Link para o artigo original: https://www.bridgewater.com/research-and-insights/are-we-still-on-the-path-to-equilibrium

The most recent Fed meeting confirmed that policy makers see the strength of conditions warranting a pause in the easing cycle. Looking forward, we expect economic outcomes to remain on the upper end of policy makers’ goals.

As we have discussed previously, we see the current economic environment reflecting the gradual drift of economic conditions toward equilibrium and market pricing reflecting expectations of stable economic outcomes and neutral monetary policy. From here, the question for markets is whether this process has room to run, or whether the underlying moderation in conditions stalls out with the economy remaining too hot for policy makers to support assets.

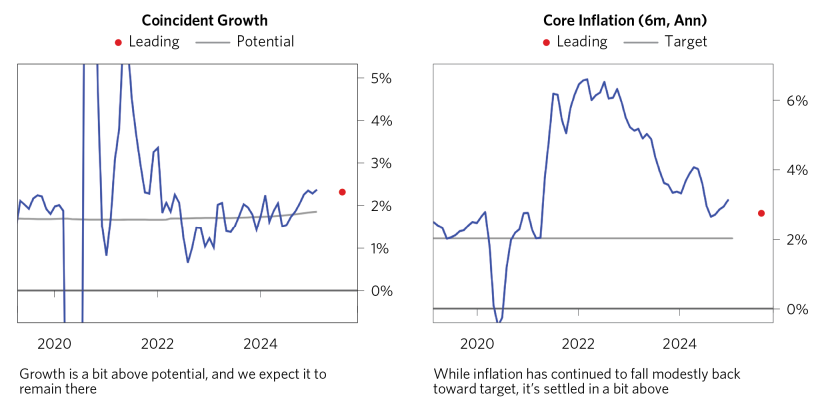

Recently, we’ve seen signs that the path will be bumpier than expected: inflation has remained above target; labor markets have remained tight; and policy makers have signaled that they in turn will be more cautious about easing policy, with the Fed on Wednesday holding rates steady. Markets have responded to these developments by increasing inflation expectations, paring back the pricing of rate cuts, and driving up forward yields relative to cash. Some degree of this is healthy; it reflects asset pricing and risk premia adjusting more in line with the current and likely forward path of conditions and policy. But these developments also reverberate back into the economy: the broad-based increase in interest rates is likely to tamp down what little credit impulse was coming from the modest easing we’ve gotten so far and to weigh more broadly as a countervailing downward pressure on growth and inflation.

Looking forward, we expect this push and pull to continue: the economy is still a bit too hot relative to policy maker goals, so a significant easing isn’t currently justified, but baseline conditions are likely to remain near the cyclical sweet spot of on-target growth and inflation. Typically, this is a solid environment for holding assets and earning a roughly normal risk premia, and we expect this dynamic to remain a support. Today, however, favorable conditions are already largely reflected in market pricing, and risk premia—particularly in the US—are narrow. On the other hand, asset yields likely can’t rise much more without exerting economic pain that policy makers are unlikely to tolerate, given only modest constraints on their capacity to ease.

