Link para o artigo original: https://www.acadian-asset.com/investment-insights/equities/non-us-small-caps-a-call-to-inaction

Key Takeaways

- We extend our research on the performance of small-cap stocks in the United States1 to other developed markets (DM).

- We attribute a recent 2 ½-year bout of weakness in DM ex-U.S. small caps to a confluence of transient macro and idiosyncratic risks. Assessing their outlook afresh, we view these stocks as fairly priced relative to large caps given expectations for fundamentals.

- We conclude that investors should stay invested and active in non-U.S. small caps. This relatively inefficient market segment offers alpha generation opportunities that merit an overweight relative to the cap-weighted market portfolio.

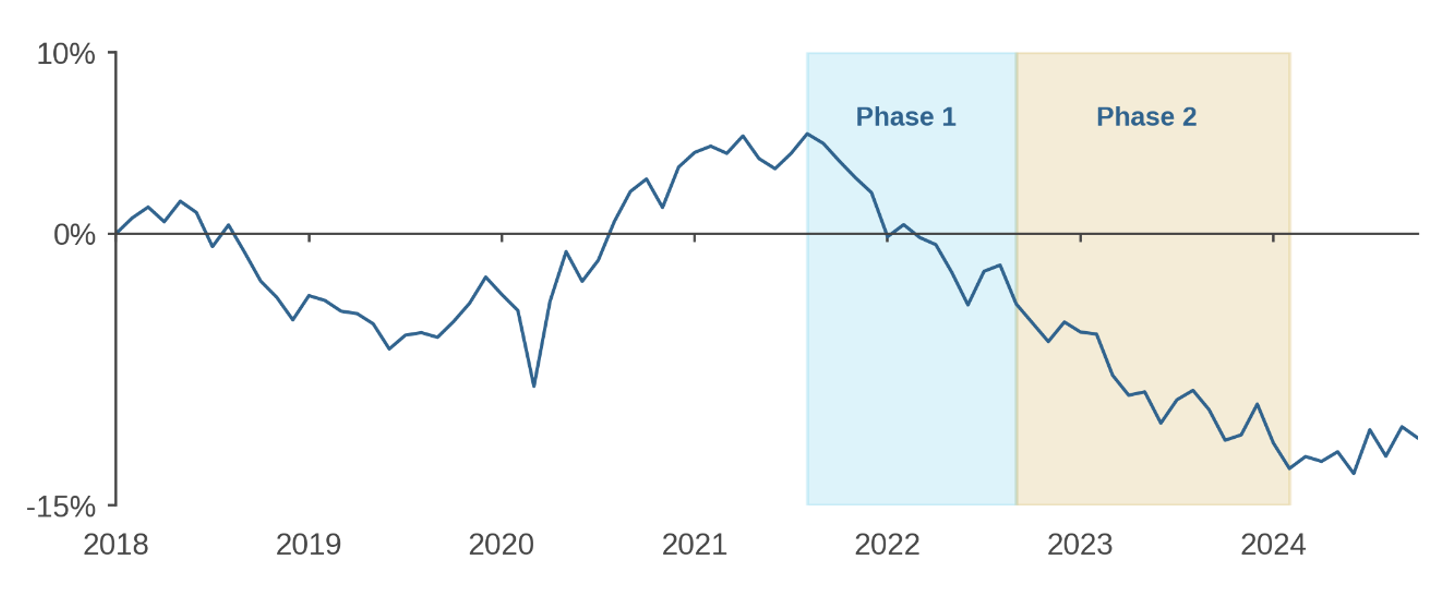

From September 2021 – February 2024, small-cap stocks in non-U.S. developed markets (DM) underperformed large caps by roughly 18% as measured by MSCI’s World ex USA benchmark indexes (Figure 1). That steady relative drawdown even led some investors to question the wisdom of non-U.S. small-cap allocations. Such reflection is natural, and it can be healthy. But asset owners have a documented tendency to make ill-timed allocation decisions by overreacting to what they see in the rear-view mirror.2 Instead, we should re-evaluate non-U.S. small caps afresh.

