28 JP Morgan

29 S&P Global Leveraged Commentary & Data; gross issuance

30 Credit Suisse

31 Credit Suisse Western Europe Leveraged Loan Index (EUR hedged)

32 JP Morgan

33 Factset

34 JP Morgan CEMBI Broad Diversified Index

35 JP Morgan Corporate Broad CEMBI Diversified High Yield Index

36 JP Morgan

37 JP Morgan

38 International Monetary Fund

39 Bloomberg U.S Financial Conditions Index; JPM EMBI Global Index Spread

40 Refinitiv Global Focus Convertible Index

41 Bank of America; gross issuance

42 Bank of America

43 JP Morgan; excludes refinancings and resets

44 JP Morgan; excludes refinancings and resets

45 JP Morgan

46 JP Morgan

47 Barclays

48 Secured Overnight Financing Rate

49 Deloitte Alternative Lender Deal Tracker Autumn 2021

50 Preqin

51The AUM figure is as of June 30, 2021 and excludes Oaktree’s proportionate amount of DoubleLine Capital AUM resulting from its 20% minority interest therein. The total number of professionals includes the portfolio managers and research analysts across Oaktree’s performing credit strategies.

NOTES AND DISCLAIMERS

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2021 OAKTREE CAPITAL MANAGEMENT E HMC ITAJUBÁ TODOS OS DIREITOS RESERVADOS.

Informações sensíveis e divulgação

Este memorando expressa as opiniões do autor na data indicada e tais opiniões estão sujeitas a alterações sem aviso prévio. A Oaktree não tem a obrigação de atualizar as informações aqui contidas. Além disso, a Oaktree não faz nenhuma representação, e não se deve assumir que odesempenho dos investimentos passados é uma indicação de resultados futuros. Além disso, onde quer que haja potencial de lucro, também existe a possibilidade de prejuízo. Este memorando está sendo disponibilizado apenas para fins educacionais e não deve ser usado para qualquer outro propósito. As informações contidas neste documento não constituem e não devem ser interpretadas como uma oferta de serviços de consultoria ou uma oferta de venda ou solicitação de compra de quaisquer títulos ou instrumentos financeiros relacionados, em qualquer jurisdição. Certas informações contidas neste documento sobre tendências econômicas e desempenho são baseadas ou derivadas de informações fornecidas por fontes terceirizadas independentes. A Oaktree Capital Management, L.P. (“Oaktree”) acredita que as fontes das quais tais informações foram obtidas são confiáveis; no entanto, não pode garantir a exatidão de tais informações e não verificou de forma independente a exatidão ou integridade de tais informações ou as suposições nas quais tais informações se baseiam. Este memorando, incluindo as informações aqui contidas, não pode ser copiado, reproduzido, republicado ou postado na íntegra ou parcialmente, em qualquer formato, sem o consentimento prévio, por escrito, da Oaktree.