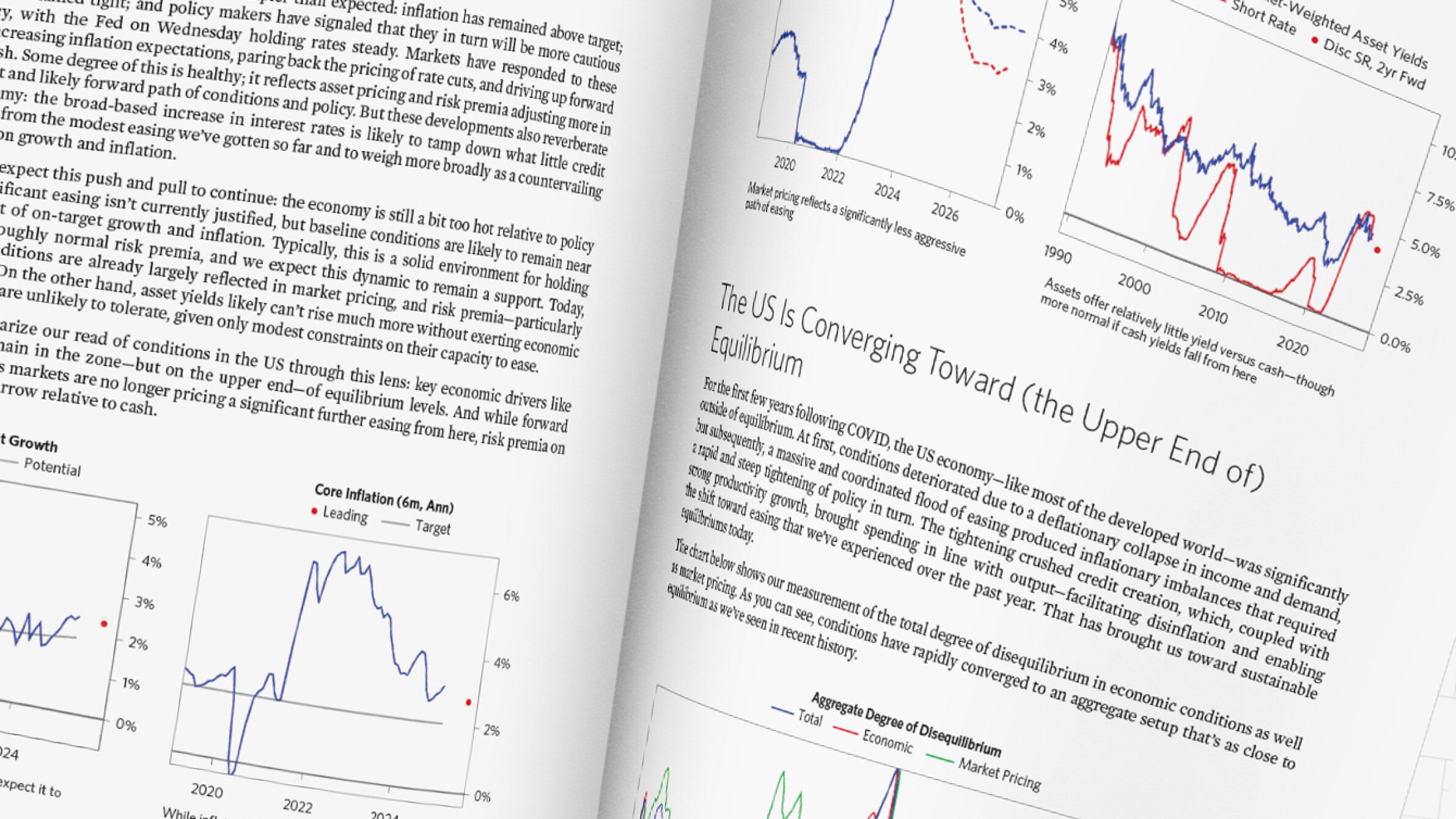

The charts below summarize our read of conditions in the US through this lens: key economic drivers like growth and inflation remain in the zone—but on the upper end—of equilibrium levels. And while forward interest rates have risen as markets are no longer pricing a significant further easing from here, risk premia on assets broadly still look narrow relative to cash.

The US Is Converging Toward (the Upper End of) Equilibrium

For the first few years following COVID, the US economy—like most of the developed world—was significantly outside of equilibrium. At first, conditions deteriorated due to a deflationary collapse in income and demand, but subsequently, a massive and coordinated flood of easing produced inflationary imbalances that required a rapid and steep tightening of policy in turn. The tightening crushed credit creation, which, coupled with strong productivity growth, brought spending in line with output—facilitating disinflation and enabling the shift toward easing that we’ve experienced over the past year. That has brought us toward sustainable equilibriums today.

The chart below shows our measurement of the total degree of disequilibrium in economic conditions as well as market pricing. As you can see, conditions have rapidly converged to an aggregate setup that’s as close to equilibrium as we’ve seen in recent history.

