Link para o artigo original: https://www.lordabbett.com/en-us/financial-advisor/insights/investment-objectives/2025/a-bull-market-in-uncertainty.html

A Bull Market in Uncertainty

- Tariffs have introduced an unexpected fiscal shock that could be a drag on GDP growth and earnings.

- Several important indicators show a surge in uncertainty and bearishness—historically these periods are followed by resilient recoveries over time.

- We believe active management and a focus on high-quality companies with durable competitive advantages are a prudent approach in this environment.

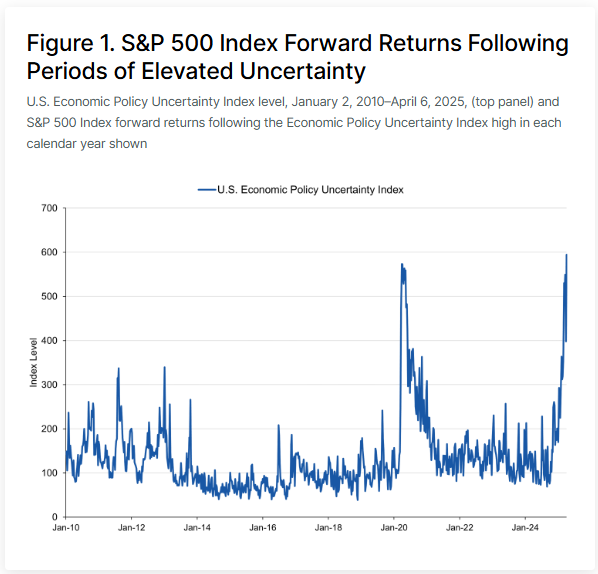

The new administration’s actions have created a surge in policy and economic uncertainty as measured by the Baker, Bloom, and Davis uncertainty index.1 This index has been in production for 40 years and last reached such heights during March 2020. Following periods of elevated levels of policy uncertainty, the U.S. equity market, represented by the S&P 500 Index®, has provided above-average forward returns, shown in Figure 1.

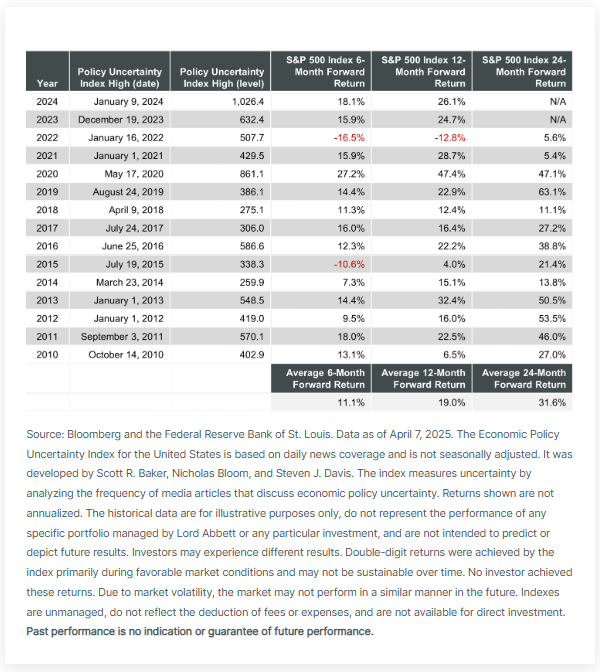

Policy uncertainty has translated into pervasive bearishness. There are many surveys that measure investor sentiment, but the preeminent measure is the Investors Intelligence Bull/Bear Ratio, a survey that has been conducted with a consistent methodology since its inception in 1964. It is unusual for bears to outnumber bulls in this survey: Bears have outnumbered bulls only eight times in the last 15 years.2 History shows that whenever bears outnumber bulls, investors have been rewarded with above-average returns over the next six and 12 months. The last two times this threshold was breached was in late 2022, which marked the end of the inflation-induced bear market, and the COVID-induced lows of March 2020.

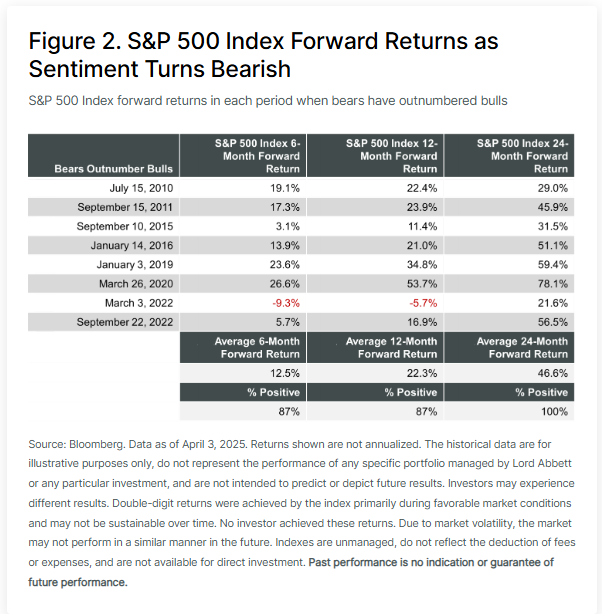

Finally, what investors are feeling (uncertainty), and what they are saying (sentiment surveys) is showing up in what they are doing. Specifically, the number of stocks trading above their 150-day moving averages has reached extreme levels, shown in Figure 3. When investors are selling indiscriminately, as these measures imply, investors’ returns over the next six and 12 months have been above average.

Putting it all together, history has shown that equity market volatility has often been followed by resilient recoveries. These periods of anxiety don’t resolve immediately, but the patient, opportunistic investor has historically reaped the benefits over the next six months, 12 months, and 24 months.

We believe Lord Abbett’s active investment portfolios are well positioned for the current environment. A unifying principle for our equity strategies is the emphasis on high-quality companies with durable competitive advantages, led by skilled management teams. This approach spans both growth and value stocks in U.S. and non-U.S. markets.

We have a differentiated approach to identify what we believe are quality investments in that the quantitative metrics we use to define quality are not static. What works to identify quality in a value universe is not the same set of metrics that one should use in a growth universe. Furthermore, the set of metrics in a global or emerging markets universe cannot be the same as what one uses for a U.S.-focused portfolio. Our portfolio teams work closely with our quantitative experts in an effort to make sure that our expression of quality is consistent with the universe that we are interrogating and aligns with our investment philosophies. This is just one of the many ways our investment teams seek to deliver excess returns on behalf of our clients.

About the Author

Essas informações podem conter declarações de previsões que envolvem riscos e incertezas; os resultados reais podem diferir materialmente de quaisquer expectativas, projeções ou previsões feitas ou inferidas em tais declarações de previsões. Portanto, os destinatários são advertidos a não depositar confiança indevida nessas declarações de previsões. As projeções e/ou valores futuros de investimentos não realizados dependerão, entre outros fatores, dos resultados operacionais futuros, do valor dos ativos e das condições de mercado no momento da alienação, restrições legais e contratuais à transferência que possam limitar a liquidez, quaisquer custos de transação e prazos e forma de venda, que podem diferir das premissas e circunstâncias em que se baseiam as perspectivas atuais, e muitas das quais são difíceis de prever. O desempenho passado não é indicativo de resultados futuros.