Featured Authors

Armen Panossian

Armen Panossian

Head of Performing Credit and Portfolio Manager

Danielle Poli, CAIA

Danielle Poli, CAIA

Managing Director, Multi-Asset Credit Product Specialist and Head of the Product Specialist Group

SHIFTING GEARS

“While today’s uncertain macroeconomic and geopolitical environment is creating risk in securities markets – particularly for fixed-rate assets – we believe it’s also generating compelling opportunities for investors able to withstand a bumpy ride.”

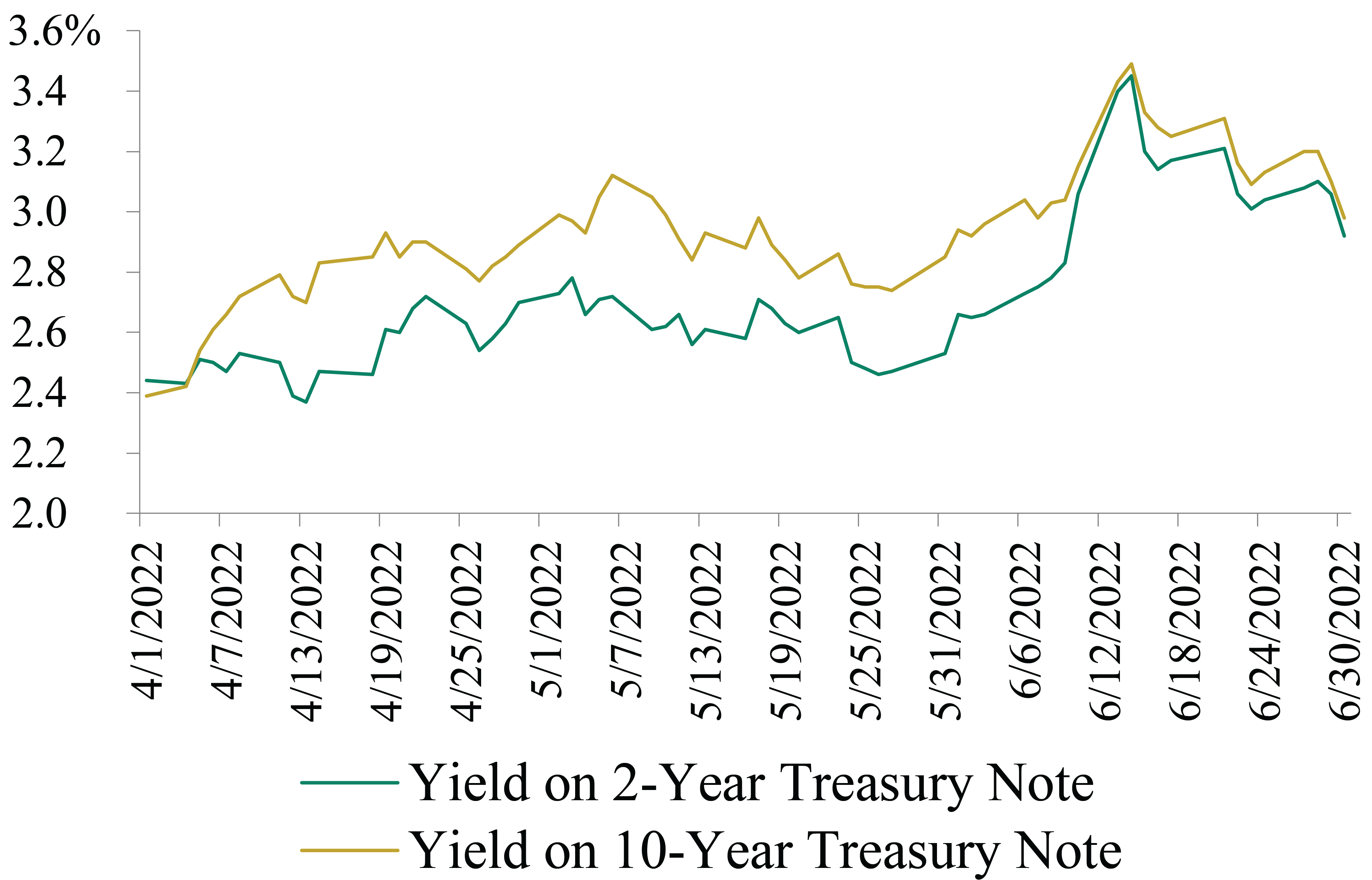

The second quarter gave investors an object lesson in how quickly market expectations can change. Rising U.S. interest rates were the driving force behind the sharp price declines suffered by fixed-rate assets throughout most of the period. The yield on the 10-year Treasury note rose by 83 basis points in the quarter through June 10, before spiking by an additional 28 bps on June 13, after the Wall Street Journal reported that the Federal Reserve was considering increasing the fed funds rate by 75 bps – the largest hike in almost three decades. (See Figure 1.) However, when the Fed followed through with this aggressive move, investors’ focus quickly shifted: the risk of a recession in the U.S. – not rising interest rates – suddenly took center stage. Consequently, the yield on the 10-year Treasury note fell by 45 bps between June 13 and June 30, while yield spreads widened across credit asset classes.1

As we assess recession risk and how an economic downturn might impact credit markets, we’re reminded of something Howard Marks recently wrote in his memo Bull Market Rhymes:

The price of an asset is based on fundamentals and how people view those fundamentals. So the change in an asset price is based on a change in fundamentals and/or a change in how people view those fundamentals.

The fundamentals of the U.S. economy have clearly weakened in 2022, as reduced fiscal largesse, tightening monetary policy, and rising prices have weighed on consumption. But these negative trends have been building for some time. What has shifted more dramatically of late is how investors interpret these fundamentals. Such interpretations are liable to remain volatile as long as the macroeconomic picture remains murky. So the road ahead could be bumpy, as we noted in Performing Credit Quarterly 1Q2022. But we believe credit investors with intestinal fortitude and the skill to navigate this landscape could find opportunities to pull ahead of those who are desperately looking for an exit ramp.

Figure 1: U.S. Treasury Yields Were Volatile in 2Q2022

Source: U.S. Department of the Treasury

THE “R” WORD

“A significant decline in economic activity that is spread across the economy and that lasts for more than a few months.”

– Definition of “Recession,” National Bureau of Economic Research (NBER)

When assessing the risk of a recession, it’s useful to consider what the term actually means. Many people believe it refers to two consecutive quarters of negative GDP growth. By this definition, the U.S. economy may already be in a recession. The U.S. economy shrunk by 1.4% in the first quarter, and the Federal Reserve Bank of Atlanta’s GDPNow tracker currently indicates that the economy has contracted by 1.5% in the second quarter.

But even if the Atlanta Fed’s estimate is accurate, that doesn’t mean the economy is officially in a recession. NBER (the private, nonpartisan organization that formally decides when recessions begin and end) focuses on the depth, diffusion, and duration of economic weakness when making its determinations. To do this, the organization considers many economic indicators – not just GDP growth – such as employment gains, real personal income, consumption, and industrial production.

So how is the broad U.S. economy faring? Many indicators have been flashing red in recent months:

-

Industrial production declined by 0.2% in June. Manufacturing output (a component of industrial production) fell for the second-consecutive month.2

-

Retail sales indicate that inflation-adjusted consumption is slowing: In June, retail sales rose by 1.0% month-over-month. However, this increase was largely driven by rising gasoline prices in early June, as retail sales aren’t adjusted for inflation. Retail sales rose by 7.7% year-over-year, slower than the 9.1% inflation rate over the same period. Retail sales in May declined by 0.1% versus the prior month.3

