Link para o artigo original: https://www.oaktreecapital.com/insights/insight-commentary/market-commentary/performing-credit-quarterly-3q2024-who-are-the-lenders-now

Performing Credit Quarterly 3Q2024: Who Are the Lenders Now?

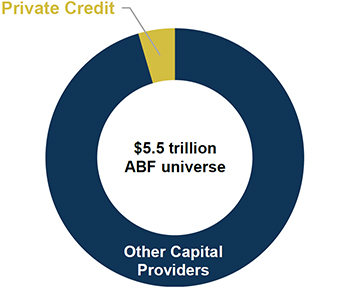

Figure 1: Private Credit Involvement in ABF Is Nascent

Source: Oliver Wyman estimate1

The Regulatory Squeeze

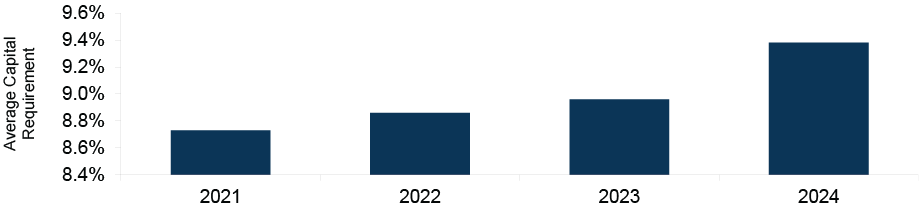

Ongoing efforts to reduce the systemic risk presented by banking institutions have manifested in a succession of regulatory changes. One of the most impactful facets of these regulations is the requirement for banks to hold more capital, which may improve bank liquidity levels but also reduce their return on equity. (See Figure 2.) Because this capital is measured as a percentage of the bank’s assets (i.e., outstanding loans), activity that grows the asset side of the equation increasingly necessitates careful consideration. Importantly, asset base is calculated on a risk-weighted basis, meaning riskier lending activities, such as loans to small businesses or against repayments from individual borrowers, require banks to hold more capital.

Figure 2: The Average Capital Requirements for Large U.S. Banks Have Steadily Increased

Source: The Federal Reserve2

The implementation of these new regulations, primarily enacted via the Basel III accords, has steadily progressed since the Global Financial Crisis but is imminently coming to a head in the form of the Basel III endgame. This refers to the culmination of the Basel III rules, with a 2025 compliance date for large U.S. banks, followed by a three-year transition period. The most stringent rules would fall on the largest, and therefore most systemically important, banks: the 37 largest banks in the U.S. would meet the proposed $100 billion asset threshold, representing over 75% of all bank assets in the country.3

Along with higher capital requirements, the Basel III endgame will constrain the usage of internal bank models for calculating risk-weighted assets, with a standardized model effectively able to overrule internal outputs. Unrated assets – common within the ABF universe – face a 100% risk weighting regardless of their true risk,4 requiring banks to hold an outsized amount of capital, thus potentially rendering this lending unfavorable for banks.

Additional Headwinds

Increases to regulatory capital only add to the pressure on banks from quantitative tightening and a string of sector-specific stresses, including the decline of brick-and mortar retailers and an increase in vacant office buildings.

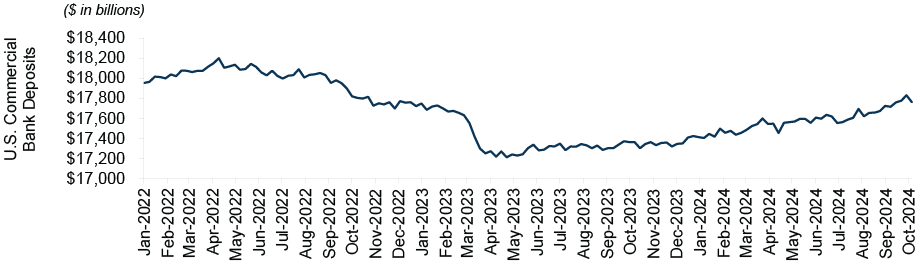

One challenge new to bank lenders has been the unreliability of deposits. (See Figure 3.) While bank loans often have long maturities, deposits can be withdrawn almost immediately. This isn’t a worry for private credit lenders, who offer their investors only limited liquidity in order to ensure stable capital. Based on the practice of fractional reserve banking – in which banks retain a portion of customer deposits as reserves and lend the rest – a reduction in deposits is naturally followed by a reduction in lending activity.

The 2023 regional banking crisis highlights the liquidity risk inherent in this model. The deposits held by Silicon Valley Bank, the headline casualty, were lent out via long duration bonds, which decreased in value as interest rates rose. When customers sought to withdraw their deposits, this asset-liability mismatch was ultimately fatal for the bank. Given this instability, banks have become more measured when providing the illiquid financing associated with ABF.

Figure 3: Deposit Instability Has Made Bank Lending More Challenging in Recent Years

Source: Board of Governors of the Federal Reserve System (U.S.)

Bank Reprioritization

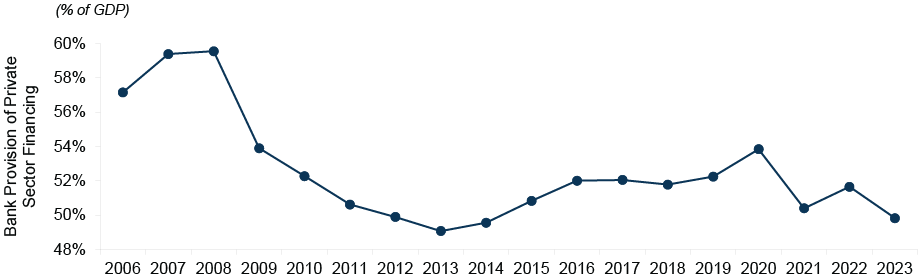

The upshot of this? Banks find certain lending activities increasingly inefficient, with no end in sight to this shift. As a result of tougher capital charges, banks are either (a) refocusing lending activity on their biggest (and safest) client base or (b) targeting lending toward situations where they stand to earn fees and attract deposits. Lending is estimated to have accounted for only 21% of banks’ total revenue in 2023, down from 26% in 2019.5 In the U.S., bank lending as a percentage of GDP has dropped by nearly ten percentage points since the Global Financial Crisis. (See Figure 4.)