Figure 1: Cumulative Returns – MSCI World ex-USA Small Cap Minus MSCI World ex-USA

January 2018 – October 2024

Source: Acadian based on cumulative (summed) monthly returns from MSCI. MSCI data copyright MSCI 2024, All Rights Reserved. Unpublished. PROPRIETARY TO MSCI. For illustrative purposes only. The above does not represent investment returns generated by actual trading or an actual portfolio. It is not possible to invest in any index. Hypothetical results are not indicative of actual future results. Investors have the opportunity for losses as well as profits.

This note offers such an appraisal in three parts. First, we put the recent underperformance of DM ex-U.S. small-cap stocks into broader context. While substantial, it was not historically exceptional. Next, we analyze the drawdown’s drivers, attributing it to a confluence of macro and idiosyncratic phenomena that both differ from the causes of small-cap underperformance in the U.S. and that would have been very difficult to foresee. Finally, in assessing the outlook based on valuations and expected earnings growth, we conclude that DM ex-U.S. small caps are reasonably priced relative to large caps. We believe that allocators ought to remain both invested and active in non-U.S. small caps, embracing them as an enduring source of stock-selection alpha.

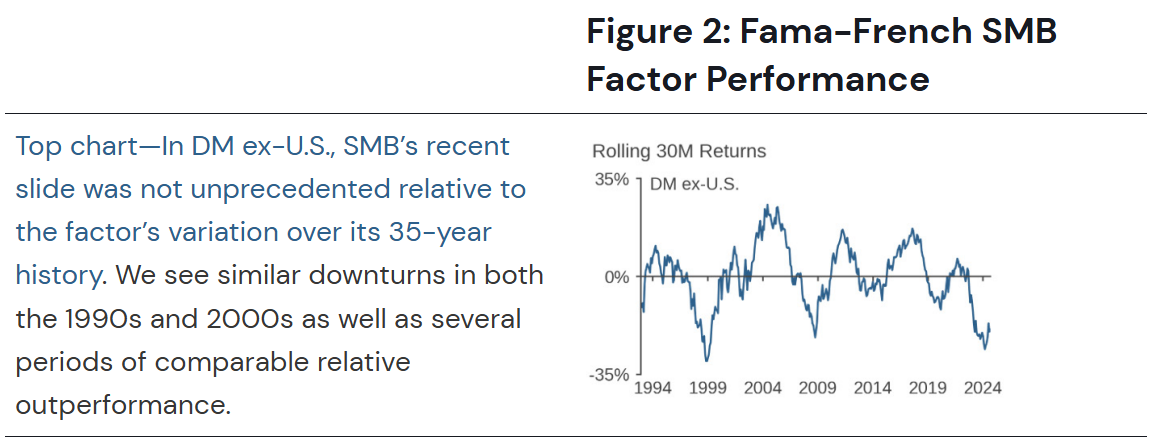

Historical Context

Over the 2 ½ years from September 2021 – February 2024, DM ex-U.S. small caps significantly underperformed large (Figure 1). Figure 2 provides context for the relative drawdown, taking advantage of the long-term history available for the well-known Fama-French small-minus-big size factor (SMB).

