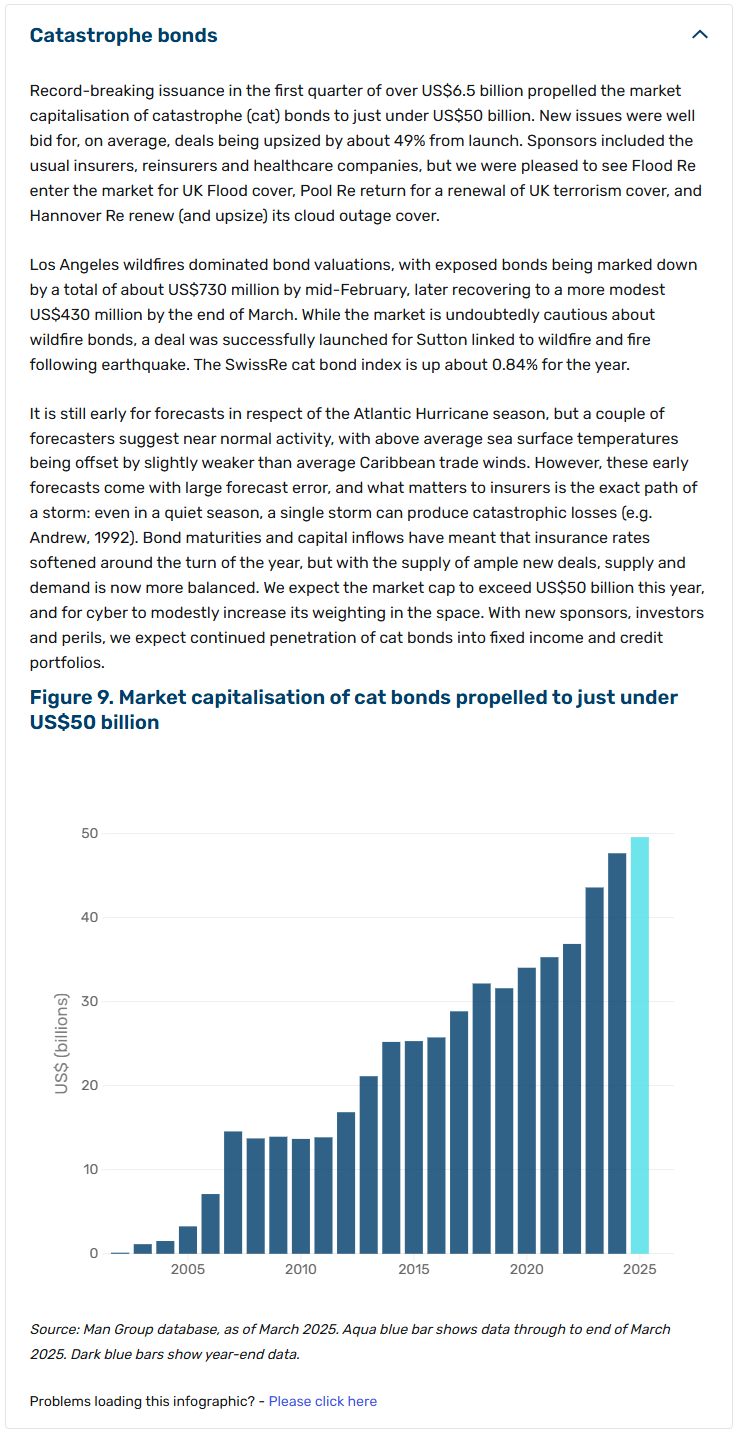

Link para o artigo original: https://www.man.com/insights/q2-2025-credit-outlook-rising-dispersion

Q2 2025: Rising Dispersion, Rising Potential

April 11, 2025

But selectivity will remain key in uncertain markets.

