Link para o artigo original : http://ow.ly/ibUE50H5YGw

Climate Investment:

Positioning Portfolios for a Warmer World

By Steven Desmyter, Otto van Hemert, Ashok Kumar Muthusamy, Matt Goldklang, Edward Cole and Alex Preston

Awards and/or ratings are for information purposes only and should not be construed as an endorsement of any Man Group company nor of their products or services. Please refer to the websites of the sponsors/issuers for information regarding the criteria on which the awards/ratings are determined.

Contents

Introduction

Part 1: The Science of Climate Change

1. Climate Models

2. AR6

3. The Paris Agreement

4. Corporations, Regulation and Climate

Part 2: Investing in a Warming World

1. Physical Cost

2. Transition Costs

3. Stranded Asset Costs

4. Opportunity

5. Portfolio Management in a Warming World

Part 3: Sustainable Investing and ESG

1. The Rise of Sustainable Investing

2. ESG Ratings Firms and Frameworks

3. From ESG to Climate+

4. Environmental Regulation in the Investment Industry

5. Stewardship and Activism

6. What Securities are ‘Good’ for the Environment?

Authors

Bibliography

Introduction

Let us skip the pleasantries. This is not a document in which we will seek to justify action on climate – the evidence is clear, the need unquestionable. Nor is this intended as a marketing document, indicating how seriously we all take the issue – we have all read enough of that kind of self-serving material. Rather, this White Paper seeks to do something that we haven’t seen done elsewhere: to give a comprehensive and realistic overview of how the climate crisis has impacted financial markets, how the markets have responded, and the role that we believe the financial services industry has to play in the move to a carbon-neutral future. Throughout this document, we will prioritise facts and data over conjecture and opinion, seeking to do several very difficult things: to look with some degree of perspective at the present moment; to steer past the fluff and bluster to establish an unalloyed picture of what has been achieved and what is yet to be achieved; and to forecast both future developments and potential challenges for the industry as we move towards 2050 (and beyond).

We begin the paper with a comprehensive survey of the world of climate science. To understand the challenges and opportunities ahead, it’s necessary to grasp the terminology and methodology that climate scientists use to model potential temperature rise scenarios. In the opening chapters we will provide an in-depth guide to climate modelling and the various paths to net zero that are currently envisaged. We will outline the terms of the Paris Agreement, look at which countries have made which pledges regarding carbon reduction and how these are factored into the broader climate models. We will look in particular at the recently-released IPCC 6th Assessment Report (AR6) and its implications for the manner in which global heating is addressed.

The second section offers the reader an alternative slant on climate investment. Here we consider how climate will impact corporations and how investors might position their portfolios for a warming planet.(1) We look at how physical costs, transition costs and stranded assets will impact company balance sheets and P&Ls. We take the reader through an example of an energy firm seeking to realign its business model with carbon neutrality and suggest ways in which investors can pick between the winners and losers in this great generational transition. Even if the world hits its 2050 goals, there will still be some measure of global heating in the coming years and this will have significant implications for companies and markets. Less Developed Economies will suffer more, while there will be opportunities for those in more temperate and polar zones. Climate change will re-draw the global economic map and investors need to prepare their portfolios for this shift.

The final section of the paper focuses on the rapidlyexpanding world of climate-focused investment. Here we chart the rise of sustainable investment, ESG and green bonds. We seek to provide investors with a model for thinking about investing with a climate-focused mandate – given the varying metrics by which firm performance can be judged as far as sustainability goes and the wide dispersion between climate ratings from different data providers, how does one establish with any certainty whether an investment is genuinely climate-positive? Is ESG an accurate and useful proxy for climate investment? Where are the disjunctures between the ‘E’ in ESG and Climate Positive investing. We will look at European SFDR directives and how these are applied to funds. We then turn to the question of stewardship, attempting to outline a model for best practice when it comes to shareholder voting and engaging with company management on climate. We end this section with an attempt to outline our best estimates of the evolution of climate-focused investment across a variety of different asset classes.

This is a document that is about time and change, about how humans negotiate horizons and how, in extremis, scientific ingenuity and political will have been harnessed to address a crisis of unimaginable seriousness. It is perhaps too soon to say that we as a financial services industry can be proud of our contribution to the climate fight, but significant steps have been taken already and it feels like there is strong investor will to follow through on the promises made so far. We hope that you enjoy this, the third of our Client White Papers, and look forward to discussing it with you now and in a cleaner, greener future.

Part 1

The Science of Climate Change

What are climate models and how are they used to measure anthropogenic climate change?

What are Greenhouse Gases (GHGs) and how do they cause global heating?