Causes

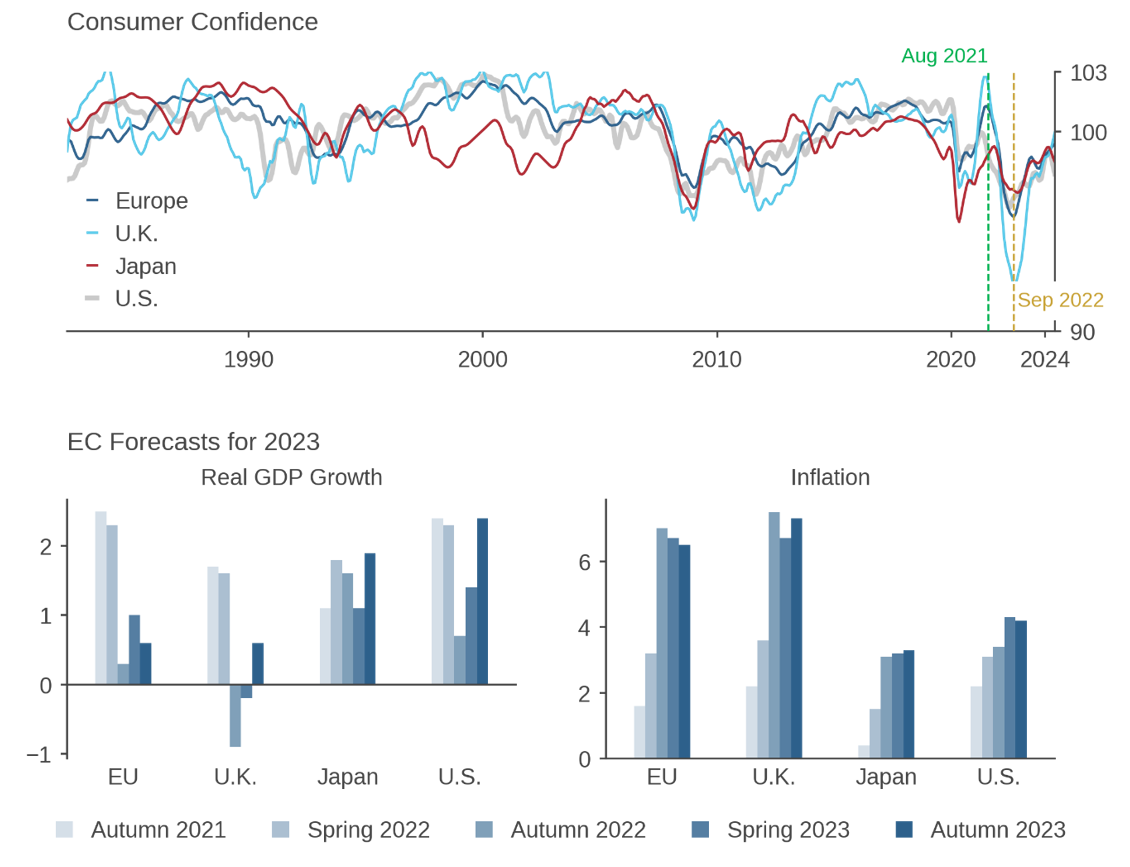

Prior to September 2021, DM ex-U.S. small-cap stocks outperformed large caps during the global speculative runup that followed the COVID selloff (Figure 1). Figure 3 offers a reminder of macro conditions that prevailed at the time. Consumer confidence was surging from COVID lows, most notably in Europe and the U.K. (top chart). Growth expectations for 2023 were healthy and inflation expectations not alarming (bottom charts).

Figure 3: The Evolution of Consumer Confidence and Economic Forecasts

Source: Acadian based on data from OECD (top chart) and the European Commission (bottom charts). For illustrative purposes only.

To understand the drivers of the subsequent underperformance of DM ex-U.S. small-cap stocks, we performed an industry-country Brinson decomposition of their performance relative to large caps. We then (subjectively) grouped both attributed and residual effects into recognizable market themes.