In focus

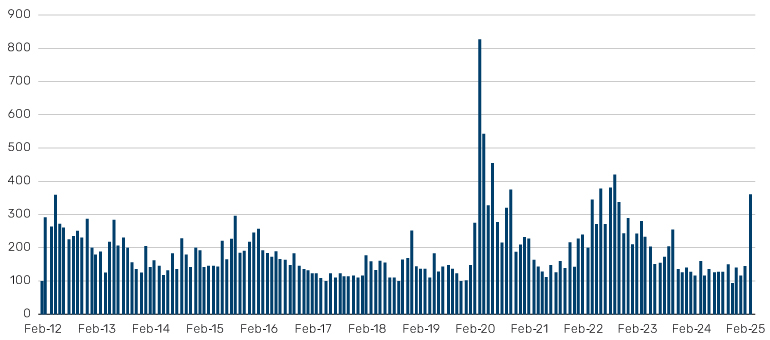

After outperforming in late March, credit largely caught up to equity markets and joined the sell-off in earnest in early April. The uncertainty generated by US President Donald Trump’s ‘Liberation Day’ tariffs, along with the rising likelihood of a recession, drove both a notable increase in spread levels and a resurgence in volatility, which had been absent from credit markets for an extended period.

Figure 1. Rising volatility triggers a significant increase in credit volatility

Source: Bloomberg, as of 7 April 2025. Based on CDX / CBOE NA High Yield One-Month Volatility Index.

Credit has a tendency to overshoot both to the up and downside, but after several quarters of emphasising how tight spreads are, recent repricing may present opportunities. With that said, we believe selectivity continues to be key.

Figure 2. Option-adjusted spreads (OAS) in some areas of credit exceed their 10-year median levels

Source: Bloomberg, ICE BofA, S&P UBS. Based on OAS from 7 April 2015 to 10 April 2025. Loans based on discount margin

