Link para o artigo original : https://www.bridgewater.com/research-and-insights/how-conditions-today-compare-to-past-equity-market-bottoms

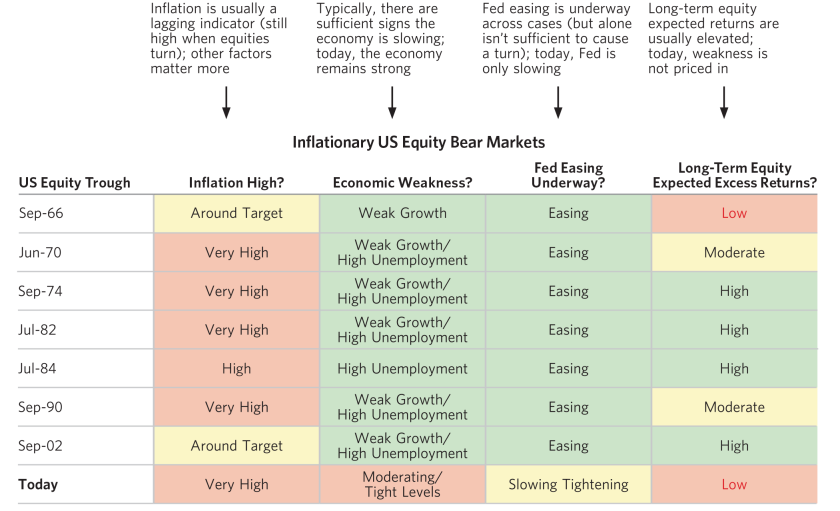

Many of the key markers of an inflation-driven bear market bottom are still missing today— little real economic weakening, few signs the central bank is ready to move to easing, and, as of yet, not much repricing of equities beyond the direct drag from rising interest rates.

Global equity markets are down more than 17% this year as central banks responded to strong inflation with a record pace of tightening. Have stocks fallen enough to see the bottom in the market, or is more pain ahead? One perspective we have found helpful when considering this question is comparing conditions today to past inflation-driven equity market bottoms.

Bear markets typically unfold in a sequence: 1) rising interest rates push down equity prices, as any future cash flow is discounted to the present at a higher yield; 2) higher rates and growing economic uncertainty draw money out of risky assets, depressing equity prices further as risk premiums rise; and 3) the combination of the impact of rising discount rates, risk premiums, and declining asset prices leads to declining economic activity and earnings, creating more downward pressure on equities.

The equity bottom typically does not come until 1) there is a meaningful period of easing sufficient to offset the negative economic momentum, and 2) equity prices fall enough that investors are incentivized to move back out the risk curve and buy stocks. The former typically means that central banks assess that the slowdown in economic activity has been large enough to bring inflation back under control. And the latter means equities typically decline much more than justified by higher interest rates, resulting in valuations that are low enough to draw investors back in.

When we look at conditions today, the typical markers of an equity market bottom are not yet present. Inflation remains very high, and the economy remains relatively strong, such that a Fed easing does not seem likely (currently the Fed has only indicated that it will slow its tightening). And despite the drop in equity prices, long-term equity expected returns still look poor compared to bonds and cash—meaning investors still lack a strong incentive to jump back in. The Fed will likely need to see more weakness—and investors, lower prices—before equities find a floor and begin a sustainable climb.

The table below synthesizes economic conditions and equity pricing around inflation-driven bear market troughs in the US (i.e., cases where concerns around high inflation drove Fed tightening that led to the equity sell-off). Inflation is typically a lagging indicator; equities rallies have typically begun when inflation is still high. Instead, rallies begin when central banks see meaningful economic weakness and shift into gear to ease to stop the downturn and when equity markets have gone through a meaningful repricing.