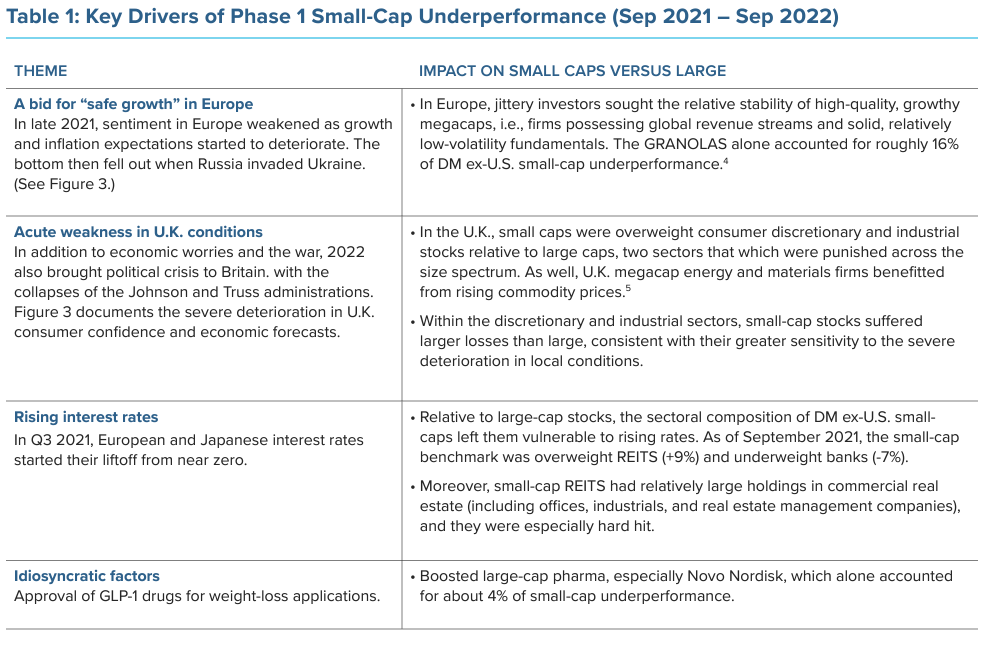

In our analysis, we separated the relative drawdown into two phases (highlighted in Figure 1) that were characterized by starkly different macro conditions. The first, from September 2021 – September 2022, was characterized by a global equity selloff as inflation reared its head, interest rates reset higher in much of the world, and Russia invaded Ukraine. While MSCI World ex USA dropped 27%, DM ex-U.S. small caps lost 34%.

We can attribute the lion’s share of that underperformance to four themes described in Table 1—a bid for large-cap “safe growth” in Europe as local economic conditions and sentiment deteriorated sharply, even more severe weakness in the U.K. amid successive political crises, the effects of rising interest rates, and idiosyncratic factors.3

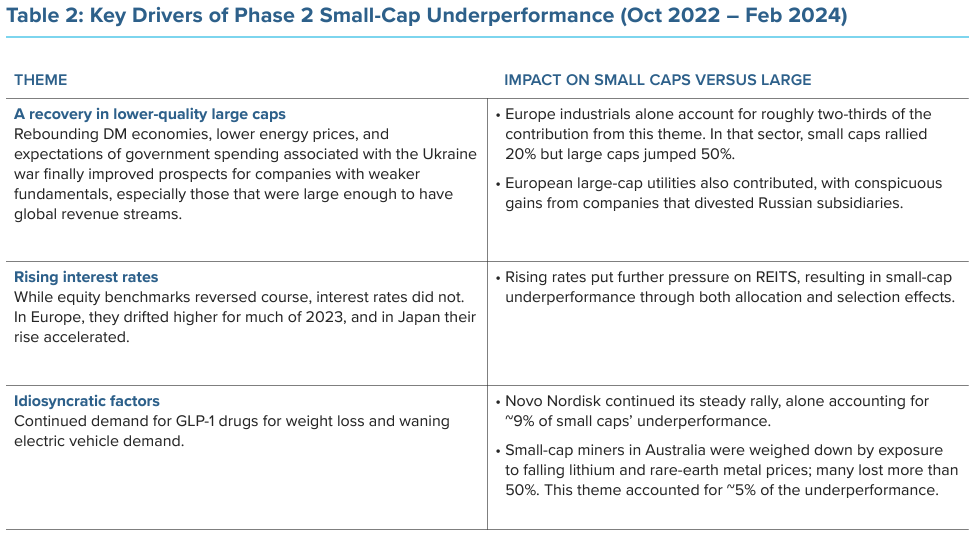

During the second phase, which started in October 2022, equity markets suddenly rebounded, yet non-U.S. small caps further extended their relative underperformance. Through February 2024, the MSCI World ex USA Index jumped 40%, while its small-cap analogue rose (only) 28%. Three themes described in Table 2 can explain of the bulk of that deficit—a recovery in lower-quality large caps, additional effects from rising interest rates (especially in Japan), and idiosyncratic effects.