-

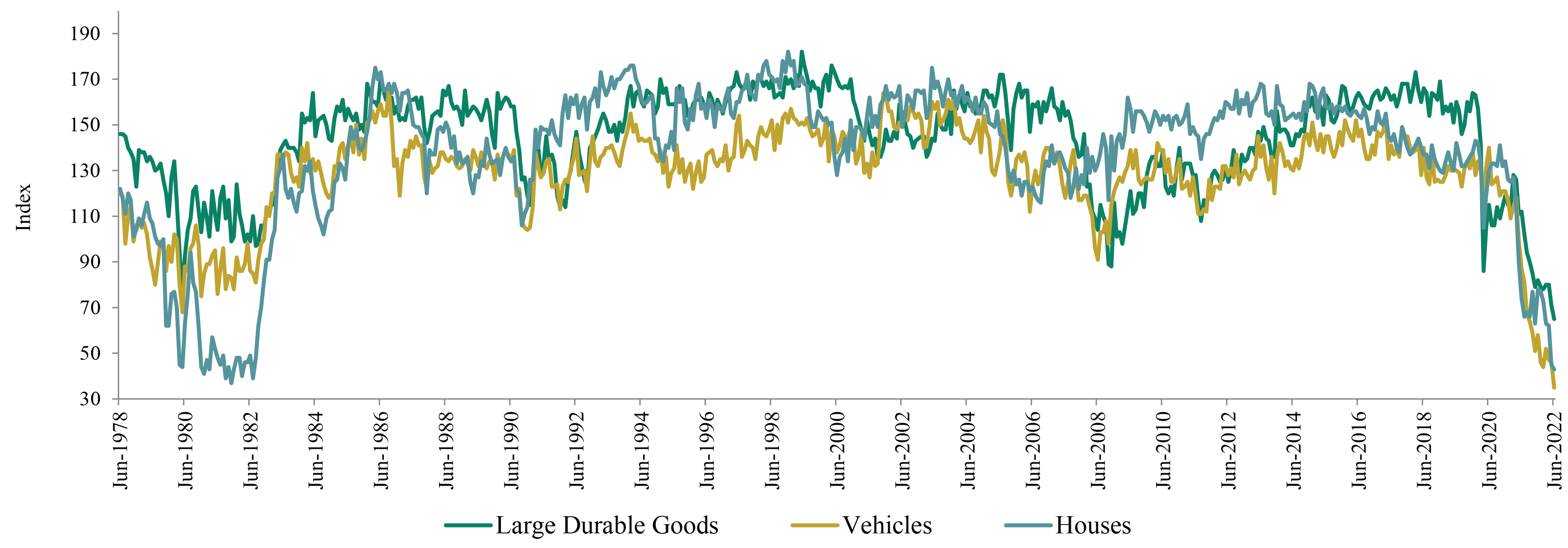

Buying conditions for cars, houses, and large durable goods fell to multi-decade lows in June, meaning the vast majority of respondents to the University of Michigan consumer survey believe it’s a bad time to buy the above. (See Figure 2.)

-

Average hourly wages increased by 5.1% in the 12 months through June, well below the 9.1% increase in prices during that period.4

-

35% of households are having trouble paying their bills, an increase of 10 percentage points versus the figure last year, according to the U.S. Census Bureau’s Household Pulse Survey.

-

Consumer sentiment about the economy has dropped to a 40-year low, according to the University of Michigan survey. (However, it’s worth noting that while the overall trend in sentiment is clearly negative, the magnitude of the decline may be skewed by political biases. For context, in June 1980, the difference between sentiment figures for self-identified Democrats and Republicans was 4.1 points. The gap is currently 31.5 points. This is another reminder of how people can interpret the same fundamentals very differently.)

Figure 2: Buying Conditions for Vehicles, Homes, and Large Durables Have Plummeted

Source: University of Michigan Survey of Consumers

Another way to identify a recession is the Sahm Rule, which states that a recession has begun when the three-month moving average of the unemployment rate has increased by at least 0.5 percentage points relative to the low in the prior 12 months. By this measure, the U.S. is currently nowhere near a recession. In June, the unemployment rate remained at 3.6%, near the 50-year-low, and the U.S. economy added 372,000 jobs, in line with the average monthly increase of 383,000 jobs in the previous three months and well above the pre-pandemic norm.5

But, once again, there is more than one way to interpret an economic data point. On the one hand, robust job growth indicates that consumers should continue to have money to spend. On the other hand, a tight labor market could produce wage inflation that would pressure the Fed to continue aggressively hiking interest rates. The risk posed by the Fed itself is tremendous, as it has rarely been able to reduce the inflation rate without causing a recession, and it has never done so with inflation running as high as it is currently.

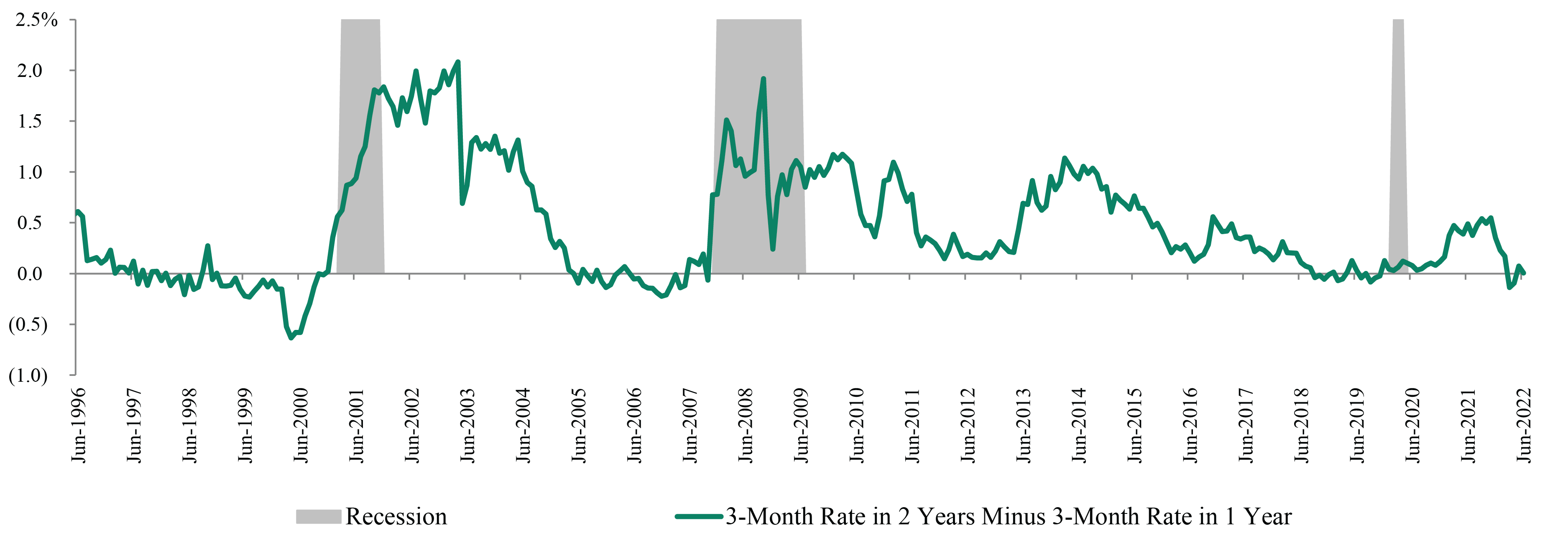

Investors don’t appear to have much confidence in the Fed’s ability to engineer this so-called soft landing. Money markets are indicating that the Fed will raise interest rates significantly in the next few months but then begin cutting them as early as next year, a monetary policy pattern typically associated with recessions. Moreover, in the last 25 years, a recession has often occurred after the expected short-term interest rate in two years has fallen below the expected short-term interest rate in one year. This inversion has recently taken place. (See Figure 3.)

Figure 3: Forward Curve Signals that Recession Risk Is Increasing

Source: Bloomberg

NOT-SO-HARD LANDING?

There are many assumptions baked into current credit and equity prices. Investors appear to believe U.S. inflation will slow enough by early next year that the Fed will not only be able to stop hiking interest rates but will also be able to cut them without further eroding confidence in its ability to keep inflation near its 2.0% target. Moreover, both yield spreads in below-investment grade credit and earnings assumptions embedded in equity prices suggest that investors believe any recession in the coming year will be mild. Indeed, high yield bond spreads have narrowed in July, despite recession concerns. Additionally, the gap between yield spreads of European high yield bonds and their U.S. counterparts is wider than average but not enormous, indicating that investors don’t believe the conflict in Ukraine will escalate dramatically. A host of risks could undermine these expectations:

-

If Russia cuts off natural gas supplies to Europe, economic activity in the latter could plummet, as many European countries would be forced to ration energy. If this scenario occurs, the German economy could contract by 3.0% in 2023, according to Germany’s Bundesbank. Moreover, if Russia removes significant oil supply from the market – potentially in retaliation against the U.S.-led effort to cap the price of Russian oil – global oil prices would spike, adding to global inflationary pressures and economic weakness. Importantly, western sanctions haven’t reduced Russian oil exports significantly thus far but have instead redirected them, most notably to China.6 Therefore, Russia has been flooded with hard currency in recent months and has consequently seen its currency appreciate massively against the U.S. dollar. This relative strength could embolden Moscow to act aggressively. Finally, the war itself – which involves a nuclear-armed country – continues to represent a serious threat on many fronts.

-

Wheat prices have fallen recently, but numerous factors – such as high fertilizer prices, export restrictions, labor supply shortages, and the La Niña weather pattern – could put upward pressure on food price inflation in the coming year.

-

Elevated food and energy prices are increasing political discontent in many countries. Historically, high food prices have frequently preceded bouts of civil unrest.

-

Rental housing costs – which constitute roughly one-third of CPI7 – could keep U.S. inflation elevated in the medium term, as they’re calculated with a lag and prices have increased substantially in the last year.

-

China’s zero-Covid policy could continue to negatively impact the world’s second-largest economy, which grew by only 0.4% in the second quarter – the weakest growth since 1Q2020.8 Future lockdowns could also damage the economic health of China’s major trading partners, including Germany, which recently recorded its first trade deficit in 20 years, partly because of reduced demand in China.