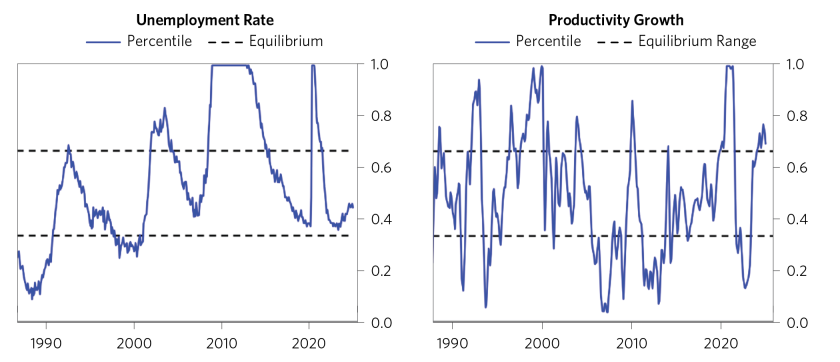

Next, we show a few of the key measures we look at to track the path to equilibrium. We show each of the measures relative to our estimate of equilibrium levels, in percentile terms versus their historical distributions, to make the relative magnitudes more comparable across concepts.

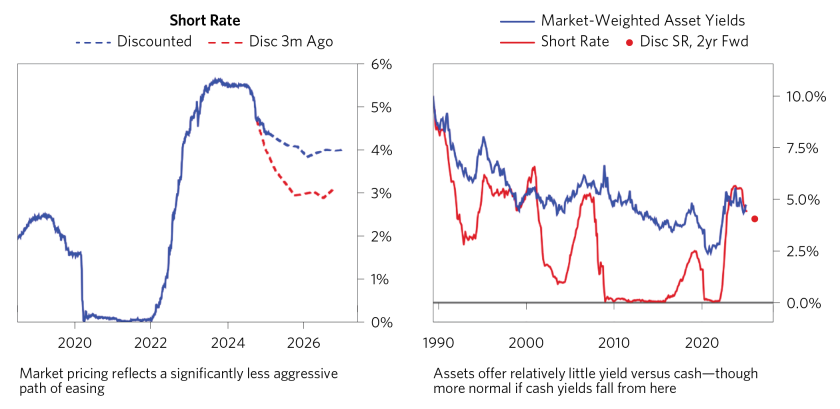

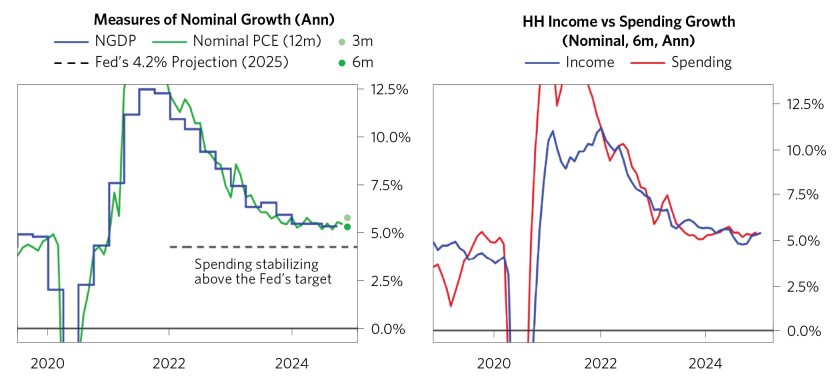

Putting together the real growth and inflation pictures, nominal spending remains strong and on the upper edge of what is likely tolerable. This spending is supported by ongoing robust income growth, which in turn is reinforced by wages and a healthy labor market. Meanwhile, the inflationary ramifications of low unemployment and high wages have been softened by the disinflationary effects of high productivity growth. Our leading measures suggest that conditions are likely to settle in at levels similar to today, without significant change pressures.

Backward-Looking Easing Has Supported Ongoing Strength, While the Recent Market-Based Tightening Is a Drag—Netting to a Balanced Forward-Looking Picture

In the US, our timely estimates suggest that nominal spending is stabilizing above the Fed’s target—with a modest acceleration in the timeliest measures (e.g., three-month spending growth) after the Fed’s pivot to easing this past fall. Further, spending is rising in line with (and feeding back into) incomes, which supports a self-sustaining flywheel at today’s levels.