We draw two inferences from the analysis summarized in the tables. First, we can largely attribute non-U.S. small-cap underperformance to transient macro risks—a confluence of economic and geopolitical phenomena— rather than to the emergence of some lasting vulnerability of small-cap companies. In the moment, the onset of an economic slowdown, generationally high inflation, the outbreak of war in Europe, and political instability in the U.K. would have been very difficult to call—and to do so faster than the market did.

Second, the causes of small-cap underperformance in the U.S. differed from its drivers in other developed markets. In contrast to the macro factors highlighted in Tables 1 and 2, in the U.S., our prior research pointed to the historical outperformance of large-cap, high-quality growth stocks (e.g., Magnificent 7) as the predominant source of relative small-cap weakness.6 The difference in drivers across regions reflects disparities in economic structures (e.g., more tech in the U.S.) and sensitivities to the specific underlying circumstances (e.g., geographical proximity to the war).

Outlook

The case for maintaining substantial non-U.S. small-cap exposure is strong. In our view, it rests on only two modest assumptions: 1) that investors ought to hold well-diversified portfolios (the cap-weighted global market portfolio being a natural starting point7) and 2) that small caps offer especially fertile ground for stock selection.

What the case does not depend on is just as important. It presumes neither that small-cap exposure offers a long-term premium nor that non-U.S. small-cap stocks currently represent a tactical allocation opportunity.