-

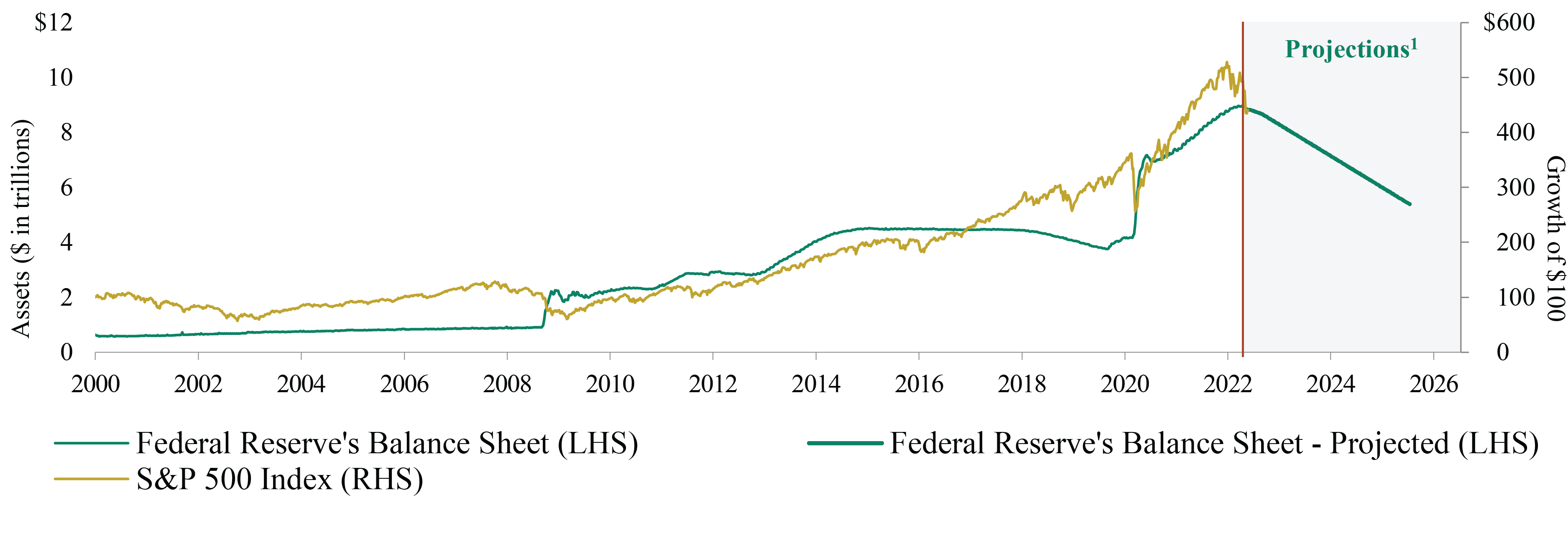

Quantitative tightening could weigh heavily on financial markets. Securities prices recovered quickly after both the Global Financial Crisis of 2008-09 and the Covid-19 shock in 2020, primarily because the Fed pumped massive liquidity into the financial system. (See Figure 4.) However, the U.S. central bank is now reducing liquidity by shrinking its balance sheet. It’s unclear how much latitude the Fed will have to support markets in an economic slowdown this time around, especially if inflation remains elevated.

Figure 4: U.S. Equity Returns Have Been Correlated with the Fed’s Balance Sheet Expansion

Source: Board of Governors of the Federal Reserve System, Bloomberg

NAVIGATING THE ROAD AHEAD

At Oaktree, we’ve long believed that some of the best potential bargains can be found in market environments where risk aversion has taken over from risk tolerance. We don’t think this transition has fully transpired, but the tide is turning. Moving forward, we believe investors will be well positioned if they have (a) the ability to conduct detailed bottom-up credit analysis and (b) the flexibility and fortitude to take advantage of attractive opportunities, wherever they arise.

(1) High yield bond spreads could widen significantly in an economic downturn, potentially offering attractive compensation for the modest default risk.

Yield spreads in the U.S. high yield bond market widened by more than 260 bps in the first half of 2022 to reach almost 600 bps, reflecting investors’ increasing pessimism about the economic outlook.9 Breaching 500 bps is noteworthy, as doing so has historically signaled that further spread widening is likely.

However, near-term default risk in the asset class remains low. First, issuers face few maturities over the next 12 months. Second, while many issuers’ fundamentals have been negatively impacted by rising input costs in 2022, most still have fairly strong cash balances and manageable interest expenses. Over 36% of U.S. high yield bond issuers had a coupon of less than 5.0% at quarter-end, compared to 16.0% at year-end 2019.10 Finally, quality (indicated by credit ratings) in the high yield bond market has increased over the last decade. Bonds with a credit rating of BB (the level just below investment grade) now constitute 53% of the U.S. high yield bond market, compared to 43% in 2012, and bonds in the lowest ratings category (CCC) currently make up under 11%.11

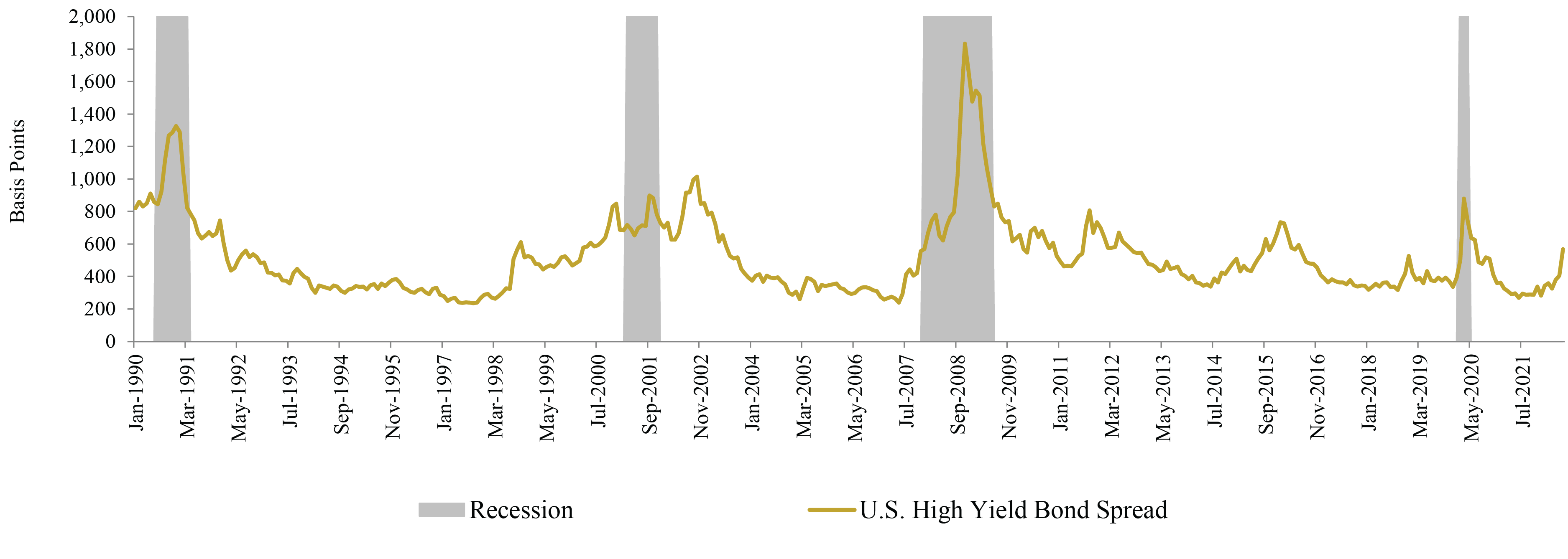

Looking forward, we believe yield spreads could expand from current levels if the U.S. economy enters into a recession, even if defaults don’t spike. During significant corrections in the U.S. high yield bond market in the last 25 years, yield spreads have typically ballooned to over 1,000 bps. (See Figure 5.) These wide yield spreads reflected default expectations that proved to be excessively pessimistic, so high yield bond investors that were able to deploy capital during the downturns were in a position to scoop up tremendous bargains. High yield bond spreads might not reach 1,000 bps this time around – as the average price in the market is already well below par – but history suggests that yield spreads might have plenty of room left to widen in this cycle.

Figure 5: High Yield Bond Spreads Remain Well Below the Recessionary Average

Source: Bloomberg U.S. Corporate High Yield Index

(2) CLOs may offer attractive relative value, due to rising yields and structural protections.

Yields of collateralized loan obligations (CLOs) have increased markedly in the first half of 2022, offering what we believe to be significant compensation for credit risk. BBB- and BB-rated CLOs yielded 8.1% and 12.6%, respectively, as of June 30, compared to 4.9% and 8.5% at the end of 2021.12 Moreover, yield spreads ended the second quarter near the widest they’ve been since December 31, 2020. Notably, BB-rated CLOs were offering a premium of 497 bps over similarly rated high yield bonds, as of quarter-end, even though the probability of one issuer defaulting is greater than the likelihood of many defaulting at the same time.13

If interest rates in the U.S. continue to rise and remain elevated through 2023, some holders of the underlying loans may face liquidity issues, especially those in industries – such as technology – in which average leverage is high. But default rates for CLOs have historically remained low, even in challenging economic environments, including the Global Financial Crisis. This is partly because CLOs include structural protections that can provide a reasonable cushion in an economic downturn. In order for a typical BB-rated CLO to incur losses, approximately 30% of the underlying loans would need to default. 14

However, during a broad market sell-off, CLOs often suffer significant mark-to-market losses, as investors seek to shed all assets perceived to be risky. But such a dislocation could present an attractive opportunity for disciplined investors, as prices typically decline far more severely than credit fundamentals.