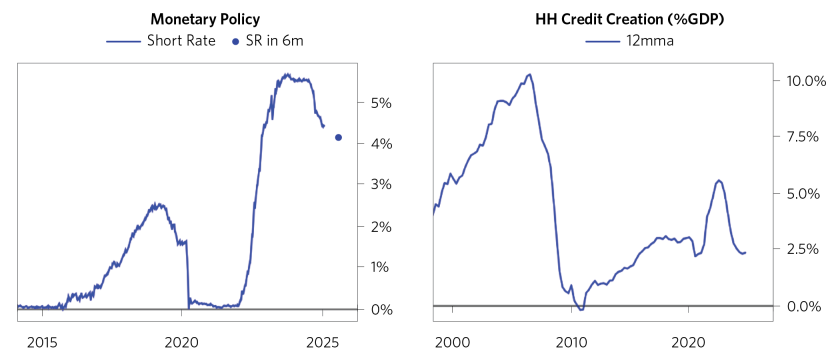

Strong incomes have continued to fuel spending without much credit creation. If the easing cycle continues, there is plenty of room for credit to bounce from today’s extremely low levels, particularly for households with strong balance sheets and low current levels of borrowing.

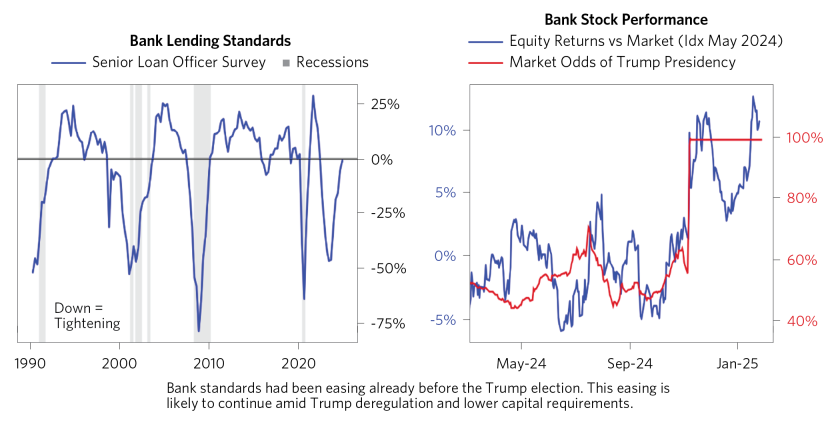

Additionally, there are signs of credit conditions easing even absent further interest rate cuts, with lending standards beginning to ease and optimism in the financial sector increasing, particularly in light of Trump’s election win.