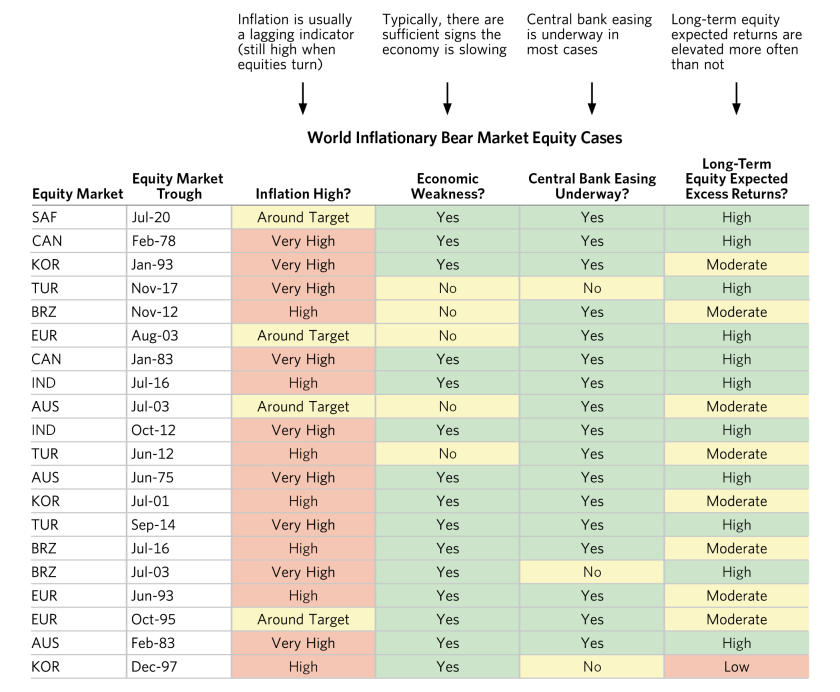

Historical cases are also illustrative of where we could be wrong. The main cases that did not see another leg down in the market were a) when inflation proved entirely driven by transitory factors and the central bank did not need to drive slowing to get inflation below target (as in 2018), and b) when the central bank decided to let inflation run much hotter (in the late ’60s as well as in emerging market cases like Turkey; we include a table synthesizing inflationary bear markets in markets outside of the US at the end of this report). We are watching for signs that we might be in either of these cases. As of now, the risk of this outcome still looks relatively low to us.

In the rest of this report, we discuss in more detail the drivers we described above of inflation-driven bear market bottoms through time. As noted, we exclude bear markets where high inflation was not a key driver, such as 1987 and 2009, and given how comparatively limited inflation concerns were in 2018, we also exclude that period. In each chart, the three months prior to the trough in equity markets is highlighted in red.

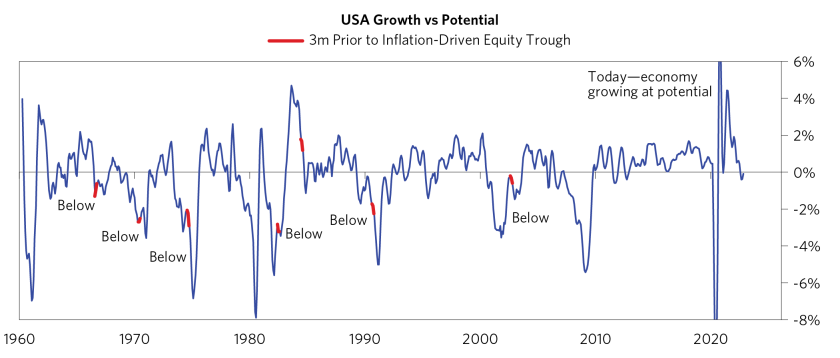

A Meaningful Period of Weak Growth Is a Common Feature of Equity Bottoms, but Growth Today Still Looks Roughly Normal

Growth is typically below potential going into inflation-driven equity market troughs, as the Fed usually needs to see weak conditions to ease and turn the market. The main exception was 1984—the economy was growing modestly above potential but turning down fast, as shown in the chart below, and as we show on the next chart, unemployment was relatively high. Today, we’re coming off a period of very strong growth and now the economy has moderated but is still expanding at around potential.

