Link para o artigo original: https://www.oaktreecapital.com/insights/insight-commentary/market-commentary/the-roundup-top-takeaways-from-oaktree-s-quarterly-letters-december-2024-edition

Amid a strong U.S. economy and potentially inflationary policies from the incoming administration, yields may remain higher for longer. High-income assets will likely benefit, but investors should avoid complacency, particularly given the unpredictability of macroeconomic factors. In the current installment of The Roundup,1 Oaktree experts examine the risks and opportunities in various asset classes, from financing solutions for life sciences companies and signs of stabilizing real estate valuations to the implications of China’s stimulus measures and the recent surge in convertible bond issuance.

1

Global Credit:

Carry On

Expectations for further cuts to the federal funds rate have moderated amid a remarkably robust U.S. economy and the prospect of inflationary policies from the incoming Republican administration. With credit spreads already on the tight end of the historical range, duration failing to be a reliable return-driver given the volatile interest rate environment, and Treasury yields remaining elevated, there has only been one sure game in credit: income. Assets offering high coupons – notably floating-rate instruments, such as senior loans and CLOs – have especially profited from this backdrop.

So, what’s led to a more hawkish Fed, and may keep Treasury yields higher for longer?

(1) The exceptional resilience of the U.S. economy:

- U.S. GDP increased at a robust annual rate of 2.8% in the third quarter.2

- Consumer sentiment hit a seven-month high in early November.3

- Jobs data has been stronger than expected, with more than 225,000 jobs added in November.4

(2) The incoming Republican administration’s potentially inflationary campaign promises:

- Imposing steep tariffs could increase the cost of imported consumer goods.

- Reducing taxes would add to the national deficit.

- Restricting immigration could trigger higher wage growth and make job openings harder to fill.

However, these factors may not run a linear course. In a recent interview, Howard Marks reminded us that “probably 98% of the things Trump will do can’t be predicted, and even the consequences of the things we know he’ll do probably can’t be predicted.” The U.S. economy seems to be on solid footing, but data surprises could lead to volatility, and policies introduced by the Trump administration may have unpredictable second-order impacts.

Though it’s difficult to predict macroeconomic factors, investors may benefit from focusing on yield and maximizing income to drive portfolio returns. Certainly, assets generally offer more income when they present more credit risk. Selecting for high income therefore isn’t a panacea; it must be matched with diligent underwriting and robust downside protection.

2

Life Sciences:

Secular Growth

Surging healthcare expenditure shows no sign of abating. Aging populations across developed markets and an expanding global middle class are driving increasing healthcare needs across almost every major economy. Meeting this demand requires companies in the life sciences industry to constantly evolve and refine crucial biopharmaceutical products and associated devices.

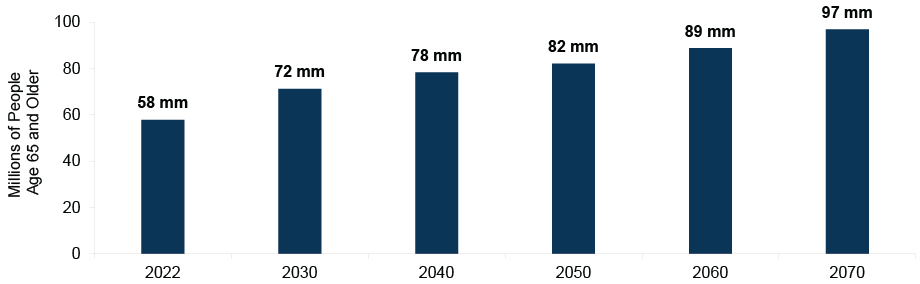

The U.S. population is aging rapidly. Between 2022 and 2050, the number of people above the age of 65 is projected to increase by nearly 25 million.5 (See Figure 1.) The cohort above 85 years of age is projected to grow at an even faster rate, tripling by 2050.6 The relevance of this is the disproportionate healthcare spend associated with senior citizens. Of Americans living with two or more chronic conditions, over 64% are aged 65 and above, with the per-person healthcare spend for this demographic roughly 2.5 times that of working-age people.7

Meeting this demand will be a highly capital-intensive endeavor, requiring significant spending on research and development, building manufacturing and supply chain capacities, and the commercializing of existing and new products. Accordingly, global annual R&D spending on drugs is expected to reach $290 billion by 2026.8 Given these demographic changes, increased governmental health care spending, and heightened demand for advanced treatments from the middle class, we expect there to be a rise in demand for financing provided to the life sciences companies engaged in addressing these factors.

