Link para o artigo original : https://www.lordabbett.com/en-us/institutional-investor/insights/markets-and-economy/are-high-yield-investors-getting-properly-paid-for-default-risk-.html

Are High Yield Investors Getting Properly Paid for Default Risk?

Amid a softening U.S. economy, investors may be wondering about prospective default rates—and their potential impact on credit spreads.

By Riz Hussain Product Messaging Lead

By Riz Hussain Product Messaging LeadHow the Distress Ratio Guides Default Expectations

-

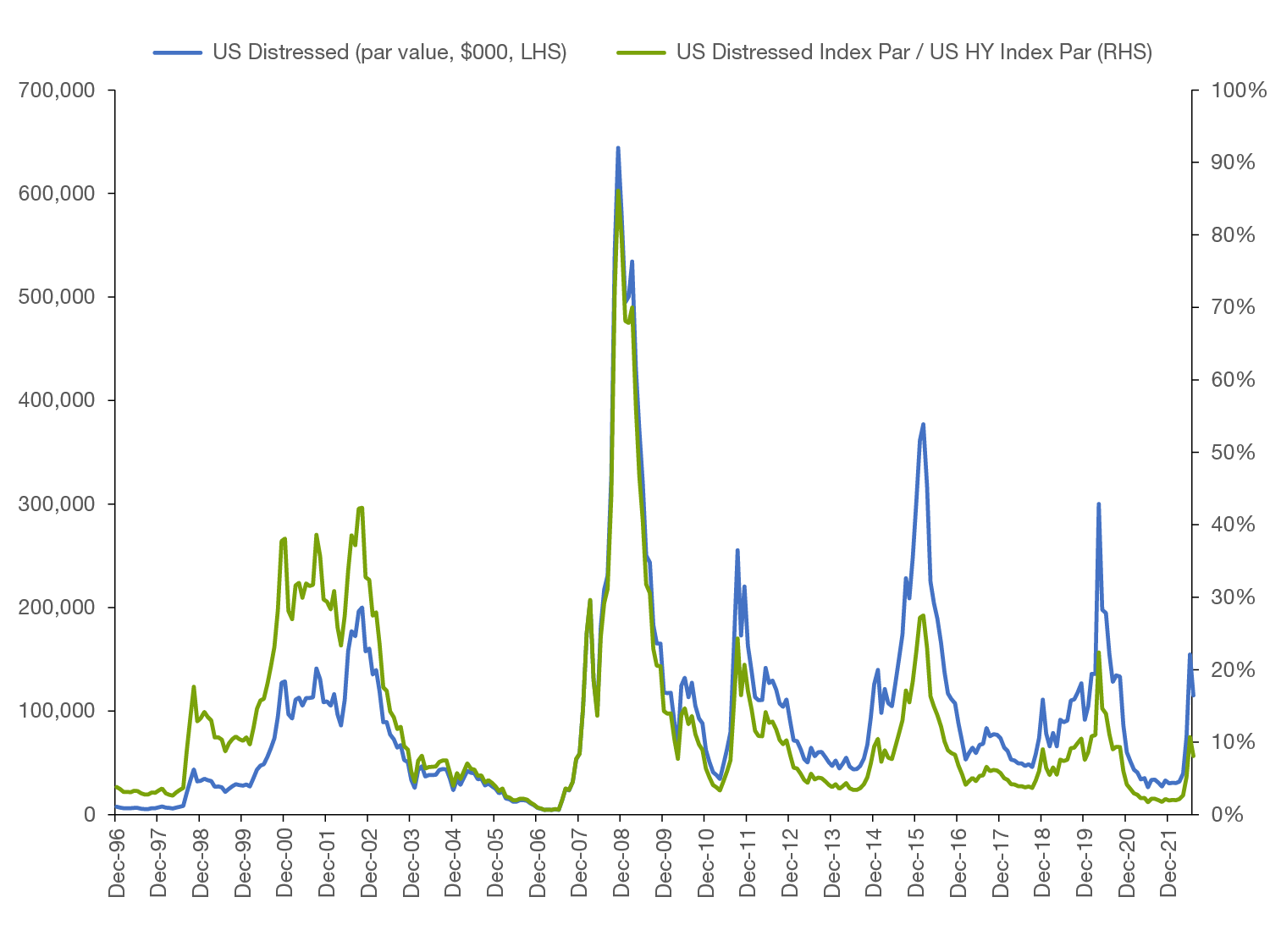

As of July month-end, the U.S. high yield distress ratio was 8.1%, rising from just below 2% at the start of the year (see Figure 1). However, this measure improved over the course of the month by 2.6 percentage points, as you would expect, given the overall rally in high yield credit spreads during July.