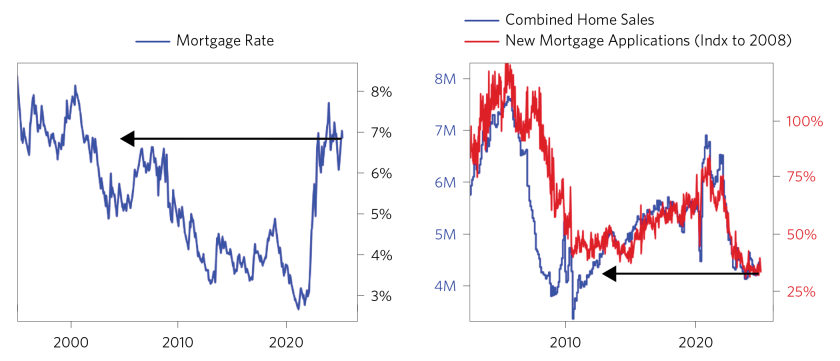

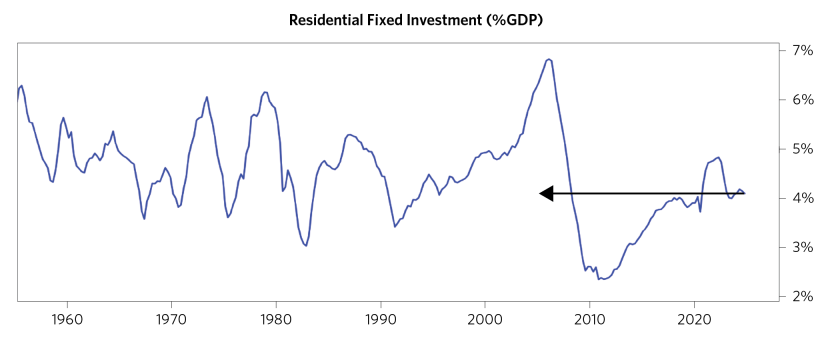

On the other hand, the recent leg up in interest rates is likely to continue to restrict borrowing. Mortgage rates are at nearly 20-year highs, and housing market activity is at its lowest point since the financial crisis.

But, because the level of credit-sensitive spending, e.g., residential fixed investment, remains a small share of the overall economy relative to history, the direct effects on growth will be small.

These Pressures Are Playing Out in the Context of Still-Tight Underlying Conditions

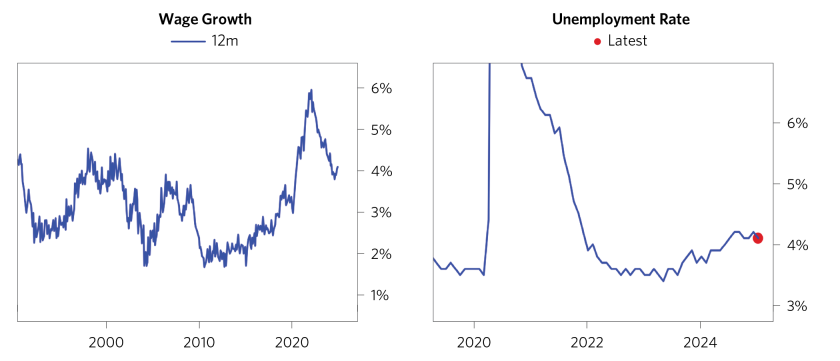

Capacity in the economy, particularly in the labor market, remains somewhat tight, with wage growth still at relatively high levels and unemployment still fairly low.

The deceleration of wages over the last few years was enabled by labor supply growth, particularly from immigration. But that is now rolling off and, with the election of President Trump, likely reversing. In turn, the level of unemployment has stopped rising as the labor force expansion has slowed and wage growth has stopped falling, with timely reads indicating a 4% or so run rate pace.

Stable Conditions and Ample Liquidity Are Almost Always Supportive of Assets But Are Rarely Priced In to This Extent

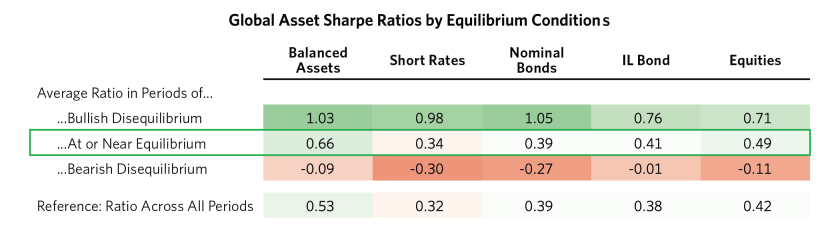

Environments like today’s, with stable conditions and policy, are generally good times for assets (for example, conditions were in a similar sweet spot for most of the 2010s), and we expect those dynamics to continue to support assets today. The table below shows global asset returns split into periods of bullish disequilibrium (high risk premia, weak conditions, easy policy), bearish disequilibrium (the opposite), and near-equilibrium periods like today. As you can see, asset returns are substantially influenced by conditions relative to equilibrium due to the confluence of what policy that environment calls for and the pricing of assets leading into the policy. Equilibrium conditions don’t call for much policy shift, are generally associated with a near-normal level of risk premia, and, as a result, have produced near-average excess returns.