Smaller and mid-sized life sciences companies have historically sought funding primarily from the equity and equity-linked markets, but over the past decade, companies have increasingly pursued non-dilutive financing solutions. Debt – besides being a less expensive source of funding compared to equity – can provide businesses with more capital certainty and allow companies to be less reliant on potentially volatile capital markets. However, traditional debt financing may be unavailable for even more mature life sciences companies: we’re increasingly seeing these companies seek financing from specialist direct lenders, who can understand their esoteric product offerings.

Figure 1: The Number of Senior Citizens in the U.S. Is Expected to Dramatically Increase

Source: U.S. Census Bureau, as of November 2023; represents the latest available national population projection

3

Real Estate Income:

Inflection Point

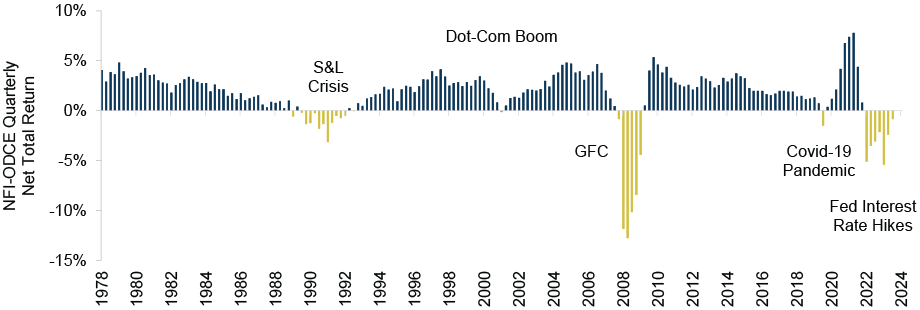

We may be reaching an inflection point for core/core-plus real estate following a significant reset in property values over the past two and a half years. (See Figure 2.) Declines in valuations over this period were largely the result of higher interest rates, rather than a significant deterioration of fundamentals.

In fact, valuations of core/core-plus properties have shown signs of stabilization in recent quarters, supported by (a) improving fundamentals, (b) declining interest rates, (c) increased debt liquidity, (d) a rebound in publicly traded REIT prices, and (e) rising demand from previously inactive real estate buyers. An exception to this is the office sector, which continues to face significant headwinds, with limited investor interest contributing to ongoing value declines.

The multifamily property sector may benefit from favorable supply/demand dynamics, including:

- Declining supply, with new supply of multifamily units expected to fall by 48% from 2024 to 2025, a trend that may persist through 2027.9

- Limited for-sale housing availability and increased replacement costs mean monthly ownership costs exceed equivalent rental costs by a historically high margin.

- Strong rental demand, with 467,000 in net-new multifamily units leased in 2024, the highest annual amount since 2000 (excluding the post-pandemic boom years of 2021 and 2022).10

Lastly, while economic uncertainty may result in near-term volatility in interest rates, core/core-plus real estate is positioned to benefit from the downward trajectory of interest rates, which would lower the cost of capital and support greater transaction activity. This shift in interest rate policy by the Fed has already led to a pick-up in private CMBS debt issuance, which is up by 154% year-over-year.11

Figure 2: The Reset in Real Estate Valuations Shows Signs of Easing

Source: NFI-ODCE Index (a proxy for core real estate performance), as of September 30, 2024

4

Emerging Markets Debt:

Turning the Tide

In late September, China’s government announced a broad stimulus package seeking to reverse the country’s recent economic downturn. The proposed policies sparked a rally in Chinese equities, which then moderated as market participants awaited further quantitative detail around the measures.