Figure 4: Bank Provision of Credit Has Declined as a Percentage of U.S. GDP

Source: The World Bank

A Financing Void

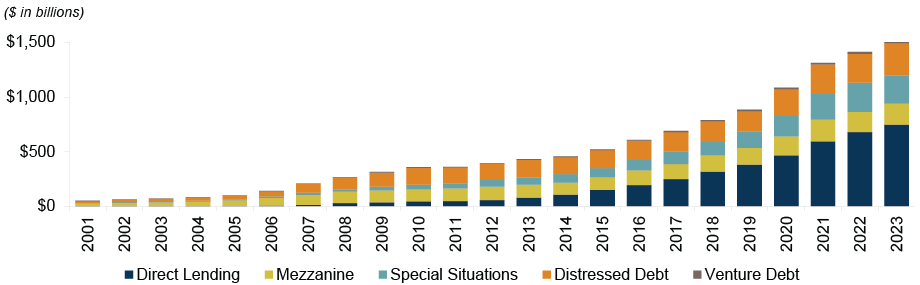

As banks continue to shift their focus, what does this mean for alternative lenders? It’s important to note that alternative lenders currently play a smaller role in ABF than in mainstream direct corporate lending. Banks started to retreat from corporate direct lending quite some time ago, and direct lending presented a more natural extension for leveraged finance practitioners, who flocked to the space. Many companies now issue both public senior loans and private loans, with the due diligence processes for these types of loans having a high degree of overlap. Direct lenders continue to dominate the private debt landscape, with nearly $200bn of combined dry powder to deploy.6 On the other hand, ABF represents a new frontier for most managers, with additional barriers to entry. (See Figure 5.)

Figure 5: Private Credit Capital Has Grown Substantially but Remains Tilted Toward Mainstream Direct Lending

Source: Preqin

We believe the most underserved portion of the ABF universe is the ‘‘core’’ segment that sits between senior, investment grade lending and the opportunistic end of the risk spectrum. The investment grade portion of ABF, with the lowest perceived risk and lowest expected returns, is well addressed by insurance buyers and other investment grade-focused ABF platforms. U.S. insurers hold a whopping $8.5 trillion7 in total cash and invested assets; they value the cash flows generated by ABF, but regulation demands an investment grade rating to ensure favorable capital treatment. For most ABF packages, investment grade ratings only extend to senior financing, therefore leaving mezzanine and junior capital financing to other parties. Additionally, many transactions don’t support ratings at all (e.g., short-term facilities, which are incompatible with rating agency criteria). In short, insurance capital won’t be able to fill the void left by retreating banks.

Meanwhile, private equity, opportunistic credit investors, and specialty finance platforms require higher returns than those generally offered by the core portion of ABF. As a result, we anticipate alternative lenders will increasingly provide essential capital in the core ABF segment where traditional senior lenders, such as insurers and banks, are unable or unwilling to operate.

ABF Sector Spotlight

Among the wide range of esoteric ABF verticals, we’ve chosen to showcase three sectors we believe may be at the center of the ABF evolution.

(1) Aircraft Leasing: Fleeting Supply

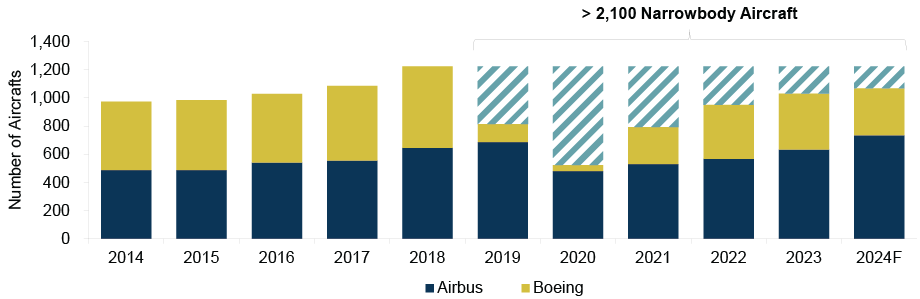

Since 2019, aircraft production has significantly declined, largely due to delays and quality control issues at major manufacturers like Boeing, Airbus, and Pratt & Whitney. (See Figure 6.) This has led to unprecedented order backlogs and higher aircraft lease rates.

Global airline traffic has now surpassed pre-pandemic levels, and aircraft producers have been unable to meet the increased demand. Due to the extremely limited supply of new planes, airlines have no choice but to put aside idealized fleet planning and prioritize leasing and purchasing midlife assets.

We believe the current supply-demand imbalance, which is expected to persist until 2030 or beyond, presents a rare opportunity for appropriately resourced aircraft investors to step in and provide financing to proven aircraft leasing platforms and originators.

Figure 6: 2024 Aircraft Deliveries Are Likely to Remain Below 2017 Levels

Source: AerCap, as of May 2024 Note: Represents narrowbody aircraft (i.e., single-aisle airliners)

(2) Synthetic Risk Transfer (SRT): Coming to America

Synthetic risk transfer (i.e., when a bank enters into a contract with an investor, whereby the investor assumes the risk of any future losses in a credit pool in exchange for coupon income) allows banks to “sell” risk without taking the immediate balance sheet impact of a below-par sale. Many banks lent aggressively at the historically low rates from 2009-21 and now find themselves with a balance sheet full of low-interest, long-duration assets.

Selling these assets in today’s elevated interest rate environment would create a book equity loss, potentially impacting capital ratios and market perception, as well as endangering the bank’s relationship with the underlying borrowers. Banks are increasingly using SRT as a tool to effectively amortize the “cost” of that sale over several years.

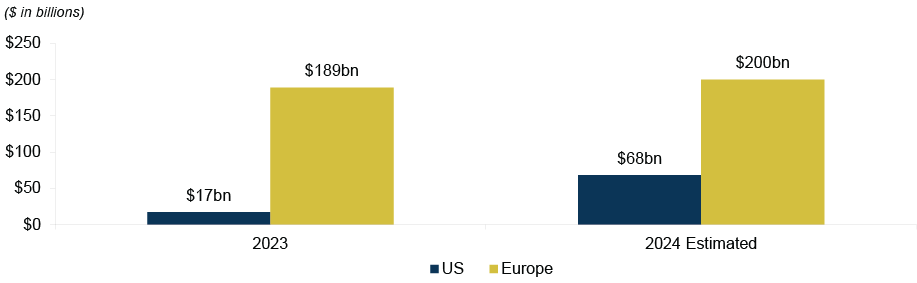

In 2023, SRT issuance in Europe was over ten times the volume in the U.S.8 It is estimated that the U.S. market will quickly begin to catch up, with a fourfold increase projected for 2024. (See Figure 7.) Moreover, we believe the most attractive SRT opportunities will be those associated with pools of niche assets that require specialized knowledge, avoiding the overly competitive auctions associated with ‘‘vanilla’’ SRT, such as corporate loans or subscription facilities.