(3) Prudent private credit investors could potentially outperform investors who’ve become overly reliant on leverage facilities.

In recent years, many direct lending funds have attempted to compensate for falling unlevered returns by increasing their use of leverage facilities provided by banks. However, as Oaktree has long noted, using leverage to produce adequate returns is a dangerous game. If a substantial portion of a direct lender’s return is tied to financial flexibility, then such an investor could be vulnerable in an economic downturn, as such flexibility often declines at the worst possible moment.

If a market dislocation occurs, banks could potentially pull private lenders’ leverage facilities. Lenders would then need to raise liquidity and would likely sell their top-performing assets that could still command a reasonable price. These lenders might then be left with poorly performing assets and still have significant leverage to repay.

Such an environment could benefit private lenders who have taken a more cautious approach to leverage. They might be better positioned to provide rescue financings or other solutions at attractive levels, while also securing strong lender protections.

ASSESSING RELATIVE VALUE

PERFORMANCE OF SELECT INDICES

As of June 30, 2022

Sources: Bloomberg Barclays, Credit Suisse, FTSE, ICE BofA, JP Morgan, S&P Global, Thomson Reuters15

DEFAULT RATES BY ASSET CLASS

Sources: Bank of America, Credit Suisse, JP Morgan16

STRATEGY FOCUS

HIGH YIELD BONDS

Market Conditions: 2Q2022

U.S. HIGH YIELD BONDS

Return: -9.9%17

Issuance: $24.6bn18

LTM Default Rate: 0.8%19

-

Rising interest rates weighed on fixed-rate assets in 2Q2022: High yield bonds reported the weakest quarterly performance since the beginning of the Covid-19 pandemic. Approximately 70% of U.S. high yield bonds offered yields above 7% at quarter-end, compared to roughly 19% as of March 31.20

-

Numerous risks caused yield spreads to widen: Yield spreads expanded by around 220 bps during the quarter, due primarily to the increasingly pessimistic economic outlook, elevated inflation, and geopolitical uncertainty.21

-

The default environment remains benign: Although defaults increased marginally during 2Q2022 compared to the prior quarter, the default rate remains well below the long-term average.

EUROPEAN HIGH YIELD BONDS

Return: -11.4%22

Issuance: €4.5bn23

LTM Default Rate: 0.01%24

-

Yield spreads are attractive on a relative basis: They’re at the widest level since the onset of the Covid-19 pandemic and offer a premium of nearly 100 bps over U.S. high yield bond spreads.25

-

Extremely poor performance among a small subset of bonds dragged down the asset class’s overall return: This phenomenon amplified the price pressure caused by the broad reduction in investors’ risk appetite and ongoing concerns about geopolitical risk.

Outlook

Opportunities

-

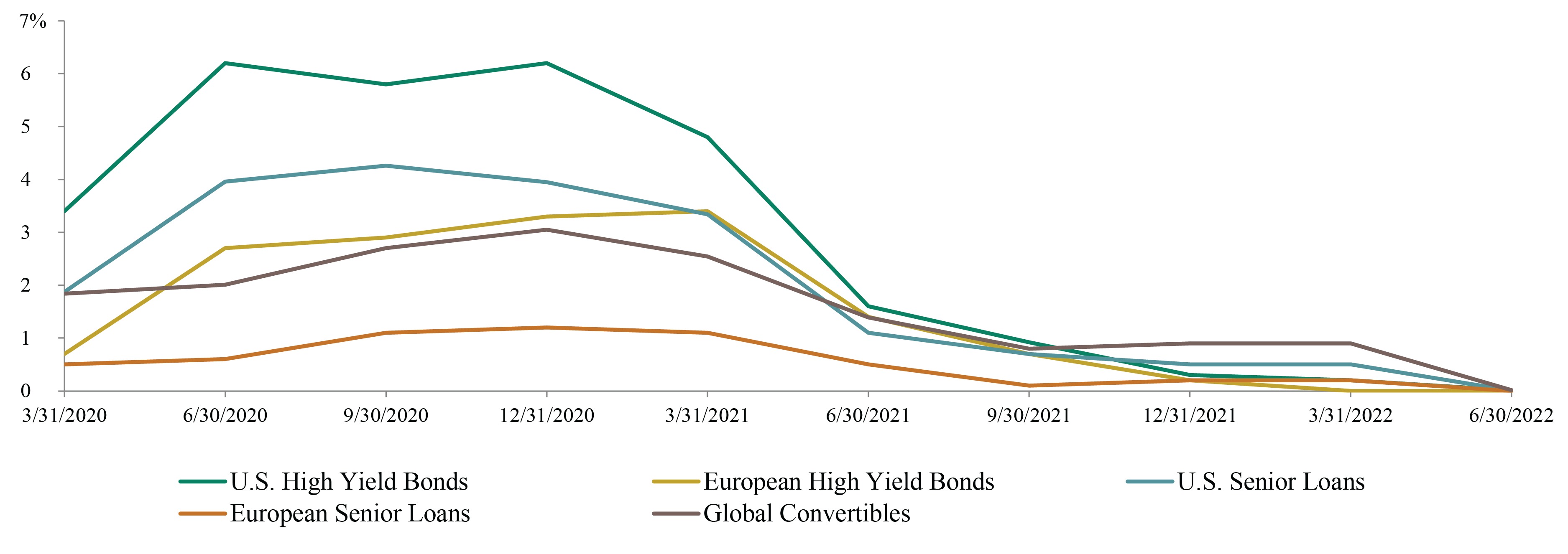

Yields have increased, but default risk remains low: In 2Q2022, yields rose in the U.S. and European high yield bond markets by 280 bps and 320 bps, respectively.26 (See Figure 6.) While analysts anticipate that default rates in the U.S. and European high yield bond markets will increase in 2022, they expect these rates to remain well below their long-term historical averages.27 Issuers’ fundamentals are fairly healthy despite the slowdown in economic growth, and near-term maturities are minimal following the 2020–21 wave of refinancings.

-

Covenant-lite loans are providing highly leveraged U.S. companies with flexibility: In recent years, high yield bond issuers have had ample access to loans with few restrictions or requirements (i.e., cov-lite loans). While such borrowing may increase risk in the long term, access to this relatively unrestricted source of capital makes bond/loan issuers less likely to default on their bonds in the near term.

Risks

-

Tightening monetary policy could harm heavily indebted companies: Low-rated corporate issuers might struggle to roll over debt if rising interest rates and quantitative tightening cause a significant slowdown in the economy. This could cause default rates to increase more than analysts currently anticipate.

-

Elevated inflation could impair issuers’ fundamentals: Companies facing rising input costs may be unable to pass along price increases to customers. Reduced earnings could negatively impact leverage ratios and potentially lead to credit ratings downgrades.

-

Credit risk appears to be higher in Europe: We believe the likelihood of a recession in 2022 is higher in Europe than in the U.S., given the former’s proximity to the war in Ukraine as well as energy security concerns.

Figure 6: High Yield Bonds Are Offering Potentially Attractive Yields and a Low Average Price

Source: ICE BofA Non-Financial Developed Markets High Yield Constrained Index and ICE BofA Global High Yield European Issuers Non-Financial Excluding Russia Index

SENIOR LOANS

Market Conditions: 2Q2022

U.S. SENIOR LOANS

Return: -4.4%28

Issuance: $60.6bn29

LTM Default Rate: 0.7%30

-

U.S. loans weakened in 2Q2022, as the economic outlook worsened: However, loans outperformed most other asset classes, and prices were far less volatile. (See Figure 7.)

-

Retail investors reduced their exposure to the asset class: Loan mutual funds and loan ETFs recorded outflows in May and June, following 17 consecutive months of inflows. Outflows for the quarter totaled $3.1bn.31

-

The default environment remains benign: The U.S. trailing-12-month default rate increased by 29 bps quarter-over-quarter to 0.68%, but it remains well below the long-term historical average of 3.1%.32

EUROPEAN SENIOR LOANS

Return: -6.3%33

Issuance: €9.0bn34

LTM Default Rate: 0.2%35

-

European loans weakened in 2Q2022: While the asset class was resilient in 1Q2022, performance declined sharply in the second quarter, as investor risk appetite declined and CLO formation stalled.

-

Relative outperformance versus European high yield bonds continued: Loans benefited from having floating rates, as investors priced in higher interest rate expectations.

-

Investors reassessed credit risk: Yield spreads in the asset class widened by more than 250 bps during the quarter, with the most significant widening in CCC-rated loans.36

Outlook

Opportunities

-

Rising interest rates should support relative performance: Credit investors will likely seek to limit duration as the Federal Reserve, European Central Bank, and Bank of England tighten monetary policy, making floating-rate loans in both regions more attractive relative to fixed-rate assets.

-

Loans’ core buyer base is stable: Volatility in loans is usually lower than in other asset classes because (a) CLOs – the primary holders – have limited selling pressure and (b) the cash settlement period for loans is lengthy, so the asset class tends to attract long-term institutional investors.

Risks

-

Rising interest rates could prove challenging for highly indebted borrowers: The reference rates used in many loan contracts have risen significantly, making it more expensive for borrowers to service their debt.