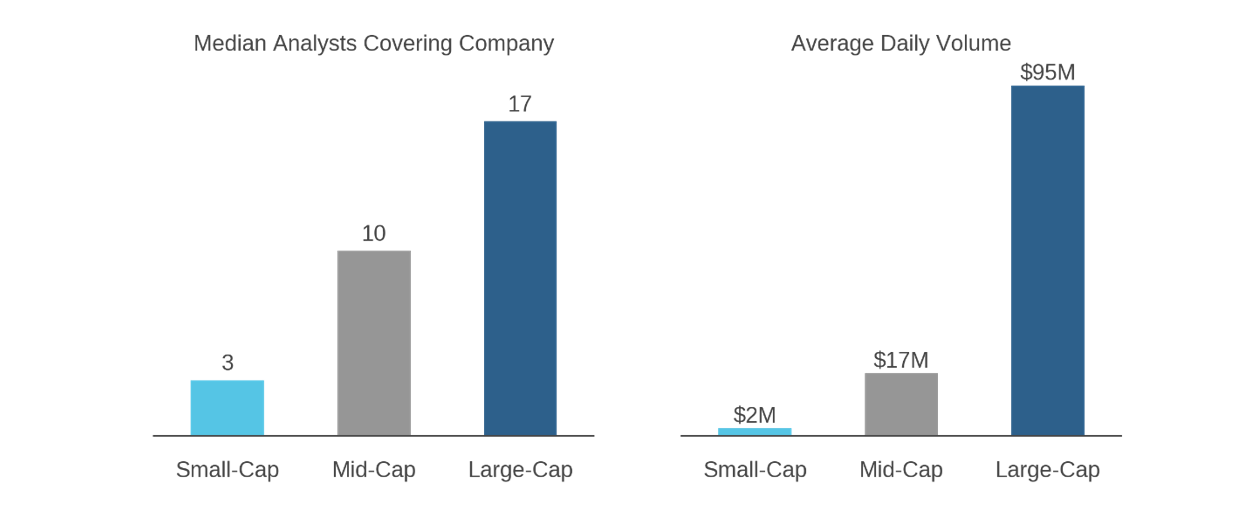

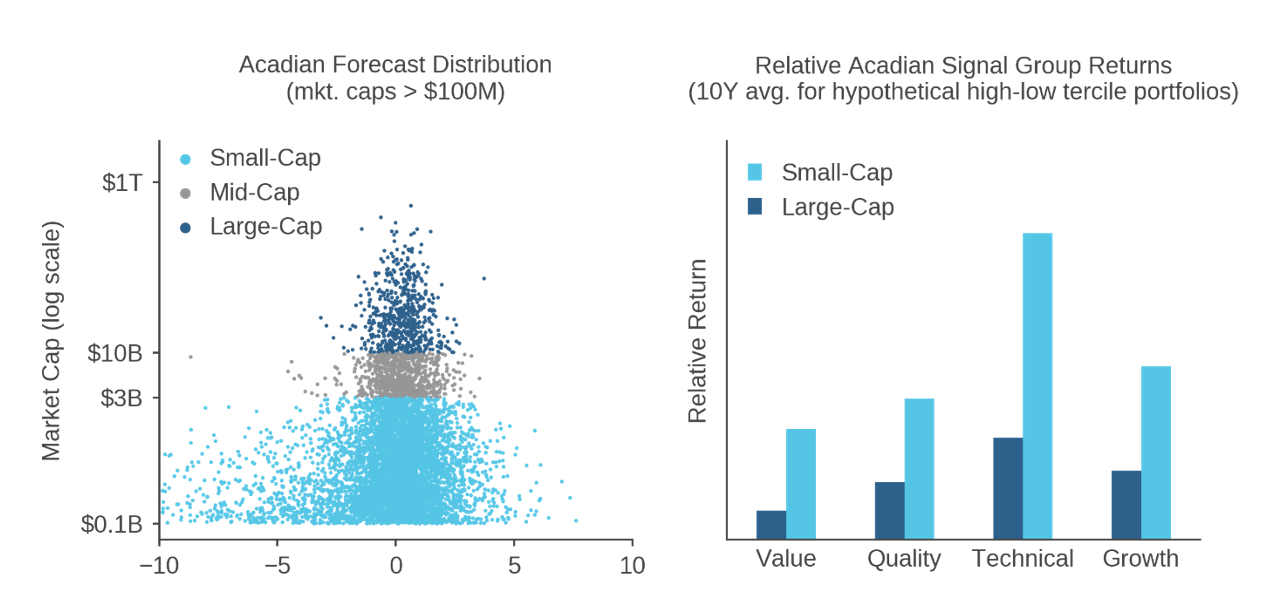

Stay InvestedNevertheless, to play devil’s advocate, could we justify a tactical underweight in non-U.S. small caps? The most intuitive thesis would be that despite their underperformance, the market hasn’t fully priced in relative deterioration of small-cap fundamentals. But we don’t believe that to be the case. The top chart in Figure 4 shows that non-U.S. small caps are now trading at a modest P/E discount to large caps for the first time in over a decade. Moreover, this shift in valuations is consistent with changes in analysts’ expectations of future earnings growth. While for years after the financial crisis analysts were forecasting higher earnings growth rates for small caps, the gap has been shrinking. In particular, analysts have expected more resilience from large-cap fundamentals in the face of the economic and geopolitical headwinds discussed above. As a result, the differential in short-term earnings growth expectations between small-caps and large is even tighter than it was in the shadow of COVID and the 2022 selloff, and long-term earnings growth forecasts are now in-line with one another.8 In view of current earnings expectations, we see the relative valuations of small- versus large-caps as fair.9 Stay ActiveAlthough we do not assume that small caps offer a return premium, we believe that they offer an enduring source of stock-selection alpha. The small-cap segment’s relatively limited information environment and lower liquidity, evidenced in Figure 5, foster persistent mispricings. |

Figure 4: DM ex-U.S. Valuations and Consensus Earnings Growth Forecasts

Source: Acadian based on index-level data from MSCI. MSCI data copyright MSCI 2024. All rights reserved. Unpublished. PROPRIETARY TO MSCI. For illustrative purposes only. |

Figure 5: DM ex-U.S. Small Caps Versus Large—Information Environment and Liquidity

Source: Acadian. There is no guarantee that forecasts will be achieved. Hypothetical returns do not represent investment returns generated by actual trading, an actual portfolio, or an investible strategy and are not indicative of future results. Every investment program has the opportunity for loss as well as profit. For illustrative use only.

Source: Acadian. There is no guarantee that forecasts will be achieved. Hypothetical returns do not represent investment returns generated by actual trading, an actual portfolio, or an investible strategy and are not indicative of future results. Every investment program has the opportunity for loss as well as profit. For illustrative use only.