Figure 7: SRT Volume Is Projected to Grow Substantially in the U.S.

Source: Bank of America estimates, as of March 2024

(3) Consumer Credit: Lender Exodus

The unsecured consumer sector underwent a negative performance shock in 2022-23 after experiencing two years of robust performance, rapid origination growth, and inexpensive funding. This downturn was driven by inflated credit scores, machine learning models misled by pandemic-related stimulus measures, and high inflation. Subsequent to this volatility, many capital providers have exited this space entirely.

Due to the deterioration in performance, originators have tightened their credit underwriting standards and increased Annual Percentage Rates, which has created a more favorable outlook for new investments as performance begins to improve.

In the unsecured consumer sector, we’ve seen loans originated through personal interaction (e.g., in-branch, at medical offices, or at point of sale) perform significantly better than those originated online or without personal interaction. Therefore, we believe investors, when looking to provide financing to thoughtful consumer lenders or purchase discounted pools of consumer loans, should favor loans originated through personal interaction and used to finance essential spending.

What Next?

We believe we’re witnessing a permanent, secular shift in the financing ecosystem, as ABF transforms from an asset class dominated by banks and insurers into an investible alternative credit opportunity. We don’t expect banks to meaningfully loosen credit standards and regain their lost market share in the near future, and we expect insurers to maintain their focus on lower-returning, investment grade lending. Thus, we believe asset-backed finance isn’t a short-term opportunity, but rather the next frontier of private credit.

However, ABF shouldn’t be viewed as a homogenous, easily accessible asset class. While we believe experienced managers can control risk, we believe those who don’t appreciate the complexity of the asset class – or who fail to conduct adequate due diligence – are at risk of getting burnt.

Credit Markets: Key Trends, Risks, and Opportunities to Monitor in 4Q2024

(1) The Trajectory for Interest Rates in the U.S. Remains Unclear Despite the First Cut

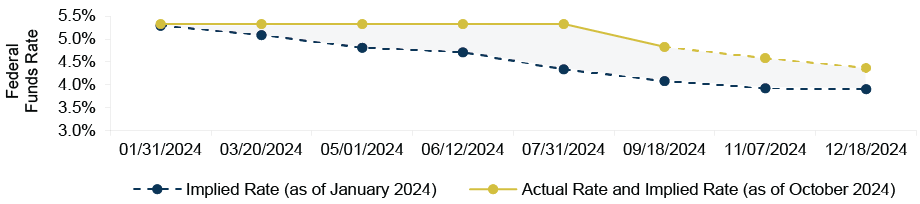

In September 2024, the U.S. Federal Reserve reduced interest rates by 50 bps, bringing the federal funds rate to the new target range of 4.75-5.00%. This ended the interest rate hiking cycle that began in March 2022 and resulted in a 525 bps rise over the period. Given the September rate cut was largely priced in by market participants, the impact on Treasury yields was limited.

The Fed’s action was long awaited after a series of ‘‘false starts’’ to the rate cutting cycle, whereby many market participants priced in aggressive interest rate cuts that then didn’t materialize. (See Figure 8.) Credit investors seeking to drive performance through duration exposure were left frustrated, while the best returns were often achieved through high-income assets with limited interest rate sensitivity, including senior loans and structured credit.

Figure 8: The Actual Fed Funds Rate in 2024 Has Diverged from the Market Prediction at the Start of the Year

Source: Bloomberg

This significant cut was followed by exceptional U.S. jobs data at the start of October. Total nonfarm payroll employment in September increased by more than 250,000 jobs, well above the consensus expectation of roughly 140,000 jobs.9 This apparent affirmation of the resilience of the U.S. labor market, and subsequent increase in uncertainty surrounding the trajectory of interest rates, led to a rise in Treasury yields.

For those that bet heavily on aggressive interest rate cuts, this proved to be another tough pill to swallow. As Howard Marks often reminds us, investors should always be conscious of where we are in the market cycle – but never make bets based on macroeconomic predictions.

(2) Favorable Conditions May Support a Rise in M&A and LBO Volume

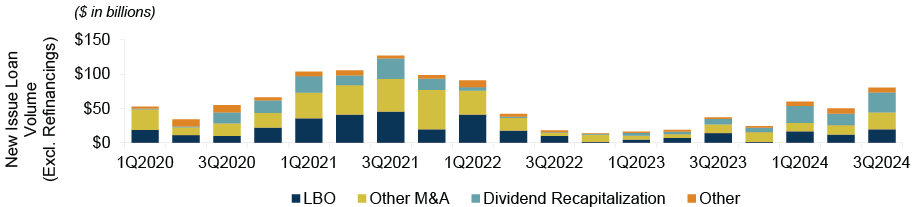

Primary leveraged finance markets experienced a meaningful surge late in the third quarter of 2024, following the usual summer lull: senior loan and high yield bond issuance was robust in September, with over $140 billion of combined volume, a 70% increase from the same period in 2023.10

Debt issuance over the last two years has been dominated by refinancings as private equity sponsors have found limited exit opportunities for their portfolio companies. The headwinds to LBO and M&A activity are well known: elevated financing costs after a historic rise in interest rates, stubbornly high equity valuations, concerns about economic growth, and, in more recent months, the uncertainty around the 2024 U.S. Presidential election.

Some of these challenges now seem to be abating. While interest rates will likely remain elevated, the first interest rate cut from the Fed in September marked the end of the hiking cycle. At the same time, the economic outlook (especially in the U.S.) appears more robust, with strong labor market data and a surprisingly resilient consumer. Another catalyst is limited partners pressing their investment managers for cash: distributions from closed-end funds have been delayed, with the median hold period for exited private equity portfolio companies recently exceeding seven years, leaving LPs pushing for exits.11

With this, we’re beginning to see signs of life in the M&A and LBO space. Importantly, the third quarter of 2024 saw the highest amount of non-refinancing loan issuance since 1Q2022. (See Figure 9.) Moreover, more LBOs were funded through the broadly syndicated loan market than through direct lending during the period.12 This shift was largely due to significant investor demand, particularly from CLOs, which has reduced the cost of financing in the public market. We anticipate that once the uncertainty surrounding the U.S. election is removed, a new wave of M&A and LBO activity could emerge.