China currently faces multiple challenges. Consumer confidence is near record lows, as evidenced by the massive $20 trillion stockpile in deposits.12 Property transactions and prices have fallen sharply this year, further dampening consumer sentiment.13 China also faces sustained deflationary pressure due to weak domestic demand: the country’s economy recorded its lowest year-over-year expansion in 18 months, at 4.6%, in 3Q2024.14

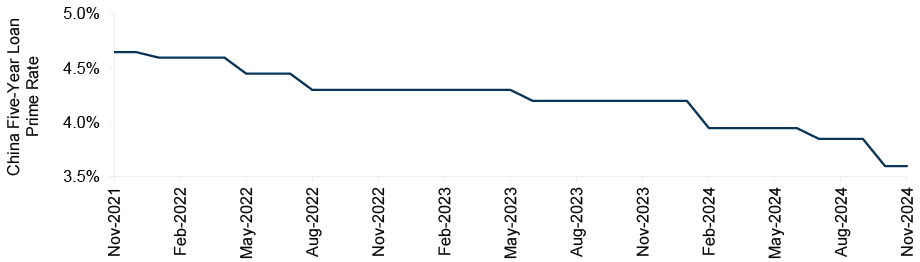

However, the recent stimulus may mark a turning point. The country’s top leadership has displayed a new urgency, and the scale of monetary easing is the largest seen in decades. (See Figure 3.) The policymakers’ stabilization objectives include:

- stimulating the stock market,

- boosting credit creation,

- reinforcing bank capital ratios and solvency,

- providing financial aid to students and the elderly, and

- bolstering housing demand (the economy’s largest “pain point”) through lower mortgage rates, tax subsidies, and reduced housing restrictions in major cities.

The critical question for market participants is whether these policies will be sufficient to reignite economic growth and investor confidence. Calibrating the world’s second-largest economy for sustainable but not excessive growth is a delicate balancing act. If the current policies fall short, particularly in the event of a trade conflict with the U.S., China remains in a position to expand its efforts, supported by the country’s world-leading foreign reserves and financial asset base, and unparalleled growth over the last half century.15

We can’t predict when investor sentiment in China will improve, given the complexities involved in reflating a large economy and the uncertainty surrounding current geopolitical tensions. For now, many Chinese assets continue to be considered “uninvestable,” creating the opportunity for value-oriented investors to identify bargains.

Figure 3: Lending Rates in China Have Been Cut Significantly

Source: Bloomberg

5

Global Convertibles:

Resurgence

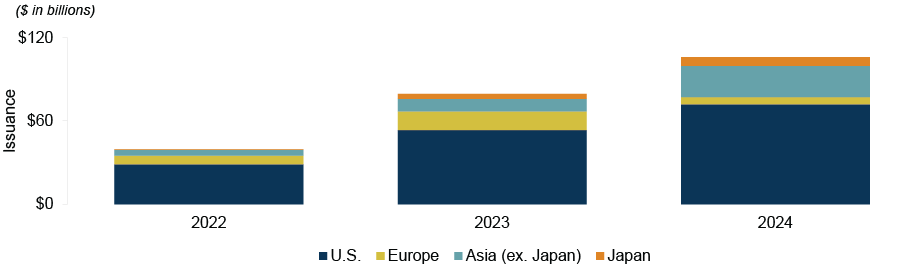

Convertible bond issuance has continued to surge since the trough in 2022, increasing both the size and quality of the convertible bond market. Thus far in 2024, new issuance of global convertible bonds is running at the fastest pace seen since 2021. Primary issuance has been strongest in the U.S., with over $60 billion in volume so far this year, but it also remains robust outside the U.S., with over $32 billion of new issuance over the same period.16 (See Figure 4.)