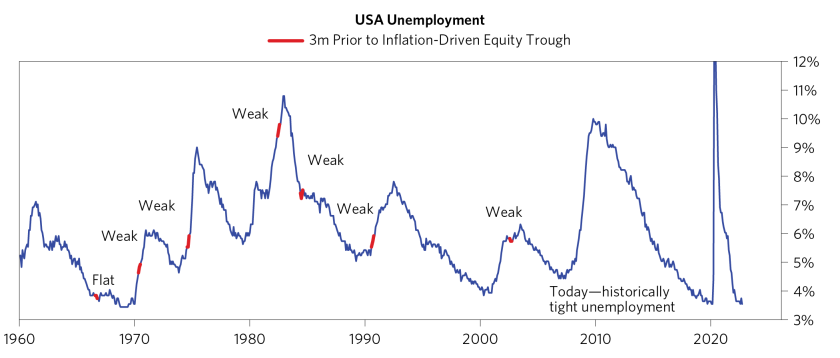

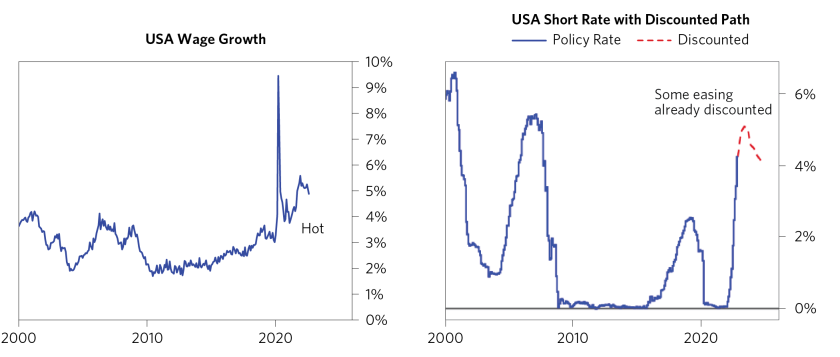

Similarly, employment is also typically weak going into inflation-driven bear market bottoms. High unemployment is both an indicator and a cause of falling growth and inflation, incentivizing the Fed to step in and support the economy while also helping create the low-inflation conditions that would allow the central bank to do so. Today, unemployment is around all-time lows and tight labor markets are a major driver of high wage growth and resilient above-target inflation.

Equity Market Bottoms Typically Don’t Emerge Until the Implications of the Tightening Have Been Discounted; That Hasn’t Happened Yet

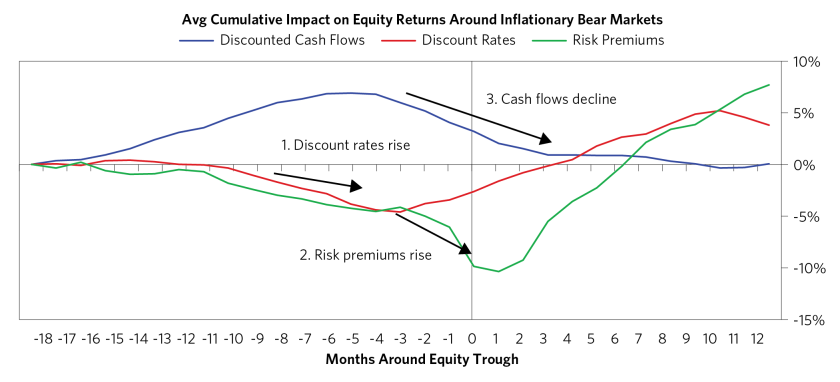

As discussed above, equity bear markets (and their troughs) typically occur in sequence. First, interest rates go up, dragging down equity prices via the discount rate effect on future cash flows. Higher rates and growing economic uncertainty, in turn, begin to pull money out of risky assets, pushing down equity prices further as risk premiums rise. Last, the combination of the impact of rising discount rates, risk premiums, and declining asset prices leads to declining economic activity and earnings, creating more downward pressure on equities. Troughs occur when there has been a material re-rating in equity pricing such that weakness in the economy is expected and risk premiums are high, setting up conditions for a bounce once the central bank eases enough to offset the downturn.