Figure 9: New Loan Supply Is Showing Signs of Recovery

Source: PitchBook LCD

(3) Private Debt Defaults Remain Limited, But Pay Attention to PIK

Performance in the private debt markets has remained strong in 2024, with business development companies (BDCs) returning an exceptional 10.7% year-to-date.13 While we’ve seen an uptick in defaults this year, the current default rate of 2.0% remains manageable, and below the default rate in the broadly syndicated loan market.14

What has kept private debt markets so buoyant? Firstly, companies have been supported by surprisingly resilient consumer expenditure. Secondly, sponsors have proactively reduced costs in their portfolio companies and passed on input price increases to end consumers. These sponsors have also collaborated with lenders to promptly address potential liquidity issues.

However, there are still several reasons for lenders to exercise caution. Issuers of floating-rate debt are likely to be exposed to higher borrowing costs for longer than they’d previously anticipated, as the market consensus around the trajectory for interest rate cuts has proven to be overly ambitious. This may put further pressure on interest coverage, particularly given that we’ve seen slowing EBITDA growth among middle-market companies.

As borrowers begin to feel the impact of these mounting pressures, we’ve observed a shift toward alternative financing solutions. The most prominent is the rise in borrowers turning to payment-in-kind (PIK) instead of making their coupon payments in cash. For example, the percentage of PIK income for BDCs has risen by nearly 200 bps since 2023. (See Figure 10.) This can alleviate liquidity pressure on borrowers, but it presents a risk for lenders who (a) miss out on regular cash payments and (b) face uncertainty regarding delivery of accrued interest or potential equity upside. While not all PIK is inherently bad, it remains crucial for managers to diligently monitor these developments.

Figure 10: PIK Constitutes an Increasing Percentage of Private Credit Income

Source: Fitch Ratings

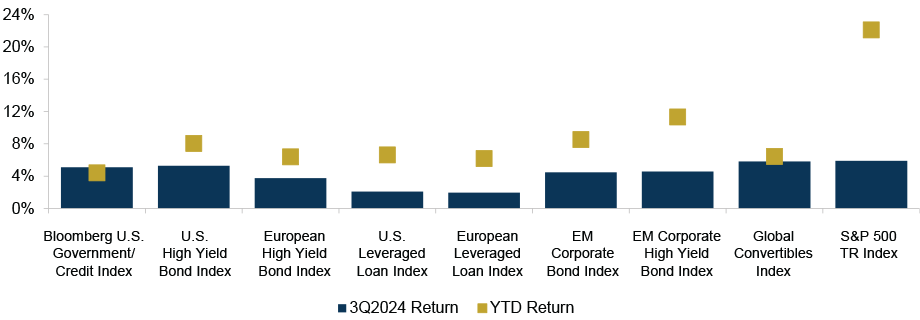

Assessing Relative Value

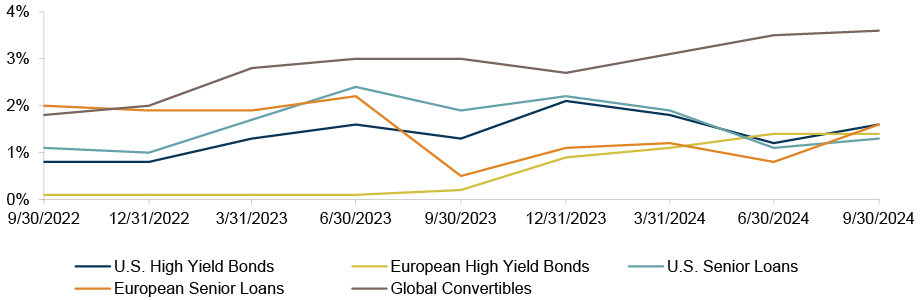

Performance of Select Indices

As of September 30, 2024 Source: Bloomberg, Credit Suisse, ICE BofA, JP Morgan, S&P Global, Thomson Reuters15

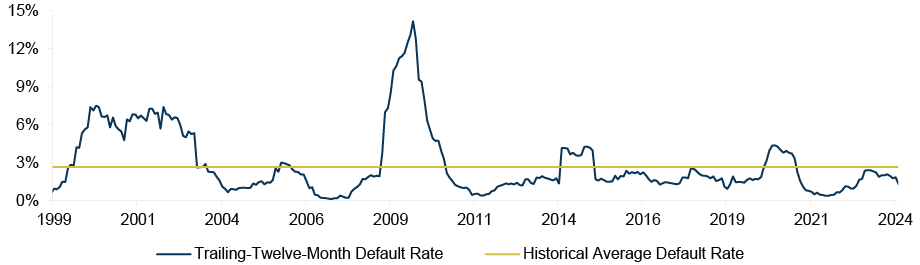

Default Rates by Asset Class

Source: JP Morgan for high yield bonds; Credit Suisse for loans through 2Q2023, UBS since 3Q2023; Bank of America for Global Convertibles Note: Data represents the trailing-12-month default rate; excludes distressed exchanges

Strategy Focus

High Yield Bonds

Market Conditions: 3Q2024

U.S. High Yield Bonds – Return: 5.3%16 | LTM Default Rate: 1.6%17

-

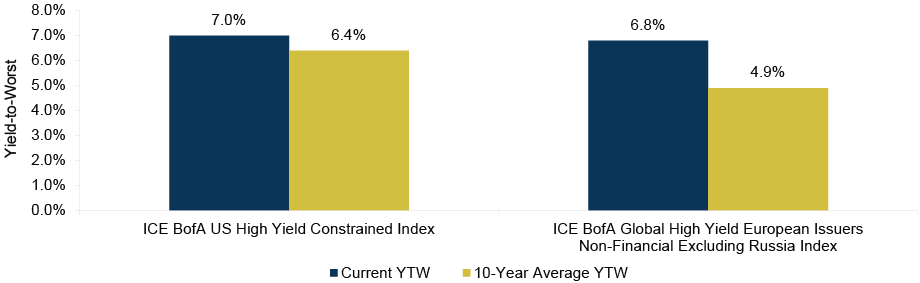

Yield spreads contracted moderately in 3Q2024: At quarter-end, yield spreads remained near the low end of the historically normal range of 300–500 bps.18

-

Yields in the asset class remain elevated: They decreased slightly in 3Q2024 but remain above the ten-year median. (See Figure 11.) Nearly 30% of high yield bonds still had yields above 7% at the end of the third quarter, compared to less than 7% at the beginning of 2022. 19

-

CCC-rated bonds outperformed: The lowest credit rating category returned 10.1% for the period. Meanwhile, B- and BB-rated bonds returned 4.6% and 4.3%, respectively. The outperformance of CCC-rated bonds derived partly from gains in the satellite and telecom sectors.