How do scientists construct climate scenarios and how do they help us to ascertain the likely path of global temperatures?

What is the Paris Agreement and what will it mean for businesses?

Chapter 1 Climate Models

Key Points

-

-

-

-

-

What is the difference between climate and weather?

-

What is the Earth System and how do Climate Systems interact with it?

-

-

-

-

1.1 Introduction

The accuracy and sophistication of climate modelling is much like any other kind of modelling – it relies on credible and dependable data and it needs powerful computers to run multiple scenarios in order to establish the likeliest future paths for our climate. One of the things that has helped overcome climate change scepticism in recent years is the increasing reliability of climate models, not only in their ability to forecast the dire ramifications if action isn’t taken on carbon and other emissions, but also in the way they are able to show with great clarity the role that humans have played in global heating. In this chapter we will look at how climate models are constructed, how they are then used by climate scientists to establish potential scenarios for future temperature rises and what mitigating impact efforts to reduce emissions are likely to have.

Let us begin with the basics. A direct line can be drawn from weather forecasts to climate models. Weather forecasters use data and weather models to establish likely atmospheric conditions. The forecast takes into account humidity, temperature, air pressure, wind speed and direction, as well as cloud cover and other natural and man-made elements that could impact the hour-by-hour weather. These forecasts look out over a period of 10 days to two weeks and ascertain with both reasonable certainty and geographic specificity the likely pattern of weather in any one location. These individual localised forecasts are then combined to give a picture of the likely weather in a region and country.

Climate models essentially employ a similar process to weather models, although whereas weather looks for short-term patterns with a high degree of granularity, climate models analyse broader data over much longer time periods to establish average conditions over decades and centuries. Climate models also include processes that may not influence short term fluctuations in weather but are contributing to longer term climate change. These include ocean currents and melting glaciers, as well as the impact of human activity. Climate models take many thousands, even hundreds of thousands, of data points and run them through sophisticated iterations to simulate the impact on complex earth systems.

What is the Earth System?

The term ‘Earth system’ refers to Earth´s interacting physical, chemical, and biological processes.

The system consists of the land, oceans, atmosphere and poles. It includes the planet’s natural cycles — the carbon, water, nitrogen, phosphorus, sulphur and other cycles — and deep Earth processes.

Life too is an integral part of the Earth system. Life – human and other – affects the carbon, nitrogen, water, oxygen and many other cycles and processes.

The Earth system includes human society – our social and economic systems are now embedded within the Earth system. In many cases, human systems are now the main drivers of change in the Earth system.

1.2 The Science of Global Heating

-

What is Global Heating and how do Greenhouse Gasses (GHGs) cause it?

-

What are the major GHGs?

- What are dadiative forcings and how do they play into the construction of climate models?

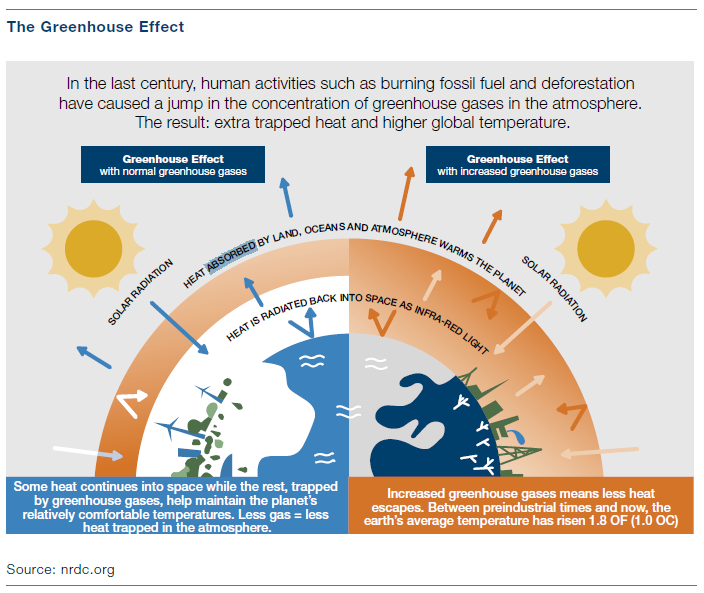

Global heating is the long-term heating of Earth’s climate system observed since the pre-industrial period (before 1850) due to human activity, primarily the burning of fossil fuels, which increases heat-trapping greenhouse gas levels in Earth’s atmosphere. Global heating (or warming) is frequently used interchangeably with the term climate change, though the latter refers to both human- and naturally produced warming and the impact it has on our planet. It is most commonly measured as the average increase in Earth’s global surface temperature.