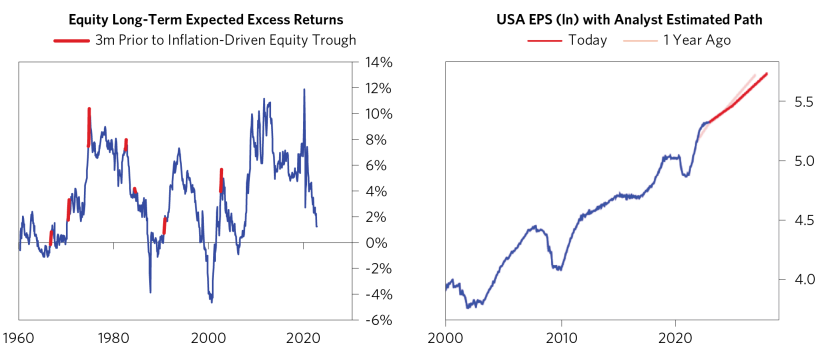

The chart below shows the average of the three components of equity returns around equity troughs—discount rates, risk premiums, and cash flow expectations. Typically, falling discount rates are already a support, while falling cash flow expectations and expanding risk premiums are a meaningful drag in the months prior to the bottom in equity markets.

As noted above, there is typically a meaningful increase in equity expected returns (shown below in excess of cash) before the turn in the market because investors need to be incentivized back into equities and out of safe assets following significant losses.

Today, based on our read, the re-rating of equity prices has a way to go. Our estimate for long-term excess expected returns remains relatively low compared to history. Consistent with that, analyst consensus for long-term corporate cash flow growth has barely budged over the last year, not yet reflecting the cooling of the economy we expect to see.

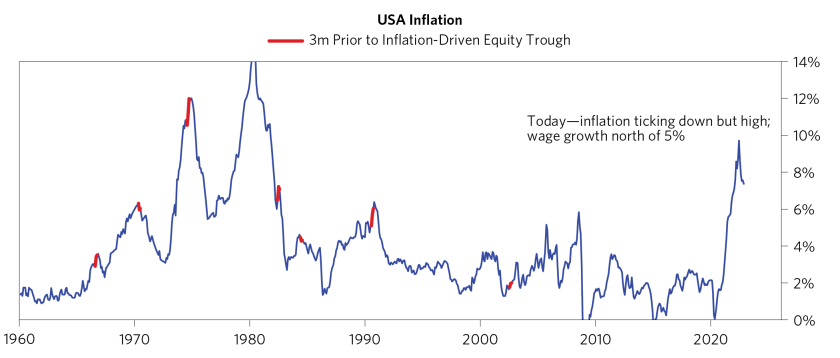

Equity Bottoms Are Typically Accompanied by Inflation Turning Over; Today, Inflation Has Moderated, but Under the Hood, Wage Growth Has Picked Up the Baton

While inflation is still high, it has come down from its peak over the past few months. In a number of the inflationary historical bear market cases, equities turned up just as inflation turned down from highs and discount rates fell. Across the historical cases, however, the turn in inflation was accompanied by meaningful economic weakness that required the Fed to choose between inflation and economic pain. And as discussed, this weaker growth and high unemployment was itself an ongoing downward pressure on inflation.

Today, moderating inflation is not accompanied by weaker growth and inflation seems unlikely to hit central bank targets any time soon. As some of the commodity surges and acute supply chain challenges roll off, wage growth (running north of 5%) is picking up the baton and fueling the next leg of inflation. As a result, the Fed is not yet being forced to choose between weak growth and high inflation and is still able to concentrate primarily on its inflation mandate. It’s also worth noting that the Fed is already discounted to slow its pace of tightening, so any support to equities will need to come from the Fed easing more than what is already discounted.