European High Yield Bonds – Return: 3.8%20 | LTM Default Rate: 1.4%21

-

The asset class strengthened modestly in 3Q2024: Returns were largely driven by coupon income and price appreciation.

-

The lowest-quality segment of the market outperformed: CCC-rated bonds returned 5.7% for the period, compared to 3.9% and 3.3% for B-rated and BB-rated bonds, respectively.

-

High yield bonds are priced at a discount to par: Investors have the opportunity to earn capital appreciation, along with elevated coupon income.

-

The high yield bond market continues to offer attractive yields: While spreads have narrowed slightly, yields remain elevated, providing investors with the opportunity to earn attractive contractual returns.

-

Default risk remains low: Quality in the asset class is high: BB-rated bonds make up more than half of the market in the U.S. Meanwhile, maturities through 2026 have declined considerably over the last year.

-

There is significant uncertainty surrounding the upcoming U.S. presidential election: Policy changes could quickly impact corporate taxes, the budget deficit, and U.S. national debt.

-

Elevated inflation and high labor costs may impair issuers’ fundamentals: While inflation has slowed, many input costs remain high.

-

Heightened geopolitical risk may put pressure on economic growth: Geopolitical tensions, including the wars in Ukraine and the Middle East and complicated China/U.S. relations, could potentially lead to volatility within the global supply chain.

Figure 11: The High Yield Bond Markets Still Offer Attractive Yields

Source: ICE BofA US High Yield Constrained Index and ICE BofA Global Non-Financial High Yield European Issuer, Excluding Russia Index, as of September 30, 2024

Senior Loans

Market Conditions: 3Q2024

U.S. Senior Loans – Return: 2.1%22 | LTM Default Rate: 1.3%

-

U.S. senior loan prices increased in 3Q2024: Positive performance was supported by high coupon income and continued demand from CLO issuance.

-

Gross issuance in the asset class remained strong: Loan primary market activity continued at a steady pace in the third quarter, bringing issuance for the year above $900bn, which is already the highest volume seen since 2017. But refinancings/repricings have continued to dominate issuance.

European Senior Loans – Return: 2.0%23 | LTM Default Rate: 1.6%

-

European loans generated a positive return during the third quarter: Strong coupon income continued to drive returns as prices remained relatively flat during the period.

-

Lower-quality loans outperformed: CCC-rated loans, the lowest-quality portion of the senior loan market, returned 4.9% in the period, while B- and BB-rated loans returned 1.7% and 2.0%, respectively.

-

High coupons could continue to attract investors: Unless there is a substantial decline in reference rates, floating-rate loans will likely remain compelling throughout the remainder of 2024.

-

The default outlook appears manageable: Default rates in the U.S. and European loan markets are projected to rise but are likely to stay below their non-recessionary averages. (See Figure 12.) This is primarily because of the limited volume of maturities in the next two years and the availability of other sources of capital (e.g., rescue financings).

-

Loans may experience less volatility than other asset classes because of loans’ stable buyer base: CLOs, the primary holders of leveraged loans, have limited selling pressure, and the asset class tends to attract long-term institutional investors because of the lengthy cash settlement period.

-

Recovery rates are well below the historical average: The increased prevalence of loan-only capital structures has caused average recovery rates in the asset class to decline to 42%.24 We expect this trend to continue through this default cycle.

-

Declining interest rates may reduce appetite for floating-rate assets: While interest rates remain above their ten-year average, additional interest rate cuts could have a negative impact on demand for floating-rate assets.

Figure 12: Default Rates Are Still Below the Historical Non-Recessionary Average

Source: J.P. Morgan, as of September 30, 202425

Investment Grade Credit

Market Conditions: 3Q2024

Return: 5.8%26

-

Investment grade debt generated positive returns in 3Q2024: This was largely driven by the decline in Treasury yields, as the U.S. Federal Reserve commenced its interest rate cutting cycle.

-

Higher-quality credit outperformed: AAA-rated corporate bonds outperformed the lowest-rated segment of the investment grade market by over 60 bps in the third quarter. This was primarily because the higher-rated segment has the longest average duration within the asset class.

-

Issuance remained robust during the quarter: Gross issuance of investment grade bonds in the period totaled $428bn, bringing year-to-date issuance to more than $1.3tn.27 Demand for investment grade credit remained more than sufficient to absorb the surge in supply; the primary market currently has an average oversubscription rate of 3.7x.

-

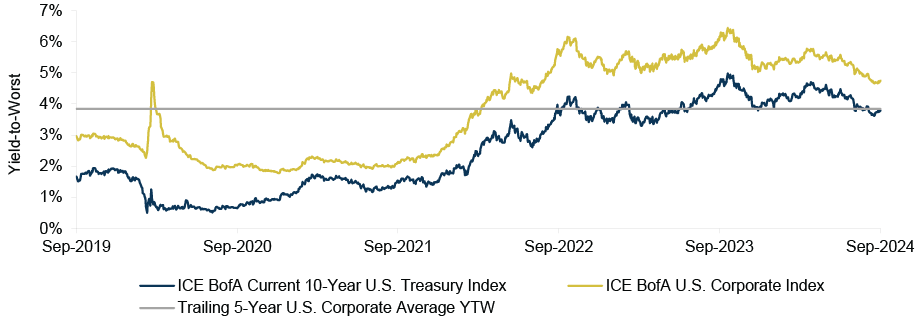

Investment grade corporate debt yields are still elevated: Yields in the asset class ended the quarter at 4.8%, which is meaningfully higher than the five-year average. (See Figure 13.)

-

Investment grade debt may benefit if economic activity slows: The asset class has a higher average credit rating and duration than high yield bonds, and so may outperform if risk sentiment declines, yield spreads widen, and interest rates fall.