-

In our prior referenced work above, we found that the median ratio of the actual 12-month-forward default rate to the starting distress ratio was about 36%. We can’t definitively state all defaults over a coming year come from those credits identified as under distress during that period, but academic work published elsewhere notes that the vast majority of defaulting names are indeed trading at distressed valuations within the year prior.

-

So, if we just use that experience as a guide, and if the distress ratio did not change from the levels on July 29, it suggests an estimated 12-month-forward default rate of about 2.9% (=36%*8.1%). Right now, that’s about the mid- to upper-end of the range of what most sell-side analysts have been calling for in high yield. Recall that the U.S. high yield, trailing-12-month default rate hit a COVID-19-era peak of about 6% in late 2020.

-

Using 40% as the approximate long-term, average observed recovery rate on defaulted high yield bonds, and the current market starting price of approximately $90, imply an expected loss-given default of 1.45%, favorable relative to current spread levels

Figure 1. Tracking the U.S. High Yield Distress Ratio

The “Excess Spread” Available in U.S. High Yield

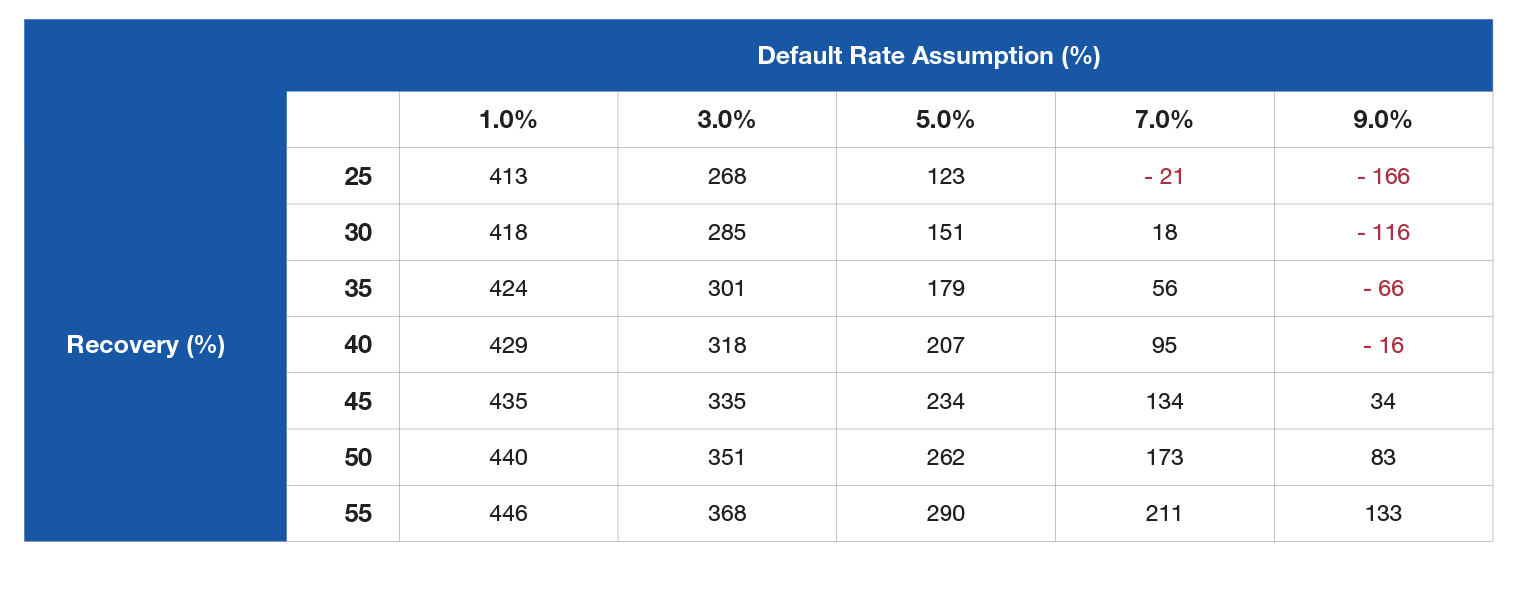

Given a range of potential default-loss outcomes, how are investors being compensated? Positive values that fall out for an assessment of this “excess spread” would reflect our long-standing view that credit spreads overpay investors for defaults. That outcome would also emphasize that investors embrace a strategic mindset (over a “market timing” approach) and collect this excess spread that remains after absorbing default losses. These positive values for excess spread are essentially risk premium that patient investors can capture, after adjusting current spread for future default losses. And it varies given investors’ collective risk sentiment, tolerance, holding periods, market structure liquidity, etc. However, we can argue that at any point in time, the then-current credit spread of the broad investment-grade-credit corporate market could serve as a lower bound for the excess spread in high yield, given investment-grade credit is largely a default-risk-remote asset class with similar types of non-default risk as high yield.

In Figure 2, we show the excess spread based on a range of assumptions for the recovery rate and default rate, at the current Index option-adjusted spread (OAS) and price (+485 bps and $90.28, respectively). Note that except for a combination of particularly low recovery levels and/or high default rates that largely exceeded that of the COVID-19 pandemic, investors are collecting a positive risk premium that exceeds the OAS of the investment-grade market at today’s valuations. Focusing just on a default assumption of approximately 3% (in line with the estimate derived from the distress ratio) and a 40% recovery leads to an excess spread of 318 bps today, for example.

Figure 2. Excess Spread on High Yield Based on Assumed Recovery and Default Rates

For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Past performance is not a reliable indicator or guarantee of future results.