In an elevated interest rate environment, companies seeking new capital, or those looking to refinance straight debt, have increasingly turned to the convertibles market, where coupons are lower. Though coupons are modest compared to the elevated levels seen on senior loans and high yield bonds, they remain attractive in historical terms: the average coupon for a new global convertible bond is 3.4%, compared to the low of 1.0% in 2021.17

The majority of convertible bond issuance in 2024 has been in the technology sector. Alongside meaningful issuance from technology companies in the U.S., we’ve seen Chinese technology companies tap the convertibles market at scale. Beyond the benefit of lower interest expenses, Chinese technology companies may be inclined to issue convertible bonds because they:

- need dollars to fund international expansion but collect renminbi from domestic sales;

- seek efficient ways to fund share buybacks;

- may struggle to access traditional equity markets (e.g., through IPOs in the U.S.); and,

- may have a relatively volatile share price, making the equity option embedded in the convertible bond more attractive for investors.

Strong equity market performance has also put convertible bonds back in the spotlight. The U.S. equity rally – previously concentrated among a handful of large technology companies – broadened in the third quarter to include a wider subset of companies. This may serve as a favorable tailwind for convertible bonds as more sectors begin to share in the profits. Global ex-U.S. equities may also have upside potential in the form of moderate valuations: the MSCI EAFE Index (a reasonable proxy for the ex-U.S. equity market) currently has a price-to-earnings ratio around half that of the S&P 500.18

Figure 4: Convertible Bond Issuance Has Recovered

Source: Bank of America Global Research, as of October 31, 2024

Endnotes

- 1The content is derived from or inspired by ideas in 3Q2024 letters or other materials sent to clients in 4Q2024; the text has been edited for space, updated, and expanded upon where appropriate.

- 2Bureau of Economic Analysis.

- 3University of Michigan Survey.

- 4U.S. Bureau of Labor Statistics.

- 5U.S. Census Bureau.

- 6Jones, C.H., Dolsten, M. Healthcare on the brink: navigating the challenges of an aging society in the United States. April 6, 2024.

- 7Ibid; Center for Medicare & Medicaid Services, as of September 2024.

- 8EvaluatePharma.

- 9CoStar, as of September 30, 2024.

- 10Ibid.

- 11JP Morgan, as of September 30, 2024.

- 12The People’s Bank of China, as of October 2024.

- 13S&P Global Ratings, as of October 2024.

- 14National Bureau of Statistics of China, as of October 2024.

- 15International Monetary Fund, as of August 2023.

- 16BofA Global Research, as of October 31, 2024.

- 17BofA Global Research, as of September 30, 2024.

- 18The MSCI EAFE Index represents large- and mid-cap securities across Europe, Australasia, and the Far East.

Notes and Disclaimers

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2024 Oaktree Capital Management, L.P.

Informações sensíveis e divulgação

Este memorando expressa as opiniões do autor na data indicada e tais opiniões estão sujeitas a alterações sem aviso prévio. A Oaktree não tem a obrigação de atualizar as informações aqui contidas. Além disso, a Oaktree não faz nenhuma representação, e não se deve assumir que o desempenho dos investimentos passados é uma indicação de resultados futuros. Além disso, onde quer que haja potencial de lucro, também existe a possibilidade de prejuízo. Este memorando está sendo disponibilizado apenas para fins educacionais e não deve ser usado para qualquer outro propósito. As informações contidas neste documento não constituem e não devem ser interpretadas como uma oferta de serviços de consultoria ou uma oferta de venda ou solicitação de compra de quaisquer títulos ou instrumentos financeiros relacionados, em qualquer jurisdição. Certas informações contidas neste documento sobre tendências econômicas e desempenho são baseadas ou derivadas de informações fornecidas por fontes terceirizadas independentes. A Oaktree Capital Management, L.P. (“Oaktree”) acredita que as fontes das quais tais informações foram obtidas são confiáveis; no entanto, não pode garantir a exatidão de tais informações e não verificou de forma independente a exatidão ou integridade de tais informações ou as suposições nas quais tais informações se baseiam. Este memorando, incluindo as informações aqui contidas, não pode ser copiado, reproduzido, republicado ou postado na íntegra ou parcialmente, em qualquer formato, sem o consentimento prévio, por escrito, da Oaktree.