-

Tightening central bank policy and the war in Ukraine could impede economic growth and increase defaults: While default risk remains muted, tail risk is growing – especially in Europe – highlighting the importance of disciplined credit selection.

-

High inflation could harm companies’ fundamentals: Borrowers may struggle to pass along cost inflation to customers, a trend that could negatively impact companies’ earnings and leverage ratios. European borrowers in particular may be vulnerable, as energy prices are likely to remain high.

-

Loan quality has declined in recent years: Issuer-friendly loans may have encouraged imprudent borrowing, which could prove problematic in an economic downturn. Loan-only issuers, which have increased by 178% since the beginning of 2013, could be the most vulnerable, as their average credit rating is far lower than that of bond-and-loan issuers.37

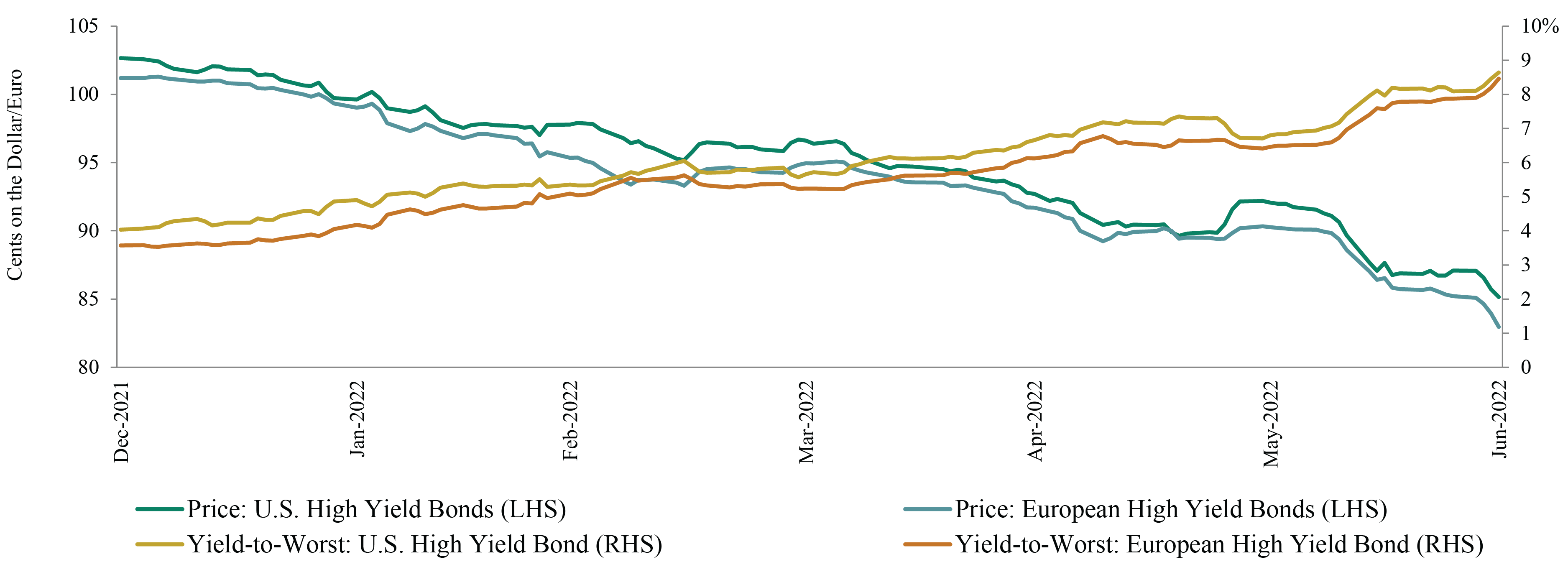

Figure 7: Loans Have Experienced Less Volatility than Fixed-Rate Debt

Source: Credit Suisse, Bank of America, FTSE, U.S. Department of the Treasury

EMERGING MARKETS DEBT

Market Conditions: 2Q2022

EM Corporate High Yield Bond Return: -7.1%38

-

Rising interest rates and rampant global inflation weighed heavily on EM debt: The asset class recorded the worst 1H performance ever.39 EM bonds with relatively long duration underperformed as many central banks tightened monetary policy.

-

Geopolitical risk has amplified fears that global growth could slow down materially: EM high yield bond spreads widened in recent months, as the war in Ukraine heightened investor concerns about inflation and the global economic outlook. Yield spread expansion accelerated near quarter-end, with more than 100 bps of widening recorded in June.40 (See Figure 8.)

-

Liquidity declined significantly, as demand for EM debt plummeted: In 2Q2022, new issuance slowed to the weakest pace since 2010, and year-to-date outflows from EM debt hard-currency funds increased to roughly $18bn.41

-

The increase in the EM debt default rate was driven by weakness among issuers in Eastern Europe and China: The EM YTD high yield bond corporate default rate reached 4.3% in mid-May.42 The war in Ukraine led to widely anticipated defaults in European EM debt, including the Russian government’s first default since 1998. China’s high yield bond market had experienced $49bn in defaults in the year through mid-May, due to stress in the country’s property sector that has been exacerbated by Covid-19 lockdowns.43

Outlook

Opportunities

-

Broad market weakness may create compelling buying opportunities: Outflows from the asset class could cause the debt of companies with strong fundamentals to trade at dislocated prices. Extensive credit analysis may help investors identify securities that can offer favorable risk-adjusted returns. Companies that can generate consistent cash flow may be well positioned in an environment in which access to financing is limited.

-

Latin American corporates may prove resilient, but political risk remains: The region could outperform other EM geographies because it benefits from high commodity prices and is fairly well insulated from geopolitical tensions in Europe. However, asset prices could be negatively impacted by risk surrounding the rise in populism in the region.

Risks

-

The broad decline in credit investors’ risk appetite could cause a more significant dislocation in EM debt: If the global economy slows, outflows from EM debt retail funds could accelerate, primary market activity could decrease further, and defaults could increase.

-

China’s zero-Covid policy may continue to weigh on the country’s economic growth: While lockdowns in several large Chinese cities have ended, the government remains committed to its zero-Covid policy. Further lockdowns could negatively impact economic activity in multiple sectors, including real estate.

-

Developed market central banks could continue to tighten monetary policy: EM countries and companies may struggle to roll over and service debt in a rising-interest-rate environment.

-

Geopolitical risks could intensify: The war in Ukraine, rising populism in Latin America, and instability in Turkey could erode investor confidence in EM credit.

Figure 8: Widening Yield Spreads Are Now Driving the Weakness in EM High Yield Debt

Source: Bloomberg

GLOBAL CONVERTIBLES

Market Conditions: 2Q2022

Return: -12.2%44

Issuance: $3.3bn45

LTM Default Rate: 1.4%46

-

The asset class’s performance continued to decline in 2Q2022: Most global equity markets weakened during the period, which caused convertible bond prices to fall. Investor concerns mounted about surging global inflation and the potential for the U.S. and global economies to contract in 2022 or 2023.

-

Growth-oriented equities underperformed: The convertibles market has significant exposure to high-multiple, high-growth issuers, which have been negatively impacted by rising interest rates.

-

Primary market activity stalled in 2Q2022: Global new issuance of convertibles totaled only $3.3bn during the quarter, bringing year-to-date issuance to $11.2bn, the lowest volume on record for the first half of a year.47

Outlook

Opportunities

-

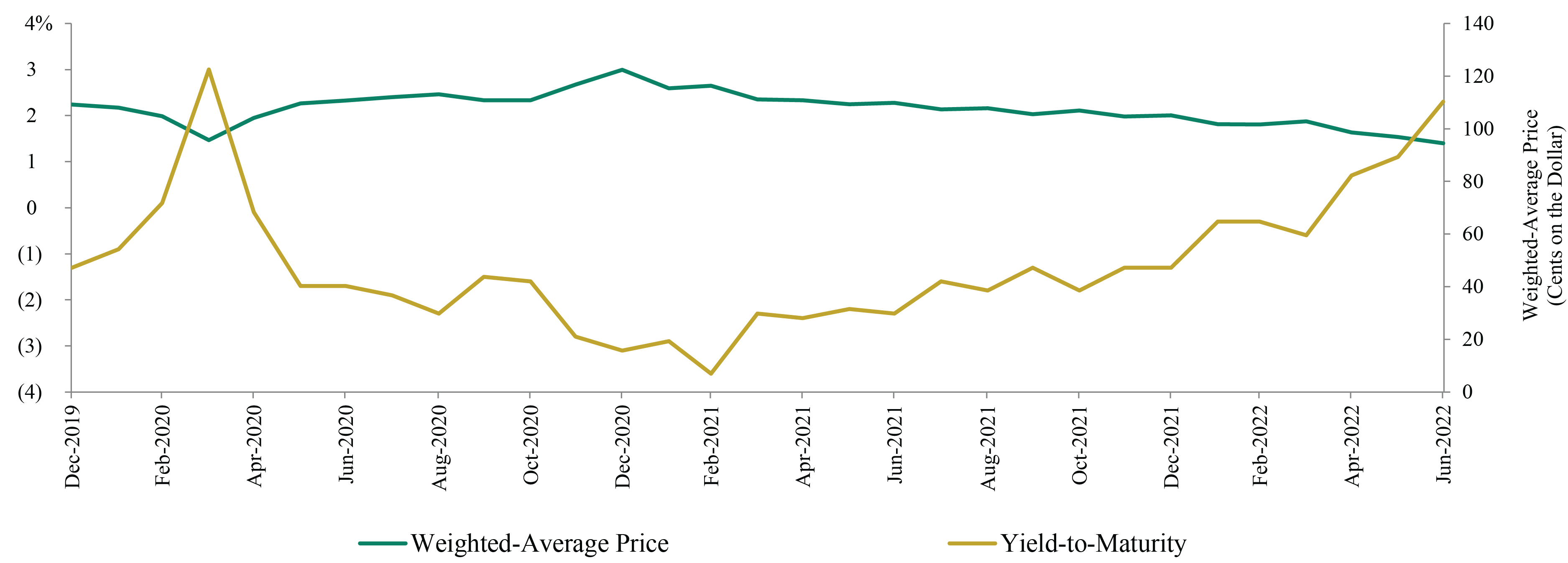

Yields on convertibles rose as monetary policy tightened and concern about global economic growth increased: The asset class’s yield-to-maturity rose by 290 bps during the quarter to reach 2.3%. (See Figure 9.)48