Problems loading this infographic? – Please click here

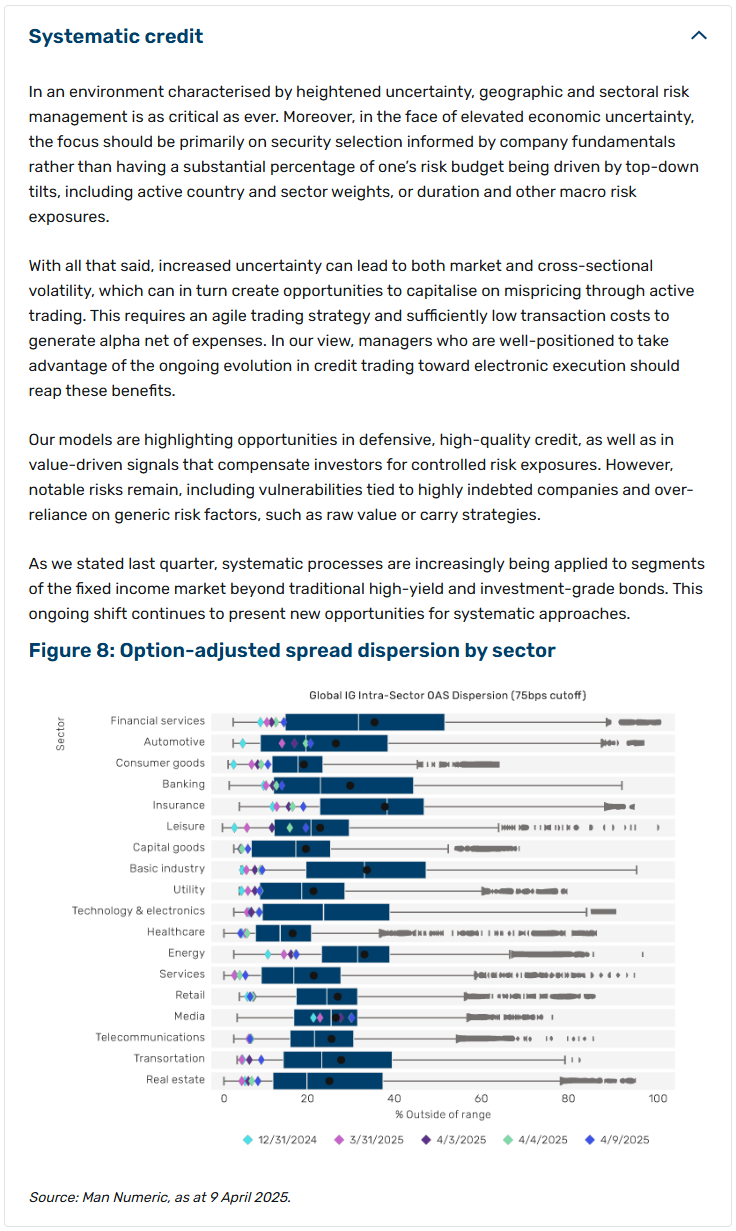

Rising dispersion

The dislocation between Europe and US has been quite telling, with the European market significantly outperforming the US so far. We believe the European market retains several positive drivers and, while it will likely follow the US directionally, we see potential for continued outperformance.

Figure 3: Notable dislocation between Europe and the US

Source: Bloomberg, ICE BofA as of 7 April 2025. Data based on ICE BofA US High Yield Index and ICE BofA Pan European Currency High Yield Index.

Problems loading this infographic? – Please click here

Figure 4. The end of US exceptionalism?

Source: Bloomberg, ICE BofA, as of 7 April, 2025. Data based on ICE BofA High Yield Emerging Markets Corporate Index and ICE BofA US High Yield Index.

Problems loading this infographic? – Please click here

We are seeing similar dislocations within broad sectors and specifically within EM countries, with tariffs potentially creating notable winners and losers.

What are the fundamentals telling us?

Recently, lower quality credit has underperformed higher quality credit, an early sign that greater recession risk is being priced into credit spreads. But is this backed up by the fundamentals?

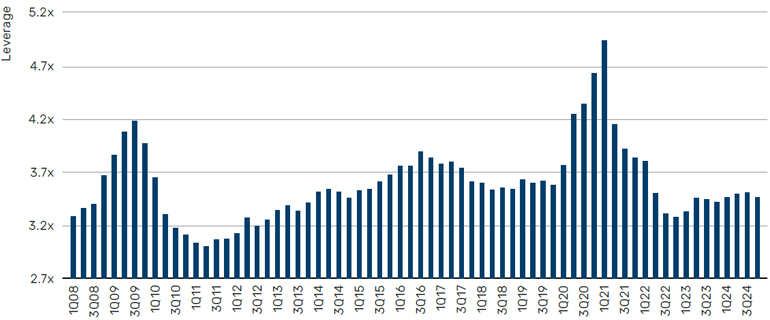

Turning first to the HY market, leverage ratios – the proportion of a company’s debt relative to its earnings – are not particularly worrisome at present, but we expect the pernicious effects of higher interest rates to filter through eventually as companies refinance their debt. Additionally, slowing growth could weigh on earnings, potentially driving leverage ratios higher from here. It may be too soon to assess the impact of tariffs on earnings, but we think it will create greater dispersion within credit markets, leading to the emergence of notable winners and losers. The good news for investors is fundamentals are much more attractive relative to history, particularly if we are approaching the end of the credit cycle.

Figure 5. Leverage ratios are not especially concerning at present…

Source: JP Morgan, as of 31 December 2024.

Figure 6. …but leverage levels by industry is showing more signs of dispersion

Source: JP Morgan, as of 31 December 2024.

Problems loading this infographic? – Please click here

What sets this cycle apart, as illustrated in Figure 6, is that traditionally more defensive sectors like telecoms, cable and healthcare are now among those with the highest debt levels and elevated leverage. As they refinance, their interest burden will become increasingly challenging. In light of this, we expect to see more liability management exercises (LME) in the coming quarters, providing a ripe opportunity for stressed and distressed credit trading.

