The Countervailing Forces on Bond Yields and the Timing of a Rise

Bond markets have been a poor predictor of changes in Fed policy.

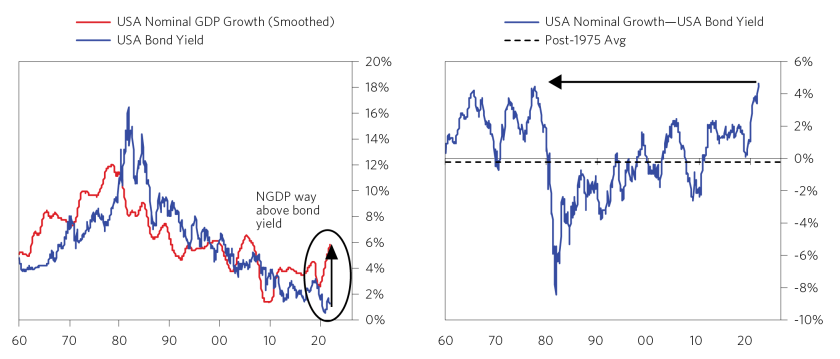

Recent bond market action has the look of an irresistible force confronting an immovable object. The irresistible force is the rapid acceleration in inflation and nominal growth combined with a precarious supply/demand balance for bonds, and the level of nominal and real interest rates offering little incentive to take down the supply. The immovable object is the Fed and other central banks’ desire to suppress a rise in interest rates that would otherwise offset the fiscal stimulation that is being applied. Their weapons are zero short-term interest rates, forward guidance pertaining to that, direct purchases of bonds, and a layer of private sector liquidity from aggressive MP3 actions.

How long might this standoff last? The best answer is that it will last until conditions become incompatible with the Fed’s economic goals (e.g., inflation or the currency getting out of control). Playing that out, given that the suppression of interest rates—intended to prevent a hot economy from pushing up yields—actually heightens those very pressures, the logical implication is that the Fed and other central banks will increasingly be pushed to change course and tighten policy. As for timing, uncertainty is increased by recurring waves of the virus, though the more virus waves occur, the less economic impact they are having. As we see it, it is a matter of time before policy preferences shift and the immovable object gives way to the irresistible force. And until then, the spread between cash flow yields and interest rates will remain very wide.