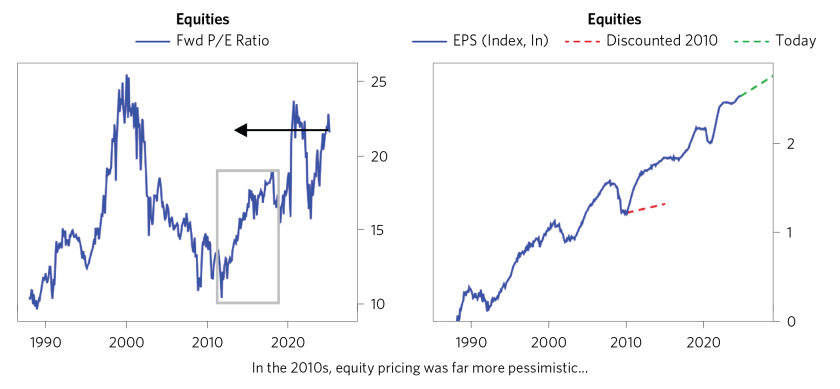

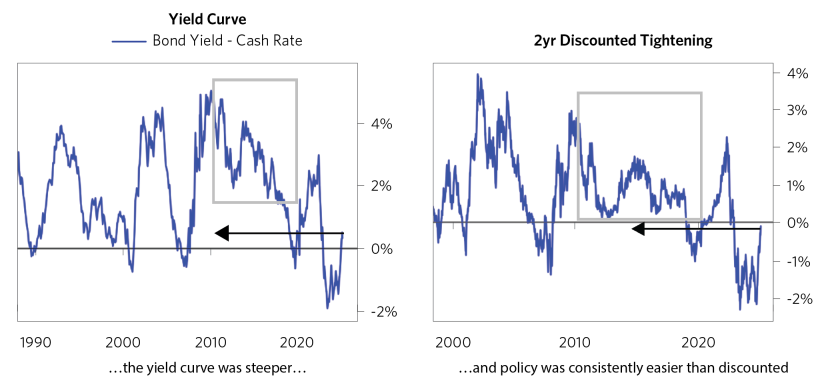

However, a favorable economic environment and policy stance today is already reflected in market pricing, and risk premia on assets have narrowed significantly relative to cash—substantially raising the hurdle needed for assets to continue to outperform. Compare, for example, current conditions to the 2010s. While the economic environment was similar—with around-target growth and inflation, and modest levels of capacity—market dynamics were much more favorable for assets: valuations were much weaker, risk curves were steeper, and policy was consistently easy relative to expectations.

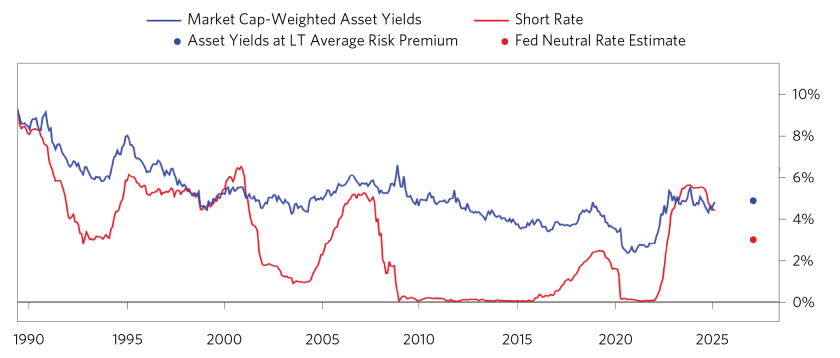

The most favorable path to restore normal risk premia in assets is to push short-term interest rates below asset yields. The chart below shows the current yield of assets in the US relative to cash, weighted by market cap. We then show the Fed’s estimate of the long-term neutral policy rate, i.e., the rate policy makers will manage toward if conditions allow. As you can see, if we get the normalization toward neutral rates that the Fed is projecting, then asset yields where they currently are will in aggregate offer a near-normal risk premium relative to that forward cash rate. But if we stabilize at a higher level of demand with tight capacity and disinflationary forces reverting, it’s unlikely policy will be able to ease as much as is discounted. In that world, asset yields likely have to rise—and prices fall—in order to create appropriate risk premia relative to cash. In our view, the market action over the past few months in part reflects this dynamic, as forward yields have risen in concert with expectations that a significant easing will be more difficult for policy makers to achieve.