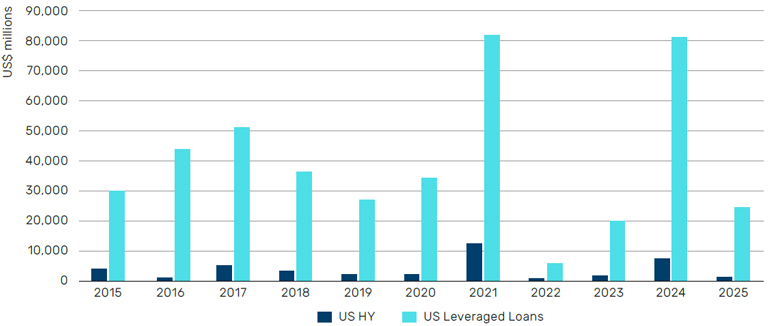

The increase in leverage has been further driven by a growth in equity-monetisation transactions. With the initial public offering (IPO) market relatively barren, private equity (PE) sponsors have reverted to dividend recap transactions – essentially raising debt to pay a special dividend – to help return capital to limited partners (LPs). This has been at the expense of the fundamentals of several portfolio companies. As a result, we are much more cautious about participating in the primary market, though we may re-evaluate these bonds in the future if the opportunity arises to buy at cheaper valuations in the secondary market.

Figure 7. Equity monetisation has increased in both broadly syndicated loans and high yield

Source: BofA Global Research, Pitchbook/LCD, as of 28 February 2025.

Opportunities in private markets

In private markets, US residential credit and middle-market private credit are, in our view, attractive opportunities for investors to explore.

Within US residential credit, we specifically see opportunities in residential transition loans and lender finance. Lender finance provides term loans or warehouse financing to allow originators to provide whole loans to individuals looking to refurbish houses. We believe structural factors limiting US housing supply will mean more of the existing supply will need to be refurbished to meet the needs of new household formation. Lender finance is backed by highly diversified loans and terms of between one and five years, usually floating rate, with an average loan-to-value after refurbishment of 40-50%, making this an investment-grade-equivalent investment. However, the spreads available are anything but ordinary at 300-400 bps1, in our view, and compare favourably to similar-quality areas of public credit markets, such as collateralised loan obligations (CLOs), investment-grade corporates and other parts of the securitised credit market with floating rates.

Last quarter, we highlighted the significance of size in the direct lending market, and this remains a dominant theme. In the upper middle market, the largest borrowers with more than US$100 million in earnings before interest, taxes, depreciation and amortisation (EBITDA) are continuing to pit private credit lenders against the broadly syndicated loan market, resulting in fierce competition and driving spread compression and the loosening of lending terms. In contrast, greater inefficiencies in lending to smaller borrowers and stronger covenants have translated into outperformance and lower defaults in the core middle market, a topic explored in depth in a recent paper.

In summary, we believe there are opportunities across both public and private credit markets, but investors need to be selective, focusing on fundamentals and the underlying data, rather than buying expensive beta in the current environment.

In brief

In depth

At Man Group, we have no house view. Portfolio managers are free to execute their strategies as they see fit within pre-agreed risk limits. With that in mind, click below to expand the Q2 2025 outlooks from our different credit teams.

Public markets

Private markets

1. Source: Man Group.

This information herein is being provided by GAMA Investimentos (“Distributor”), as the distributor of the website. The content of this document contains proprietary information about Man Investments AG (“Man”) . Neither part of this document nor the proprietary information of Man here may be (i) copied, photocopied or duplicated in any way by any means or (ii) distributed without Man’s prior written consent. Important disclosures are included throughout this documenand should be used for analysis. This document is not intended to be comprehensive or to contain all the information that the recipient may wish when analyzing Man and / or their respective managed or future managed products This material cannot be used as the basis for any investment decision. The recipient must rely exclusively on the constitutive documents of the any product and its own independent analysis. Although Gama and their affiliates believe that all information contained herein is accurate, neither makes any representations or guarantees as to the conclusion or needs of this information.

This information may contain forecasts statements that involve risks and uncertainties; actual results may differ materially from any expectations, projections or forecasts made or inferred in such forecasts statements. Therefore, recipients are cautioned not to place undue reliance on these forecasts statements. Projections and / or future values of unrealized investments will depend, among other factors, on future operating results, the value of assets and market conditions at the time of disposal, legal and contractual restrictions on transfer that may limit liquidity, any transaction costs and timing and form of sale, which may differ from the assumptions and circumstances on which current perspectives are based, and many of which are difficult to predict. Past performance is not indicative of future results. (if not okay to remove, please just remove reference to Man Fund).