Figure 6 documents how this inefficiency benefits stock selection. The left chart shows that there is greater dispersion in our return forecasts among small caps than among large. In other words, we generally find that, on an ex ante basis, small caps look like the most attractive candidates for both overweights and underweights. The right chart then shows that the stock selection signals underlying these forecasts perform materially better in small caps than in large, ex post. These findings are not unique to the DM ex-U.S. universe—small caps offer richer stock-selection opportunities than large caps, globally.

Figure 6: Benefits of Small-Cap Inefficiency for Active Investing

Acadian DM ex-U.S. Equity Universe

Source: Acadian. There is no guarantee that forecasts will be achieved. Hypothetical returns do not represent investment returns generated by actual trading, an actual portfolio, or an investible strategy and are not indicative of future results. Every investment program has the opportunity for loss as well as profit. For illustrative use only.

What are the actionable implications for asset owners? Our prescription would depend on how the investor structures their large- and small-cap allocations. Conceptually, the cleanest long-only approach is to pool them into a single all-cap active allocation. To the extent that alpha dispersion is generally higher among small caps, such a portfolio will naturally tend to overweight small-cap stocks relative to the market portfolio. In the absence of a binding risk constraint on size exposure, the degree of that overweight can fluctuate as the forecasted opportunity set for stock selection among small caps expands or contracts relative to large caps.10

The pooled allocation framework clarifies the prescription for investors who instead separately allocate to large and small strategies in DM ex-U.S. (and other regions). First, stay active in small caps because that’s where the stock selection opportunity set is richest. Second, as a general rule, overweight active small caps relative to large. The degree of that small-cap overweight should depend on investor-specific views and constraints, including expectations of small-cap alpha and tolerance for small-cap risk.11

Conclusion

In our view, it would be understandable but unwise for institutional investors to reduce their allocations to small caps in non-U.S. developed markets based on their performance over the past few years. Currently, we think that these stocks, in aggregate, look reasonably priced relative to larger caps. Over the long run, we would encourage allocators to view small-cap exposure as an uncompensated risk factor that is well worth taking to exploit stock-selection opportunities in a relatively inefficient segment of the market. Based on a forward-looking perspective, stay both invested and active in non-U.S. small caps.

Endnotes

- U.S. Small-Cap Performance: Relatively Bad but Absolutely Fine, Acadian, June 2024.

- Ang, Andrew, Amit Goyal, and Antti Ilmanen, “Asset allocation and Bad Habits.” Rotman International Journal of Pension Management 7, issue 2 (Fall 2014): 16-27.

- Across DM ex-U.S., there is a strong relationship across firms between their market capitalizations and revenue derived from their home region. For companies with market caps from $1-$10B, $10-50B, and $50B+, medians are 78%, 53%, and 44%, respectively.

- GRANOLAS is an acronym for high-quality European bellwethers that analysts coined in April 2020 (GlaxoSmithKline, Roche, ASML, Nestle, Novartis, Novo Nordisk, L’Oreal, LVMH, AstraZeneca, SAP, Sanofi). References to these and other companies should not be interpreted as recommendations to buy or sell specific securities. Acadian and/or the authors of this paper may hold positions in one or more securities associated with these companies.

- As of September 2024, MSCI’s U.K. Large Cap Index had a 21.7% in the two sectors versus only 8.3% for the Small Cap analogue. Source: MSCI factsheets.

- See U.S. Small-Cap Performance: Relatively Bad but Absolutely Fine, previously cited.

- The Capital Asset Pricing Model justifies a high bar for deviations from the market portfolio. Heaton, Polson, and White (2017) provide an alternative rationale. Based on a model calibrated to historical data, they argue that randomly selecting a subset of the market portfolio, similar to taking strategic underweights, can significantly increase the probability of long-term underperformance. See Heaton, J. B., N. G. Polson, and J. H. White, “Why Indexing Works.” Applied Stochastic Models in Business and Industry 33, issue 6 (November/December 2017): 690-693.