This report is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or tolerances of any of the recipients. Additionally, Bridgewater’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This material is for informational and educational purposes only and is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned. Any such offering will be made pursuant to a definitive offering memorandum. This material does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual investors which are necessary considerations before making any investment decision. Investors should consider whether any advice or recommendation in this research is suitable for their particular circumstances and, where appropriate, seek professional advice, including legal, tax, accounting, investment, or other advice. No discussion with respect to specific companies should be considered a recommendation to purchase or sell any particular investment. The companies discussed should not be taken to represent holdings in any Bridgewater strategy. It should not be assumed that any of the companies discussed were or will be profitable, or that recommendations made in the future will be profitable.

The information provided herein is not intended to provide a sufficient basis on which to make an investment decision and investment decisions should not be based on simulated, hypothetical, or illustrative information that have inherent limitations. Unlike an actual performance record simulated or hypothetical results do not represent actual trading or the actual costs of management and may have under or overcompensated for the impact of certain market risk factors. Bridgewater makes no representation that any account will or is likely to achieve returns similar to those shown. The price and value of the investments referred to in this research and the income therefrom may fluctuate. Every investment involves risk and in volatile or uncertain market conditions, significant variations in the value or return on that investment may occur. Investments in hedge funds are complex, speculative and carry a high degree of risk, including the risk of a complete loss of an investor’s entire investment. Past performance is not a guide to future performance, future returns are not guaranteed, and a complete loss of original capital may occur. Certain transactions, including those involving leverage, futures, options, and other derivatives, give rise to substantial risk and are not suitable for all investors. Fluctuations in exchange rates could have material adverse effects on the value or price of, or income derived from, certain investments.

Bridgewater research utilizes data and information from public, private, and internal sources, including data from actual Bridgewater trades. Sources include BCA, Bloomberg Finance L.P., Bond Radar, Candeal, CBRE, Inc., CEIC Data Company Ltd., China Bull Research, Clarus Financial Technology, CLS Processing Solutions, Conference Board of Canada, Consensus Economics Inc., DataYes Inc, DTCC Data Repository, Ecoanalitica, Empirical Research Partners, Entis (Axioma Qontigo Simcorp), EPFR Global, Eurasia Group, Evercore ISI, FactSet Research Systems, Fastmarkets Global Limited, The Financial Times Limited, FINRA, GaveKal Research Ltd., Global Financial Data, GlobalSource Partners, Harvard Business Review, Haver Analytics, Inc., Institutional Shareholder Services (ISS), The Investment Funds Institute of Canada, ICE Derived Data (UK), Investment Company Institute, International Institute of Finance, JP Morgan, JSTA Advisors, LSEG Data and Analytics, MarketAxess, Medley Global Advisors (Energy Aspects Corp), Metals Focus Ltd, MSCI, Inc., National Bureau of Economic Research, Neudata, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Pitchbook, Rhodium Group, RP Data, Rubinson Research, Rystad Energy, S&P Global Market Intelligence, Scientific Infra/EDHEC, Sentix GmbH, Shanghai Metals Market, Shanghai Wind Information, Smart Insider Ltd., Sustainalytics, Swaps Monitor, Tradeweb, United Nations, US Department of Commerce, Verisk Maplecroft, Visible Alpha, Wells Bay, Wind Financial Information LLC, With Intelligence, Wood Mackenzie Limited, World Bureau of Metal Statistics, World Economic Forum, and YieldBook. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

This information is not directed at or intended for distribution to or use by any person or entity located in any jurisdiction where such distribution, publication, availability, or use would be contrary to applicable law or regulation, or which would subject Bridgewater to any registration or licensing requirements within such jurisdiction. No part of this material may be (i) copied, photocopied, or duplicated in any form by any means or (ii) redistributed without the prior written consent of Bridgewater® Associates, LP.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.