-

The convertibles universe remains broad and diverse: While primary market activity slowed in 2022, robust issuance in the previous two years has provided an expansive opportunity set to investors who are seeking to locate value under challenging market conditions.

-

Market weakness could create attractive buying opportunities: Value-oriented investors may be able to identify bargains in this environment, as an increasing number of convertibles are trading below par. (See Figure 9).49

Risks

-

Numerous trends threaten to slow economic growth globally and push down equity prices: These include the war in Ukraine, high commodity prices, elevated inflation, declining consumer sentiment, the Chinese government’s zero-Covid policy, tightening global monetary policy, and the reduction in fiscal support in most major economies.

-

High-multiple equities remain vulnerable: Convertibles are highly exposed to growth-oriented stocks, which may continue to decline in price if U.S. interest rates keep rising.

Figure 9: The Convertibles Market Is Now Offering Positive Yields and an Average Price Below Par

Source: Refinitiv

STRUCTURED CREDIT

Market Conditions: 2Q2022

CORPORATE

BB-Rated CLO Return: -6.9%50

BBB-Rated CLO Return: -5.9%51

U.S. CLO Issuance: $41.1bn52

European CLO Issuance: €4.0bn53

-

Primary market activity has picked up slightly in 2Q2022: Issuance in the U.S. totaled $41.1bn in the period, an increase compared to 1Q2022 but well below the 2Q2021 level. Meanwhile, European primary markets have stalled: Only €4.0bn priced during the period.54

-

Geopolitical risk and tightening monetary policy weighed on prices: Concerns about the global economy and decreased trading activity have negatively impacted the asset class, though corporate structured credit performed far better than primarily fixed-rate asset classes.55

REAL ESTATE

BBB-Rated CMBS Return: -4.9%56

-

The primary market has slowed since April: Year-to-date issuance of commercial mortgage-backed securities totaled $73.9bn at quarter-end, well above the $65.0bn recorded in the same period in 2021. The increase was primarily driven by issuance of single asset single borrower CMBS and CRE CLOs.57 However, decreased demand for AAA-rated tranches has caused issuance to slow in recent months.

-

Yield spreads have widened: Rising interest rates, the lingering pandemic, and the broad decline in risk appetite weighed on commercial real-estate-backed securities.

Outlook

Opportunities

-

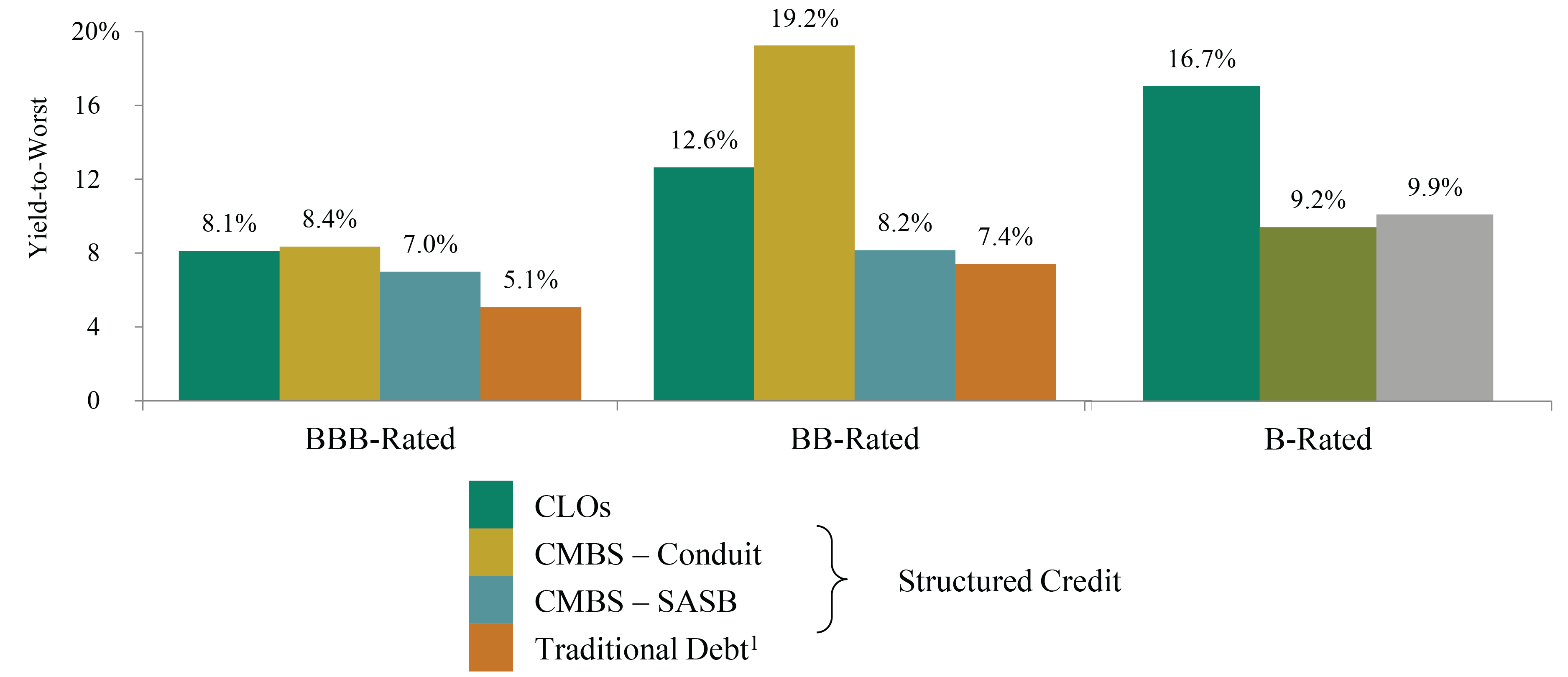

BB-rated CLO debt tranches have many sources of potential value: These instruments have attractive structural and credit enhancements as well as low sensitivity to interest rates increases. Structured credit continues to offer higher average yields than traditional credit asset classes. (See Figure 10.)

-

Weakness in real-estate-backed securities may create compelling opportunities for disciplined investors: We believe the risk/return profile for SASB CMBS and conduit CMBS is improving, but we also think disciplined credit analysis is necessary in this challenging environment.

Risks

-

CLOs have historically performed poorly during bouts of equity market weakness: Performance could continue to be negatively affected by numerous factors: the conflict in Ukraine and related energy security concerns in Europe, rising inflation, tightening monetary policy, slowing global growth, and the decline in investor risk appetite.

-

Widening yield spreads could limit primary market activity in real-estate-backed securities: Issuers may be unwilling to offer the yields demanded by investors, limiting the opportunity set.

Figure 10: Structured Credit Offers Higher Yields Than Most Traditional Debt

Source: Bloomberg Barclays Index Services, FTSE Global Markets, Credit Suisse, JP Morgan

PRIVATE CREDIT

Market Conditions: 2Q2022

-

Direct lending has benefited from investor demand for floating-rate debt: Rising interest rates have made private debt with floating rates attractive to investors, because coupons have increased and the debt’s interest rate risk is low. Floating-rate direct loans have historically performed well in rising-interest-rate environments.

-

LBO activity has declined significantly: Rising financing costs have caused sponsor-backed deals to decline in 2022. Competition for these deals remains fierce.

-

Europe’s economy is in a vulnerable position: The unemployment rate in the eurozone fell to 6.6% in May from 8.3% at year-end, but annual inflation surged from 5.1% in January to 9.6% in June, primarily because of the war in Ukraine.58 The region’s economic health is being negatively impacted by the conflict, the related surge in energy prices, and the prospect of tightening monetary policy. The slowdown in China’s economy also poses a risk to Europe, as China is Germany’s largest trading partner. Germany recorded its first trade deficit in over 30 years in June.59

Outlook

Opportunities

-

Non-sponsor-backed deals may offer more attractive opportunities than the crowded sponsor-backed market: Investing in the former often demands specialization, an extensive network, and robust sourcing capabilities.