-

Fixed-rate asset classes may suffer if interest rates don’t decrease as much as currently anticipated: At quarter-end, market participants were projecting two to three additional cuts in the remainder of 2024, and five more in 2025. If the Fed takes a more patient approach, there will likely be volatility in many of the more rate-sensitive credit markets.28

-

If interest rates decline substantially, there could be reduced demand for low-yielding fixed income securities: Investors that need to achieve a particular yield may gravitate from investment grade credit toward asset classes offering higher yields. However, the flipside of this dynamic is the potential for inflows from money market investors; this may be significant given money markets have risen to $6.4tn in volume.29

Figure 13: Investment Grade Bond Yields Remain Well Above the Five-Year Average

Source: Bloomberg

Emerging Markets Debt

Market Conditions: 3Q2024

EM Corporate High Yield Bonds – Return: 4.6%30

-

EM high yield corporate debt recorded a positive return for the eighth consecutive quarter: Following this strong performance, the EM index now offers a yield below 8% for the first time since the U.S. Federal Reserve began raising interest rates in early 2022. The spread premium versus U.S. high yield is near the historical average; however, spreads in the asset class are currently around the tightest they’ve been in six years.

-

Global policy has been supportive: In September, the Fed reduced interest rates for the first time in over four years, developed market economic data was resilient, and China announced a wave of new stimulus measures, which boosted investor sentiment regarding global growth.

-

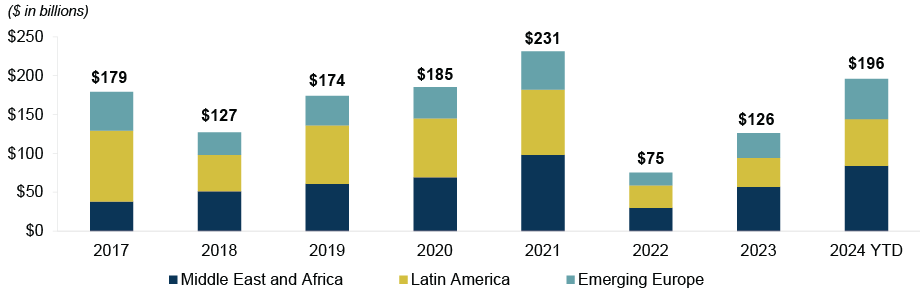

Declining interest rates contributed to a surge in bond issuance: EM companies issued $64 billion of new bonds in September, the highest volume since June 2021. Despite moderate EM debt fund outflows, there was ample investor appetite for issuance, including debt issued by debut and lower-rated companies. (See Figure 14.)

-

Political risks relating to Latin America and the U.S. election are lurking: Central banks in Latin America have kept real interest rates high (i.e., Brazil, Mexico, and Colombia are all above 5%), largely due to regional currency weaknesses and ongoing domestic challenges. The uncertainty around the U.S. election has affected investment in many emerging markets, given its potential impact on critical global policies, including trade tariffs and U.S./China relations.

-

The investable universe is expanding: Improved financing conditions have supported additional debt-financed transactions, including M&A activity and the emergence of new borrowers.

-

Even with the recent rally, there are attractive opportunities across the diverse regions and industries within EM: These various segments of EM are at different stages in the credit cycle and exposed to idiosyncratic risks.

-

The EM default outlook is moderate: The EM default rate is below 3% year-to-date, representing a decline from the high levels recorded in recent years.

-

Market stability may have increased investor complacency: A surge in EM issuance, including of lower-quality bonds, may suggest complacency following a relatively calm period across key markets.

-

A global economic slowdown could put pressure on EM export-driven economies: Unresolved factors, including the impact of Chinese economic stimulus and the outcome of U.S. elections, could reshape global trade dynamics.

-

Geopolitical tensions may have negative long-term effects on EM debt capital flows: Investor confidence in EM credit could decline if ongoing conflicts escalate or if China/U.S. relations worsen.

Figure 14: EM Corporate Bond Issuance in Many Regions Has Meaningfully Recovered

Source: JP Morgan, as of October 11, 2024

Global Convertibles

Market Conditions: 3Q2024

Return: 5.8%31 | LTM Default Rate: 3.5%32

-

Convertible bond prices increased in the third quarter upon strong equity market performance: Stocks in Asia ex-Japan and the United States generated the largest gains, primarily due to (a) several new stimulus measures recently announced by policymakers in China and (b) the U.S. Federal Reserve’s 50-bps interest rate cut. As a result, small-cap shares, as well as other equities that previously struggled in the face of higher interest rates, outperformed during the period.

-

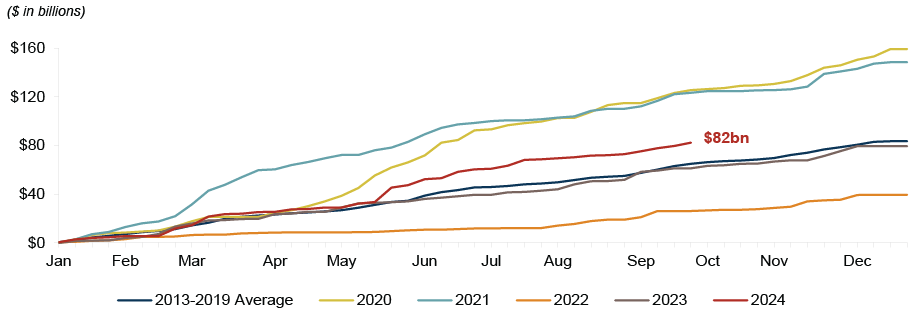

Primary market activity remained healthy: New issuance of global convertibles totaled $21.9bn across 42 new deals in 3Q2024. The majority of issuance was concentrated in the U.S. and Asia ex-Japan, and primarily within the technology and financial sectors.

-

The size and quality of the convertible bond market has continued to improve: In an elevated interest rate environment, companies seeking new capital or those looking to refinance straight debt have increasingly turned to the convertibles market, where coupons are lower. Thus far in 2024, new issuance of global convertible bonds is running at the fastest pace since 2021. (See Figure 15.) Importantly, nearly 70% of the volume this year has come from companies with large equity market capitalizations.33

-

The equity rally is expanding: The rally in U.S. equity markets – which was primarily concentrated among a handful of large technology companies (i.e., the “Magnificent Seven”) – broadened in the third quarter, with over 60% of S&P 500 companies outperforming the index, compared to around 25% in the first half of the year.34

-

Numerous trends threaten to slow global economic growth and weigh on equity prices: These include concerns about sticky inflation, uncertainty surrounding the U.S. presidential election, and heightened geopolitical risk.