Historically, Bond Yields Haven’t Led Central Bank Tightening by Much

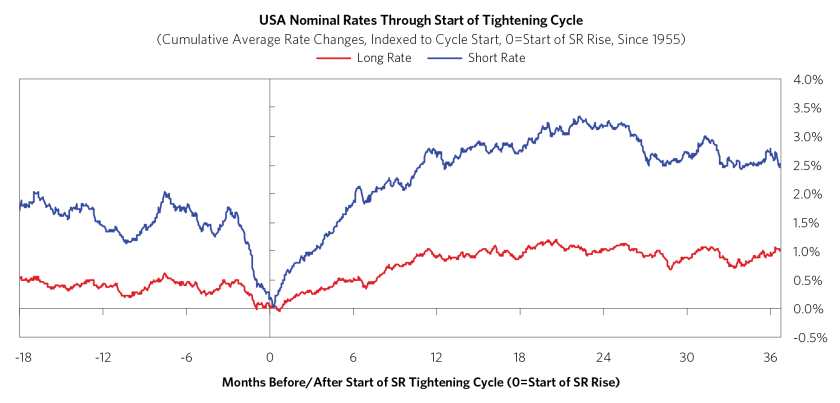

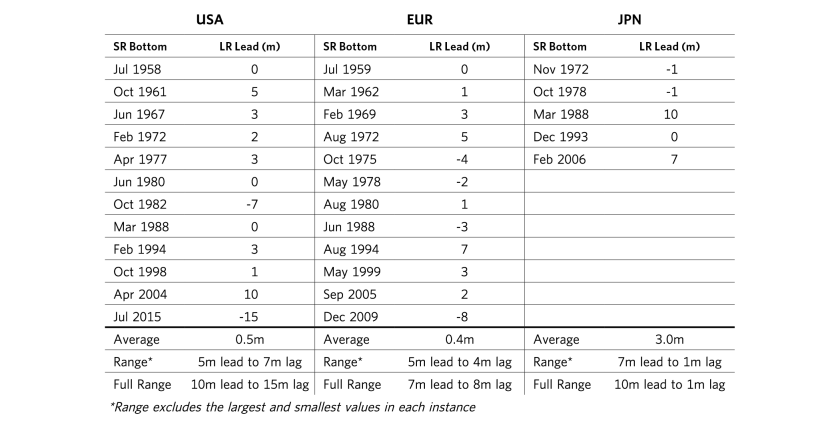

While the policy intentions of the Fed and other central banks are the primary weight holding down bond yields, it is an interesting observation of history that the bond market has not been a far forward discounter of future changes in central bank policy. In fact, even though most rises in short-term interest rates (the Fed’s primary policy tool until recently) have been clearly foreshadowed by the economic conditions that caused them, the history of the bond market is that bond yields haven’t risen until just before the rise in short-term interest rates takes place. The following chart shows the average pattern of US bond yields just before the bottom and initial rise in short-term interest rates in the US across 12 cases since 1955. On average, bond yields have only led the move in short-term interest rates by less than a month.

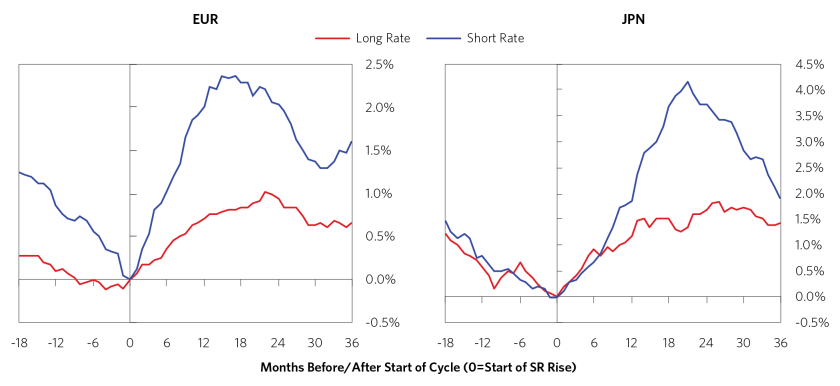

The same tendency has also been the case in Europe and Japan, with an average lead time of less than a month and three months, respectively.

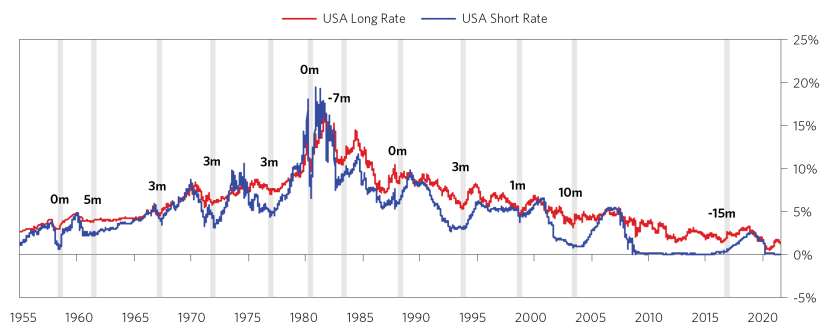

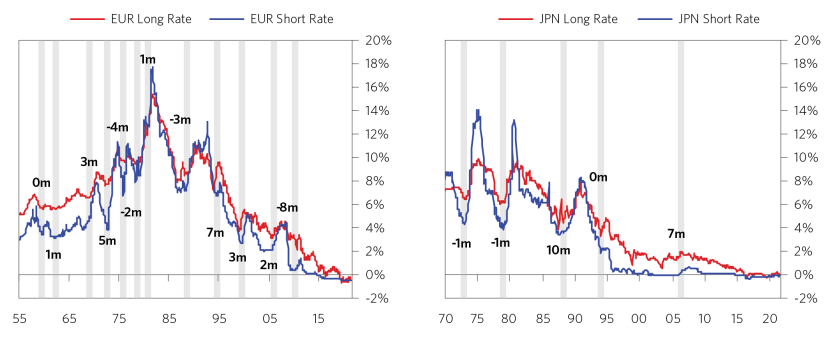

The following charts show all of the cycles in the three economies, with each bottom in short-term interest rates marked in gray and the respective lead or lag time of the bond yield shown.

The following table summarizes all of the cases above. What is remarkable is that the bond market has hardly ever led a rise in short-term interest rates by more than a few months (a negative number means the bond market lagged the rise in short-term interest rates).