- To see earnings growth expectations back on an equal footing with large is consistent with longer-term history. Since 1990, price-to-cash-earnings multiples of non-U.S. small caps have both exceeded and trailed those of large caps for extended periods. In other words, market prices have not, over the long term, consistently impounded higher expected long-term earnings growth rates for small caps than large.

- If anything, the macro environment provides us with some near-term optimism regarding the relative prospects of small caps outside of the United States. Figure 3 shows that in Europe, Japan, and especially the U.K., consumer confidence has rebounded significantly from historically weak levels of 2022, surpassing what we see in the U.S. (Figure 3, top chart).

- To be clear, the variation in aggregate small-versus-large weighting does not require the forecasting model to include an explicit “small-versus-large” component. The aggregate small-cap weighting would also depend on variation in risk and transaction costs among small stocks versus large.

- Investors who are sensitive to size risk should consider long-short extensions as an alternative to long-only portfolios. While taking leverage involves risk and complexity, relaxing the long-only constraint allows for more flexibility to exploit the small-cap opportunity set by offsetting attractive longs with attractive shorts. For further discussion, see Thinking Broadly: Improving Active Performance Via Systematic Extensions, Acadian, October 2023.

Legal Disclaimer

These materials provided herein may contain material, non-public information within the meaning of the United States Federal Securities Laws with respect to Acadian Asset Management LLC, BrightSphere Investment Group Inc. and/or their respective subsidiaries and affiliated entities. The recipient of these materials agrees that it will not use any confidential information that may be contained herein to execute or recommend transactions in securities. The recipient further acknowledges that it is aware that United States Federal and State securities laws prohibit any person or entity who has material, non-public information about a publicly-traded company from purchasing or selling securities of such company, or from communicating such information to any other person or entity under circumstances in which it is reasonably foreseeable that such person or entity is likely to sell or purchase such securities.

Acadian provides this material as a general overview of the firm, our processes and our investment capabilities. It has been provided for informational purposes only. It does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or to purchase, shares, units or other interests in investments that may be referred to herein and must not be construed as investment or financial product advice. Acadian has not considered any reader’s financial situation, objective or needs in providing the relevant information.

The value of investments may fall as well as rise and you may not get back your original investment. Past performance is not necessarily a guide to future performance or returns. Acadian has taken all reasonable care to ensure that the information contained in this material is accurate at the time of its distribution, no representation or warranty, express or implied, is made as to the accuracy, reliability or completeness of such information.

This material contains privileged and confidential information and is intended only for the recipient/s. Any distribution, reproduction or other use of this presentation by recipients is strictly prohibited. If you are not the intended recipient and this presentation has been sent or passed on to you in error, please contact us immediately. Confidentiality and privilege are not lost by this presentation having been sent or passed on to you in error.

Acadian’s quantitative investment process is supported by extensive proprietary computer code. Acadian’s researchers, software developers, and IT teams follow a structured design, development, testing, change control, and review processes during the development of its systems and the implementation within our investment process. These controls and their effectiveness are subject to regular internal reviews, at least annual independent review by our SOC1 auditor. However, despite these extensive controls it is possible that errors may occur in coding and within the investment process, as is the case with any complex software or data-driven model, and no guarantee or warranty can be provided that any quantitative investment model is completely free of errors. Any such errors could have a negative impact on investment results. We have in place control systems and processes which are intended to identify in a timely manner any such errors which would have a material impact on the investment process.

Acadian Asset Management LLC has wholly owned affiliates located in London, Singapore, and Sydney. Pursuant to the terms of service level agreements with each affiliate, employees of Acadian Asset Management LLC may provide certain services on behalf of each affiliate and employees of each affiliate may provide certain administrative services, including marketing and client service, on behalf of Acadian Asset Management LLC.

Acadian Asset Management LLC is registered as an investment adviser with the U.S. Securities and Exchange Commission. Registration of an investment adviser does not imply any level of skill or training.

Acadian Asset Management (Singapore) Pte Ltd, (Registration Number: 199902125D) is licensed by the Monetary Authority of Singapore. It is also registered as an investment adviser with the U.S. Securities and Exchange Commission.