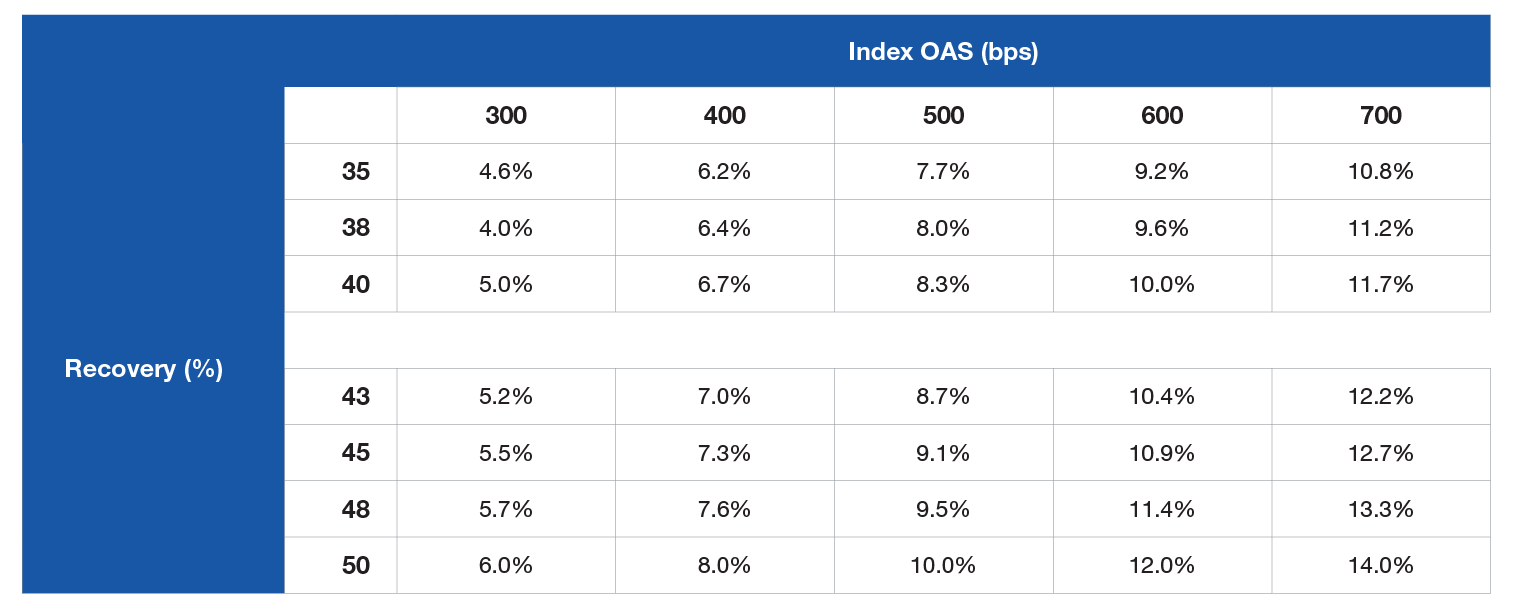

Figure 3. Investors Appear to Be Overly Pessimistic about Potential Default Rates

For illustrative purposes only and does not represent any specific portfolio managed by Lord Abbett or any particular investment. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Past performance is not a reliable indicator or guarantee of future results.

Key Takeaways

Under the Hood of “Excess Spread”

We discuss excess spread, the amount that high yield investors can capture in excess of projected default loss, extensively in this article. But how is it derived? First, let’s start with two equations that are important in credit math:

Spread Compensation for Expected Defaults = (Index Option-Adjusted Spread [OAS] – Excess Spread)

Expected Loss Given Default = Default Rate * [(Index Price – Recovery)/Index Price]

And we know by definition:

Spread Compensation for Expected Defaults = Expected Loss Given Default

Thus:

(Index OAS – Excess Spread) = Default Rate * [(Index Price – Recovery)/Index Price], or

(Index OAS – Excess Spread) = Default Rate * (1 – Recovery/Index Price)

Determining all these factors leads us to our excess spread calculation:

Excess Spread = Index OAS – (Default Rate * (1 – Recovery/Index Price))

As informações aqui contidas estão sendo fornecidas pela GAMA Investimentos (“Distribuidor”), na qualidade de distribuidora do site. O conteúdo deste documento [e informações neste site] contém informações proprietárias sobre LORD ABBETT e o Fundo. Nenhuma parte deste documento nem as informações proprietárias do LORD ABBETT ou DO Fundo aqui podem ser (i) copiadas, fotocopiadas ou duplicadas de qualquer forma por qualquer meio (ii) distribuídas sem o consentimento prévio por escrito do LORD ABBETT. Divulgações importantes