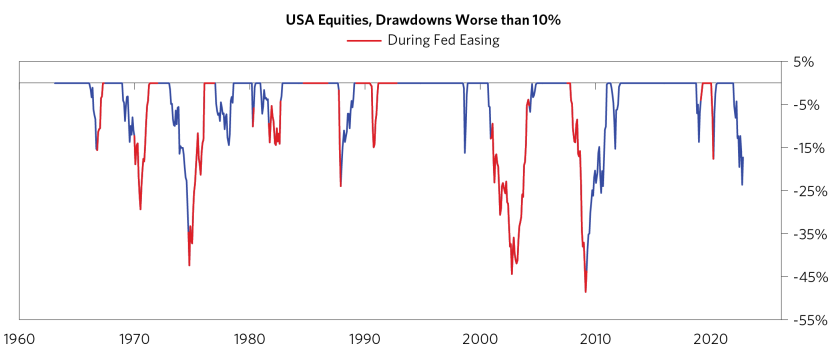

Equity Bottoms Are Typically Accompanied by a Significant Period of Easing; Today, the Fed Has Yet to Pause

Today, the Fed has stated that it might consider slowing its future pace of tightening. Typically, it takes much more than this to bring about the bottom in the equity market. It takes a long enough period and significant enough amount of easing to really offset economic weakness and bring about an upturn. The chart below shows this point. Note the format is a bit different from those shown above. We show equity market drawdowns, but this time the line in red illustrates the period when the Fed was actively easing. This highlights that the most significant drawdowns in US history have occurred after the Fed shifts to lowering rates.

While we mainly focus on the US in this report, a similar pattern holds true in inflationary equity bear markets across other developed economies and emerging markets. There is a collection of cases where EM central banks eased fast enough and hard enough to offset a cash flow decline prior to any real weakening in employment (Turkey throughout the 2000s and Brazil in 2012). In these cases, ultimately, the central bank was really letting inflation go. Note this analysis excludes hyperinflation cases.

This research paper is prepared by and is the property of Bridgewater Associates, LP and is circulated for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives or tolerances of any of the recipients. Additionally, Bridgewater’s actual investment positions may, and often will, vary from its conclusions discussed herein based on any number of factors, such as client investment restrictions, portfolio rebalancing and transactions costs, among others. Recipients should consult their own advisors, including tax advisors, before making any investment decision. This report is not an offer to sell or the solicitation of an offer to buy the securities or other instruments mentioned.

Bridgewater research utilizes data and information from public, private, and internal sources, including data from actual Bridgewater trades. Sources include BCA, Bloomberg Finance L.P., Bond Radar, Candeal, Calderwood, CBRE, Inc., CEIC Data Company Ltd., Clarus Financial Technology, Conference Board of Canada, Consensus Economics Inc., Corelogic, Inc., Cornerstone Macro, Dealogic, DTCC Data Repository, Ecoanalitica, Empirical Research Partners, Entis (Axioma Qontigo), EPFR Global, ESG Book, Eurasia Group, Evercore ISI, Factset Research Systems, The Financial Times Limited, FINRA, GaveKal Research Ltd., Global Financial Data, Inc., Harvard Business Review, Haver Analytics, Inc., Institutional Shareholder Services (ISS), The Investment Funds Institute of Canada, ICE Data, ICE Derived Data (UK), Investment Company Institute, International Institute of Finance, JP Morgan, JSTA Advisors, MarketAxess, Medley Global Advisors, Metals Focus Ltd, Moody’s ESG Solutions, MSCI, Inc., National Bureau of Economic Research, Organisation for Economic Cooperation and Development, Pensions & Investments Research Center, Refinitiv, Rhodium Group, RP Data, Rubinson Research, Rystad Energy, S&P Global Market Intelligence, Sentix Gmbh, Shanghai Wind Information, Sustainalytics, Swaps Monitor, Totem Macro, Tradeweb, United Nations, US Department of Commerce, Verisk Maplecroft, Visible Alpha, Wells Bay, Wind Financial Information LLC, Wood Mackenzie Limited, World Bureau of Metal Statistics, World Economic Forum, YieldBook. While we consider information from external sources to be reliable, we do not assume responsibility for its accuracy.

The views expressed herein are solely those of Bridgewater as of the date of this report and are subject to change without notice. Bridgewater may have a significant financial interest in one or more of the positions and/or securities or derivatives discussed. Those responsible for preparing this report receive compensation based upon various factors, including, among other things, the quality of their work and firm revenues.