-

Rising interest rates and slowing economic growth may make European banks less willing to lend: European borrowers outside the sponsor-backed market have traditionally had to rely on banks or informal sources of capital, but these borrowers may now turn to direct lenders as bank lending declines.

-

Fast-growing life sciences and software companies may access capital through direct lending markets: Public market valuations of life sciences companies have plummeted over the last 12 months, so companies may seek non-dilutive financing in private markets. We expect that significant lending opportunities in these industries will develop, driven by technological advancements and sizable research & development requirements.

Risks

-

Businesses’ fundamentals could decline: Shortages of labor and key inputs could impede economic growth and weigh on the earnings of companies that can’t pass rising costs onto customers.

-

Recession risk is increasing: If the U.S. economy contracts, private equity sponsors may not inject capital into struggling companies like they did in 2020–21. Sponsors may have already met their investment caps or believe they won’t earn a sufficient return.

-

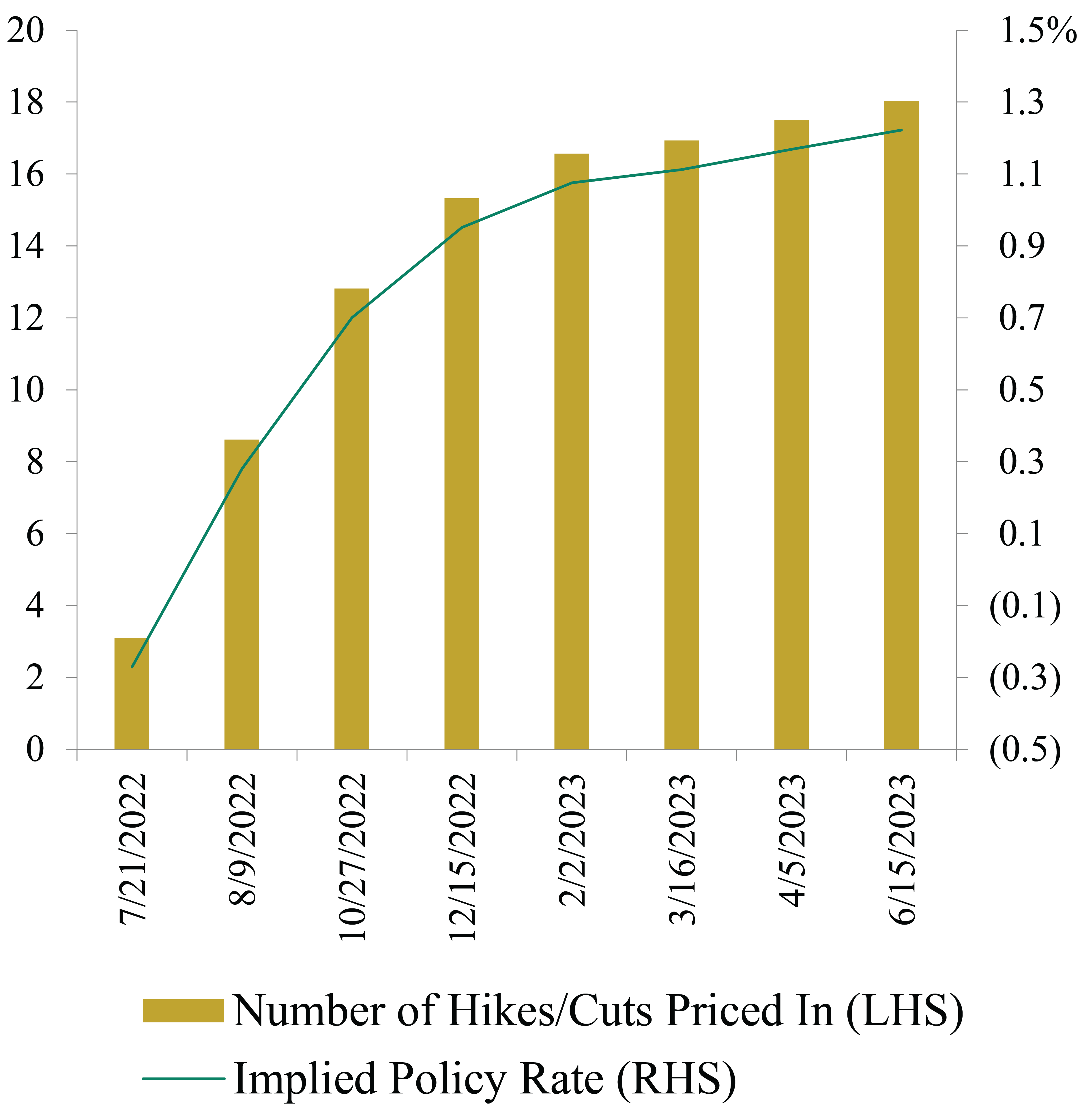

Tightening monetary policy could negatively impact the lending environment: The Fed has already begun to hike interest rates, and the ECB is now expected to increase interest rates multiple times in 2022. (See Figure 11.) Higher interest rates may discourage new borrowing and make it challenging for current borrowers to roll over their debt. This situation could make defaults more likely.

Source: Bloomberg

INVESTMENT GRADE CREDIT

Market Conditions: 2Q2022

Return: -6.7%60

Issuance: $282bn61

-

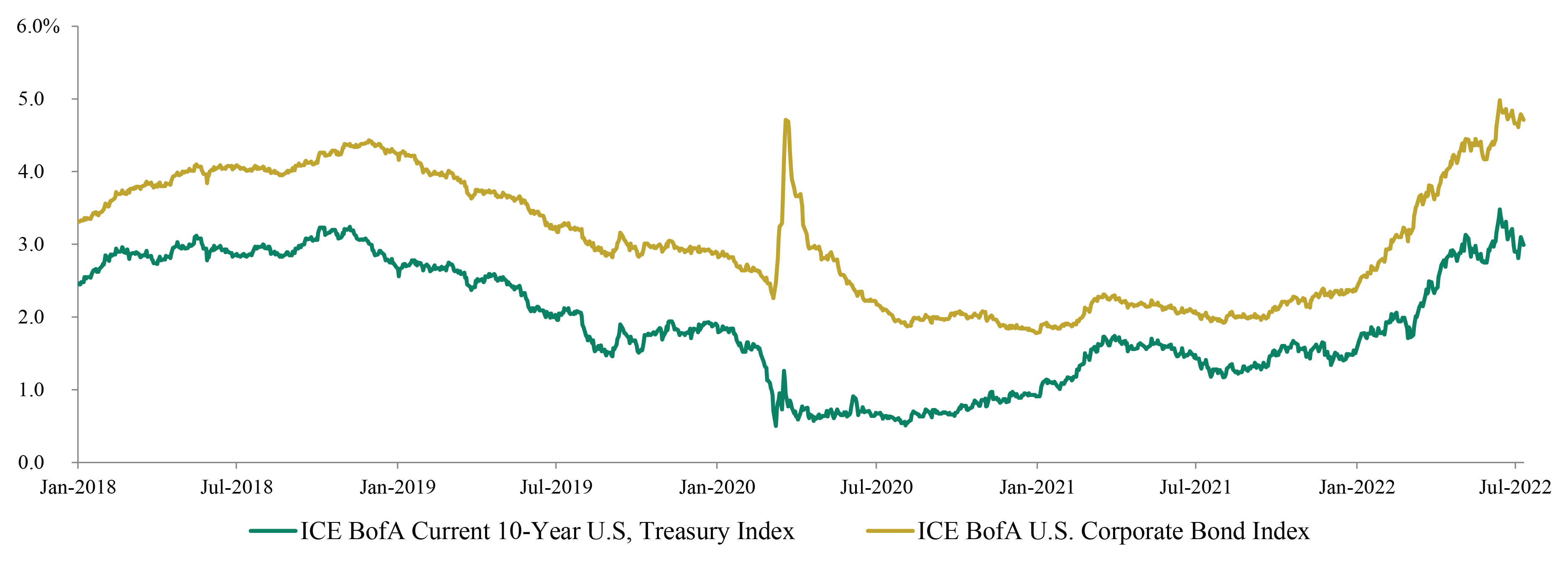

Tightening U.S. monetary policy was the primary driver of weakness in investment grade credit during 2Q2022: U.S. Treasury yields increased significantly during the quarter, as the Federal Reserve hiked interest rates to combat elevated inflation. The yield on the 10-year Treasury note rose by 66 bps during the period.62 Investment grade bonds outperformed their high yield counterparts, due to the significant yield spread widening in the latter market.

-

Investment grade bonds benefited from investors’ focus on recession risk near quarter-end: Treasury yields fell in the second half of June after the Federal Reserve raised the fed funds rate by 75 bps, and investor attention shifted to the threat of a recession. Investment grade bonds have benefited more from the recent decline in interest rates than their high yield counterparts.

-

Higher-quality credits have proven resilient: Yield spreads of A-rated credits have widened less significantly than those of lower-rated credits. A-rated bond offer an average price near 90 cents on the dollar and a yield-to-maturity of roughly 4.5%.63

Outlook

Opportunities

-

Yields on investment grade corporate debt have risen to attractive levels: The asset class’s yield rose by around 110 bps during the quarter to reach 4.7% as of June 30.64 (See Figure 12.)