Figure 15: New Issuance of Global Convertibles Has Been Running at the Fastest Pace Since 2021

Source: BofA Global Research

Structured Credit

Market Conditions: 3Q2024

Corporate – BB-Rated CLO Return: 2.7%35 | BBB-Rated CLO Return: 2.3%36

-

Collateralized Loan Obligation spreads have tightened but still offer a premium over equivalent corporate bonds: BBB-rated CLO spreads tightened to 358 bps at the end of 3Q2024, but this still represents an attractive premium over BBB-rated corporate bonds.

-

Activity in the primary market decelerated in 3Q2024 but remains robust: CLO issuance recorded its weakest quarter of the year but remains meaningfully above the level of the same period in 2023. Issuance of CLOs in the U.S. exceeded $41bn in the period, up from $23bn in 3Q2023. Issuance in Europe totaled €11bn compared to €8bn in 3Q2023.37

Real Estate – BBB-Rated CMBS Return: 4.6%38

-

Real estate structured credit recorded positive performance in 3Q2024: The asset class continues to benefit from improving investor sentiment around the real estate sector, which has been largely driven by expectations of further interest rate cuts over the next year.

-

Valuations in the CRE market varied by sector: Green Street’s Commercial Property Price Index39 increased by 1.6% quarter-over-quarter but decreased by 3.1% year-over-year.40 The office subsector index declined by 8.2% YoY.41 While most sectors experienced annual declines in the low single digits, many increased modestly on a quarterly basis, suggesting that the market may be stabilizing.

-

Primary market activity continues to accelerate meaningfully: CMBS issuance in 2024 is already more than double last year’s modest volume: year-to-date, total private label issuance of commercial mortgage-backed securities is over $75bn, an increase of 140% compared to the same period in 2023.

-

Corporate structured credit offers higher average yields than traditional credit asset classes: CLO debt has shown significant resilience throughout various market dislocations since the Global Financial Crisis, including the pronounced fluctuations in 2020 and 2022-23, as evidenced by their low long-term loss rates. (See Figure 16.)

-

New loan supply may increase in the near future: As central banks continue along the path of cutting interest rates, M&A and LBO activity, which has been lackluster in recent years, could pick up, creating a supply of new loans.

-

While valuations in the CMBS market appear to be stabilizing, the bank market remains sidelined due to an excess of CRE loans made before 2022: The bank pullback has created a significant void of capital for borrowers seeking to acquire or refinance existing assets, presenting an opportunity for non-bank lenders with available capital and limited problems in their existing portfolios.

-

Limited supply of new loans may lead to underwriting compromises: Limited new loan supply but ample demand means some CLO managers may fill warehouses with low quality paper.

-

Weakness in the office sector may persist: The sector continues to face multiple headwinds, and its performance will likely continue to weigh on real estate structured credit indices throughout the remainder of the year.

Figure 16: Structured Credit Has Historically Had Lower Loss Rates than Traditional Credit

Source: JP Morgan Research (High Yield Bonds, 1978-2024), J.P. Morgan Research (Leveraged Loans, 1998-2024), Moody’s (CLOs, 1993-2023, updated annually), J.P. Morgan Research (SASB CMBS and large loan floaters, 1996-2024), as of September 30, 2024, updated quarterly unless otherwise stated.

Private Credit

Market Conditions: 3Q2024

-

Private credit’s susceptibility to creditor-on-creditor violence is lower than the broadly syndicated loan market: This is largely due to (a) the absence of multiple classes of debt in most transactions, (b) tighter credit documentation, and (c) strong relationships between borrowers, sponsors, and lenders, given that direct lending typically has a smaller lender base. Thus, sponsors often find it difficult to execute aggressive liability management exercises (i.e., the transactions behind creditor-on-creditor violence), as most lenders lend at par and secondary trading is less common.

-

European private credit deal volume and average size continue to rise: Deal volume rebounded meaningfully in the second quarter: the asset class recorded 246 deals during the period, a 110% increase compared to the first quarter and the highest since tracking began in 2012.42 In the first half of the year, strategic bolt-on acquisitions represented 36% of transactions across Europe (excluding the UK).43

-

Fixed-rate junior capital can help investors lock in today’s elevated yield: Roughly 50% of today’s all-in yield on floating-rate debt is attributable to base rates; the yield on senior direct lending portfolios is therefore expected to fall if interest rates continue to decline. However, the fixed-rate nature of junior capital solutions offers investors the opportunity to maintain higher yields moving forward.

-

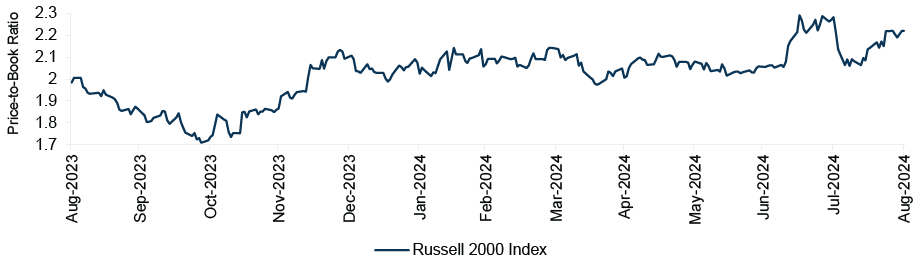

Recovering equity valuations may signal an upcoming rise in non-sponsor activity: Stabilizing earnings in the Russell 2000 index, a proxy for U.S. middle-market companies, could boost lender confidence and make non-sponsored companies more attractive for direct lending. (See Figure 17.) Moreover, non-sponsored companies may also seek financing for growth, acquisitions, or other strategic initiatives, creating more opportunities for customized financing solutions from direct lenders.

-

Pricing is near all-time tights and the dispersion of risk has grown: The average pricing on a senior sponsored first lien loan is currently hovering around SOFR+4.75%. Deals executed at higher yields today are typically more intricate and come with greater risk. Some credit managers are willing to assume more risk to sustain the yields offered during the same period last year. However, we believe caution remains warranted as the incremental yield may not justify the additional risk.