estão incluídas ao longo deste documento e que devem ser utilizadas exclusivamente para fins de análise do LORD ABBETT e do Fundo. Este documento não pretende ser totalmente compreendido ou conter todas as informações que o destinatário possa desejar ao analisar o LORD ABBETT e o Fundo e/ou seus respectivos produtos gerenciados ou futuramente gerenciados. Este material não pode ser utilizado como base para qualquer decisão de investimento. O destinatário deve confiar exclusivamente nos documentos constitutivos de qualquer produto e em sua própria análise independente. Nem o LORD ABBETT nem o Fundo estão registrados ou licenciados no Brasil e o Fundo não está disponível para venda pública no Brasil. Embora a Gama e suas afiliadas acreditem que todas as informações aqui contidas sejam precisas, nenhuma delas faz qualquer declaração ou garantia quanto à conclusão ou necessidades dessas informações.

Essas informações podem conter declarações de previsões que envolvem riscos e incertezas; os resultados reais podem diferir materialmente de quaisquer expectativas, projeções ou previsões feitas ou inferidas em tais declarações de previsões. Portanto, os destinatários são advertidos a não depositar confiança indevida nessas declarações de previsões. As projeções e/ou valores futuros de investimentos não realizados dependerão, entre outros fatores, dos resultados operacionais futuros, do valor dos ativos e das condições de mercado no momento da alienação, restrições legais e contratuais à transferência que possam limitar a liquidez, quaisquer custos de transação e prazos e forma de venda, que podem diferir das premissas e circunstâncias em que se baseiam as perspectivas atuais, e muitas das quais são difíceis de prever. O desempenho passado não é indicativo de resultados futuros.