-

Rising recession risk may benefit investment grade debt: High yield bonds are likely to underperform investment grade debt in the coming months if performance in credit is driven more by widening yield spreads than rising Treasury yields.

-

Defensive sectors could potentially offer attractive value if the macro backdrop deteriorates: Non-cyclical sectors such as financials typically outperform during economic downturns.

Risks

-

Inflation may remain elevated, putting pressure on the Fed to continue aggressively hiking interest rates: Tighter monetary policy and slowing economic activity should temper inflation, but endogenous factors (such as the lag in accounting for rental housing price increases) and exogenous factors (such as geopolitical risk) could put upward pressure on inflation.

-

Rising input costs and slowing economic growth could weigh on corporate earnings: Issuers’ fundamentals remain fairly robust, but margin compression could negatively impact credit metrics, generating credit ratings downgrades and mark-to-market weakness.

Figure 12: Yields on Investment Grade Bonds Have Spiked as U.S. Treasury Yields Have Risen

Source: ICE BofA

ABOUT OAKTREE’S PERFORMING CREDIT PLATFORM

Oaktree Capital Management is a leading global alternative investment management firm with expertise in credit strategies. Our Performing Credit platform encompasses a broad array of credit strategy groups that invest in public and private corporate credit instruments across the liquidity spectrum. The Performing Credit platform, headed by Armen Panossian, has $55.8 billion in AUM and approximately 190 investment professionals.65

ENDNOTES

1 U.S. Department of the Treasury.

2 The Federal Reserve.

3 U.S. Census Bureau.

4 U.S. Bureau of Labor Statistics.

5 U.S. Bureau of Labor Statistics.

6 Oxford Economics, as of June 22, 2022.

7 U.S. Bureau of Labor Statistics.

8 National Bureau of Statistics of China.

9 ICE BofA US High Yield Constrained Index.

10 ICE BofA US High Yield Constrained Index.

11 ICE BofA US High Yield Constrained Index, as of June 30, 2022.

12 JPM CLOIE BBB Index and JPM CLOIE BB Index.

13 Comparison calculated using FTSE High Yield Cash Pay Capped Index and JP Morgan CLOIE BB Index.

14 JP Morgan; Assuming 8% starting BB attachment point, 60% recovery, 15% CPR, 97% reinvestment price, and 1.5% benefit from diversion of interest to cure triggers.

15 The indices used in the graph are: Bloomberg Barclays Government/Credit Index, Credit Suisse Leveraged Loan Index, Credit Suisse Western European Leveraged Loan Index (EUR hedged), FTSE High Yield Cash Pay Capped Index, ICE BofA Global Non-Financial HY European Issuers ex-Russia Index (EUR Hedged), Refinitiv Global Focus Convertible Index (USD Hedged), JP Morgan CEMBI Broad Diversified Index (Local), JP Morgan Corporate Broad CEMBI Diversified High Yield Index (Local), S&P 500 Total Return Index, and FTSE All-World Total Return Index (Local).

16 Trailing-12-Month Default Rate.

17 FTSE High Yield Cash Pay Capped Index.

18 JP Morgan.

19 JP Morgan.

20 ICE BofA High Yield Master II Constrained Index.

21 FTSE High Yield Cash Pay Capped Index

22 ICE BofA Global Non-Financial High Yield European Issuer, Excluding Russia Index (EUR hedged).

23 S&P Global Leveraged Commentary & Data.

24 Credit Suisse.

25 ICE BofA US High Yield Index; ICE BofA Global Non-Financial High Yield European Issuer Excluding Russia Index.

26 FTSE High Yield Cash Pay Capped Index for the US, ICE BofA Global Non-Financial High Yield European Issuer Excluding Russia Index for Europe.

27 JP Morgan.

28 Credit Suisse Leveraged Loan Index.

29 JP Morgan; gross issuance includes refinancings and resets.

30 JP Morgan; Excludes distressed exchanges.

31 JP Morgan.

32 JP Morgan.

33 Credit Suisse Western Europe Leveraged Loan Index (EUR hedged).

34 S&P Global Leveraged Commentary & Data; gross issuance.

35 Credit Suisse.

36 Credit Suisse Western Europe Leveraged Loan Index (EUR hedged).

37 JP Morgan, as of July 14, 2022.

38 JP Morgan Corporate Broad CEMBI Diversified High Yield Index. The Emerging markets debt section focuses on dollar-denominated debt issued by companies in emerging market countries.

39 JP Morgan Corporate Broad CEMBI Diversified High Yield Index.

40 JP Morgan Corporate Broad CEMBI Diversified High Yield Index.

41 Morgan Stanley Research.

42 JP Morgan.

43 JP Morgan.

44 Refinitiv Global Focus Convertible Index.

45 Bank of America; gross issuance.

46 Bank of America.

47 Bank of America.

48 Refinitiv Global Focus Convertible Index; yield-to-maturity is currency hedged.

49 Refinitiv Global Focus Convertible Index.

50 JP Morgan CLOIE BBB Index.

51 JP Morgan CLOIE BB Index.

52 JP Morgan; new issue only, so doesn’t include refinancings and resets.

53 JP Morgan; new issue only, so doesn’t include refinancings and resets.

54 JP Morgan.

55 JP Morgan CLOIE BBB Index, JP Morgan CLOIE BB Index.

56 Barclays CMBS 2.0 BBB Index.

57 Barclays.

58 Eurostat, as of July 13, 2022.

59 Federal Statistical Office of Germany (Destatis).

60 ICE BofA US Corporate Index.

61 SIFMA.

62 U.S. Department of the Treasury.

63 ICE BofA US Corporate Index.

64 ICE BofA US Corporate Index.

65 The AUM figure is as of March 31, 2022 and excludes Oaktree’s proportionate amount of DoubleLine Capital AUM resulting from its 20% minority interest therein. The total number of professionals includes the portfolio managers and research analysts across Oaktree’s performing credit strategies.

NOTES AND DISCLAIMERS

This document and the information contained herein are for educational and informational purposes only and do not constitute, and should not be construed as, an offer to sell, or a solicitation of an offer to buy, any securities or related financial instruments. Responses to any inquiry that may involve the rendering of personalized investment advice or effecting or attempting to effect transactions in securities will not be made absent compliance with applicable laws or regulations (including broker dealer, investment adviser or applicable agent or representative registration requirements), or applicable exemptions or exclusions therefrom.

This document, including the information contained herein may not be copied, reproduced, republished, posted, transmitted, distributed, disseminated or disclosed, in whole or in part, to any other person in any way without the prior written consent of Oaktree Capital Management, L.P. (together with its affiliates, “Oaktree”). By accepting this document, you agree that you will comply with these restrictions and acknowledge that your compliance is a material inducement to Oaktree providing this document to you.

This document contains information and views as of the date indicated and such information and views are subject to change without notice. Oaktree has no duty or obligation to update the information contained herein. Further, Oaktree makes no representation, and it should not be assumed, that past investment performance is an indication of future results. Moreover, wherever there is the potential for profit there is also the possibility of loss.

Certain information contained herein concerning economic trends and performance is based on or derived from information provided by independent third-party sources. Oaktree believes that such information is accurate and that the sources from which it has been obtained are reliable; however, it cannot guarantee the accuracy of such information and has not independently verified the accuracy or completeness of such information or the assumptions on which such information is based. Moreover, independent third-party sources cited in these materials are not making any representations or warranties regarding any information attributed to them and shall have no liability in connection with the use of such information in these materials.

© 2022 Oaktree Capital Management, L.P.

Informações sensíveis e divulgação

Este memorando expressa as opiniões do autor na data indicada e tais opiniões estão sujeitas a alterações sem aviso prévio. A Oaktree não tem a obrigação de atualizar as informações aqui contidas. Além disso, a Oaktree não faz nenhuma representação, e não se deve assumir que odesempenho dos investimentos passados é uma indicação de resultados futuros. Além disso, onde quer que haja potencial de lucro, também existe a possibilidade de prejuízo. Este memorando está sendo disponibilizado apenas para fins educacionais e não deve ser usado para qualquer outro propósito. As informações contidas neste documento não constituem e não devem ser interpretadas como uma oferta de serviços de consultoria ou uma oferta de venda ou solicitação de compra de quaisquer títulos ou instrumentos financeiros relacionados, em qualquer jurisdição. Certas informações contidas neste documento sobre tendências econômicas e desempenho são baseadas ou derivadas de informações fornecidas por fontes terceirizadas independentes. A Oaktree Capital Management, L.P. (“Oaktree”) acredita que as fontes das quais tais informações foram obtidas são confiáveis; no entanto, não pode garantir a exatidão de tais informações e não verificou de forma independente a exatidão ou integridade de tais informações ou as suposições nas quais tais informações se baseiam. Este memorando, incluindo as informações aqui contidas, não pode ser copiado, reproduzido, republicado ou postado na íntegra ou parcialmente, em qualquer formato, sem o consentimento prévio, por escrito, da Oaktree.