Of course, bond markets today are not the same as they have been in the past. Central banks are now major players and are using new tools, like quantitative easing, that add an additional variable beyond short rates for investors to consider (e.g., investors may sell bonds in anticipation of a tapering instead of a short rate tightening). But these changes make bond markets less equipped than ever to discount future conditions correctly. Interest rates are now less a market-based measure of economic conditions and more a reflection of what interest rate level policy makers think will generate their desired economic outcomes. So when we see markets pricing in a continuation of low inflation conditions and very little tightening despite inflationary pressures mounting across inputs and outputs in response to inflationary policies, we think it is likely another time when bond markets are under-discounting the extent of the inflation and tightening that lies ahead.

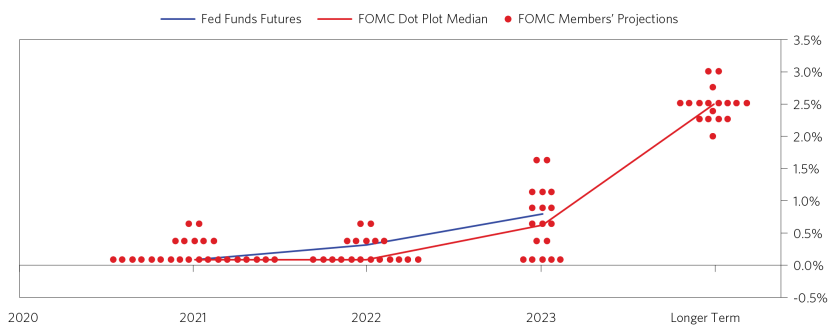

If things play out similarly this time around (i.e., the bond markets don’t move until right about when the Fed does) and if you believe that the Fed will do what they indicate (two big “ifs,” but good to consider), a rise in bond yields would be unlikely for a while, as the Fed has indicated that it will stay easy and continue to lag the economy. However, what is not considered in this scenario is that the Fed will respond to actual conditions as they unfold, and whatever they had previously indicated will have no bearing on what they actually do. Below are the current dot plots, which implicitly reflect an expectation of future economic conditions, including an expectation of a quick transitory path of inflation, which the unfolding evidence increasingly suggests is unlikely.

From a positioning standpoint, the longer it takes for interest rates to rise, the longer the current, very wide spread between nominal income growth and interest rates will persist, which favors high-cash-flow-yielding assets funded by bonds during the intervening period. With respect to our process, continuing to build out a diversified set of ways to capture this is an area of emphasis in our research.

This research paper is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives or tolerances of any of the recipients. Additionally, Bridgewater’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This report is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned.

Bridgewater research utilizes data and information from public, private and internal sources, including data from actual Bridgewater trades. Sources include, the Australian Bureau of Statistics, Bloomberg Finance L.P., Capital Economics, CBRE, Inc., CEIC Data Company Ltd., Clarus Financial Technology, Conference Board of Canada, Consensus Economics Inc., Corelogic, Inc., CoStar Realty Information, Inc., CreditSights, Inc., Credit Market Analysis Ltd., Dealogic LLC, DTCC Data Repository (U.S.), LLC, Ecoanalitica, Energy Aspects, EPFR Global, Eurasia Group Ltd., European Money Markets Institute – EMMI, Evercore, Factset Research Systems, Inc., The Financial Times Limited, GaveKal Research Ltd., Global Financial Data, Inc., Harvard Business Review, Haver Analytics, Inc., The Investment Funds Institute of Canada, ICE Data Derivatives UK Limited, IHS Markit, Impact-Cubed, Institutional Shareholder Services, Informa (EPFR), Investment Company Institute, International Energy Agency (IEA), Investment Management Association, JP Morgan, Lipper Financial, Mergent, Inc., Metals Focus Ltd, Moody’s Analytics, Inc., MSCI, Inc., National Bureau of Economic Research, Organisation for Economic Cooperation and Development (OCED), Pensions & Investments Research Center, Qontigo GmbH, Quandl, Refinitiv RP Data Ltd, Rystad Energy, Inc., S&P Global Market Intelligence Inc., Sentix GmbH, Spears & Associates, Inc., State Street Bank and Trust Company, Sustainalytics, Totem Macro, United Nations, US Department of Commerce, Verisk-Maplecroft, Vigeo-Eiris (V.E), Wind Information(HK) Company, Wood Mackenzie Limited, World Bureau of Metal Statistics, and World Economic Forum. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.