-

Interest rate reductions may cause borrowers to increase leverage levels: As interest rates decrease, companies will benefit from lower interest expense on floating-rate debt. As debt becomes relatively cheaper, some sponsors may look to increase leverage levels to boost their returns on equity, which in turn increases risk.

Figure 17: Non-Sponsor Activity May Increase as Equity Valuations Stabilize

Source: Bloomberg, as of August 31, 2024

![]()

Oaktree Capital Management is a leading global alternative investment management firm with expertise in credit strategies. Our Performing Credit platform encompasses a broad array of credit strategy groups that invest in public and private corporate credit instruments across the liquidity spectrum. The Performing Credit platform, headed by Armen Panossian, has $95.3 billion in AUM and approximately 190 investment professionals.44

Endnotes

- 1Oliver Wyman, Private Credit’s Next Act, April 2024. The $5.5 trillion figure represents the U.S. asset-backed finance market, excluding real estate.

- 2Average of CETI requirements for large U.S. banks, derived from the Federal Reserve Board’s capital framework for bank holding companies.

- 3Brookings, FDIC, March 2024.

- 4Moody’s, February 2023.

- 5Oliver Wyman, Into The Great Unknown For Wholesale Banking, 2023 full-year forecast.

- 6Preqin, March 2024.

- 7National Association of Insurance Commissioners Capital Markets Special Report.

- 8Bank of America, as of March 2024.

- 9United State Department of Labor.

- 10PitchBook.

- 11PitchBook, 2023.

- 12PitchBook.

- 13Cliffwater BDC Index, as of October 18, 2024.

- 14KBRA DLD Direct Lending Index, trailing 12-month issuer default rate.

- 15The indices used in the graph are Bloomberg Government/Credit Index, Credit Suisse Leveraged Loan Index, Credit Suisse Western European Leveraged Loan Index (EUR hedged), ICE BofA US High Yield Index, ICE BofA Global Non-Financial HY European Issuers ex-Russia Index (EUR Hedged), Refinitiv Global Focus Convertible Index (USD Hedged), JP Morgan CEMBI Broad Diversified Index (Local), JP Morgan Corporate Broad CEMBI Diversified High Yield Index (Local), S&P 500 Total Return Index.

- 16ICE BofA US High Yield Constrained Index for all references to U.S. High Yield Bonds, unless otherwise specified.

- 17JP Morgan for all U.S. default rates, unless otherwise specified. This figure excludes distressed exchanges.

- 18The normal range refers to the average range over the last 25 years.

- 19ICE BofA US High Yield Constrained Index. Percentages are based on the market value of debt.

- 20ICE BofA Global Non-Financial High Yield European Issuer, Excluding Russia Index (EUR hedged) for all references to European High Yield Bonds, unless otherwise specified.

- 21UBS for all European default rates, unless otherwise specified.

- 22Credit Suisse Leveraged Loan Index for all data in the U.S. Senior Loans section, unless otherwise specified.

- 23Credit Suisse Western Europe Leveraged Loan Index (EUR Hedged) for all data in the European Senior Loans section, unless otherwise specified.

- 24JP Morgan, LTM average rate, as of September 30, 2024. Default figures exclude distressed exchanges.

- 25TXU was removed from J.P. Morgan’s twelve-month default rate calculation in April 2015 resulting in a meaningful decrease in the rate in March 2015.

- 26ICE U.S. Corporate Index for all data in this section, unless otherwise specified.

- 27BofA Securities IG Syndicate Deal Recap.

- 28As of September 30, 2024.

- 29Investment Company Institute Money Fund Assets, as of September 30, 2024.

- 30JP Morgan Corporate Broad CEMBI Diversified High Yield Index for all data in this section unless otherwise specified. The emerging markets debt section focuses on dollar-denominated high yield debt issued by companies in emerging market countries.

- 31Refinitiv Global Focus Convertible Index for all performance data, unless otherwise indicated.

- 32Bank of America for all default and issuance data in this section, unless otherwise specified.

- 33Defined by Bank of America as issuers with underlying equity market capitalizations of $10 million or more.

- 34Reuters.

- 35JP Morgan CLOIE BB Index.

- 36JP Morgan CLOIE BBB Index.

- 37JP Morgan for all data in this section, unless otherwise specified.

- 38Bloomberg US CMBS 2.0 Baa Index Total Return Index Unhedged Index.

- 39Index tracks the pricing of institutional-quality commercial real estate.

- 40Green Street Commercial Property Index, as of September 30, 2024.

- 41Green Street Commercial Property Index, as of September 30, 2024.

- 42Deloitte Private Debt Deal Tracker Autumn 2024.

- 43Ibid.

- 44The AUM figure is as of September 30, 2024 and excludes Oaktree’s proportionate amount of DoubleLine Capital AUM resulting from its 20% minority interest therein. The total number of professionals includes the portfolio managers and research analysts across Oaktree’s performing credit strategies.

Notes and Disclaimers

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2024 Oaktree Capital Management, L.P.

Informações sensíveis e divulgação

Este memorando expressa as opiniões do autor na data indicada e tais opiniões estão sujeitas a alterações sem aviso prévio. A Oaktree não tem a obrigação de atualizar as informações aqui contidas. Além disso, a Oaktree não faz nenhuma representação, e não se deve assumir que o desempenho dos investimentos passados é uma indicação de resultados futuros. Além disso, onde quer que haja potencial de lucro, também existe a possibilidade de prejuízo. Este memorando está sendo disponibilizado apenas para fins educacionais e não deve ser usado para qualquer outro propósito. As informações contidas neste documento não constituem e não devem ser interpretadas como uma oferta de serviços de consultoria ou uma oferta de venda ou solicitação de compra de quaisquer títulos ou instrumentos financeiros relacionados, em qualquer jurisdição. Certas informações contidas neste documento sobre tendências econômicas e desempenho são baseadas ou derivadas de informações fornecidas por fontes terceirizadas independentes. A Oaktree Capital Management, L.P. (“Oaktree”) acredita que as fontes das quais tais informações foram obtidas são confiáveis; no entanto, não pode garantir a exatidão de tais informações e não verificou de forma independente a exatidão ou integridade de tais informações ou as suposições nas quais tais informações se baseiam. Este memorando, incluindo as informações aqui contidas, não pode ser copiado, reproduzido, republicado ou postado na íntegra ou parcialmente, em qualquer formato, sem o consentimento prévio, por escrito, da Oaktree.