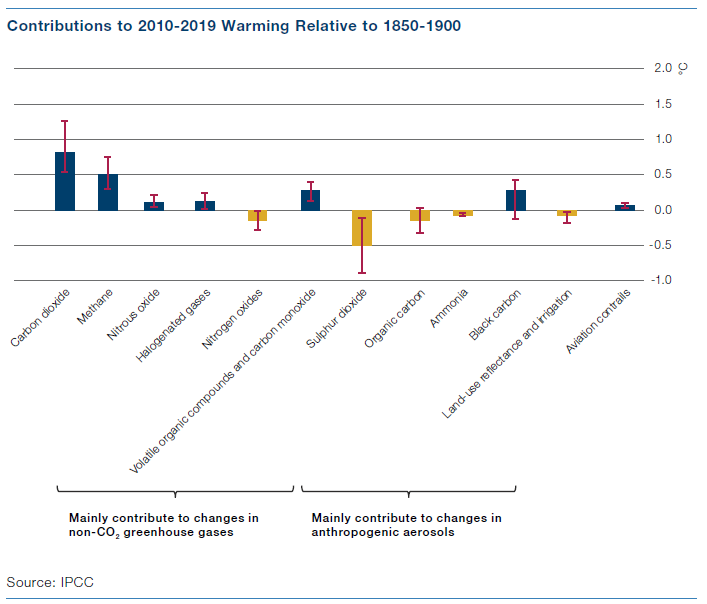

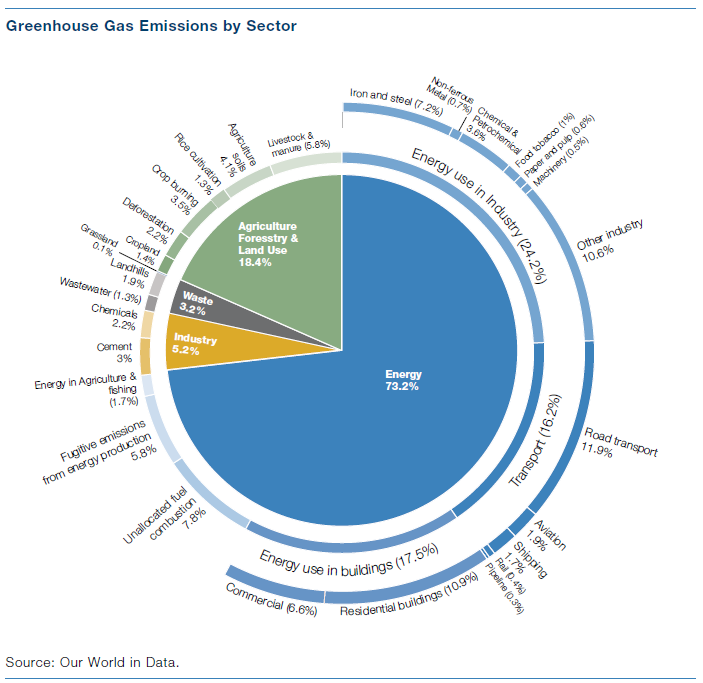

Earth’s greenhouse gases trap heat in the atmosphere and consequently increase global temperatures. The main greenhouse gases emitted by human activity are carbon dioxide (CO2), methane (CH4), and nitrous oxide (N20). Annual emissions of these three substances have respectively risen, as measured in billions of tons, from 14.8, 5.3, and 2.2 in 1970 to 36.1, 8.0, and 3.2 by 2014. CO2 is the least potent but nonetheless the most important greenhouse gas. It is released in massive and rising volume from the burning of fossil fuels (petrol, natural gas, coal) and land use (deforestation, slash-and-burn agriculture). More potent, but released in overall volume that is less impactful, is CH4, which is a by-product of livestock digestion, fossil fuel extraction, and the decay of agricultural waste. This is followed by N20, which is released by industrial activity and industrial agriculture. Methane is more potent immediately after it is released, but it decays faster (over one or two decades) than carbon dioxide (which takes around a century).

There are other harmful gases that contribute to global heating, including Fluorinated gases (F-gases) including hydrofluorocarbons, perfluorocarbons, sulphur hexafluoride and nitrogen trifluoride. These are powerful synthetic greenhouse gases that are emitted from a variety of industrial processes.

Greenhouse gases have different chemical properties and are removed from the atmosphere, over time, by different processes. Carbon dioxide, for example, is absorbed by so-called carbon sinks such as plants, soil, and the ocean. Fluorinated gases are destroyed only by sunlight in the far upper atmosphere.

How much any one greenhouse gas influences global warming depends on three key factors. The first is how much of it exists in the atmosphere. Concentrations are measured in parts per million (ppm), parts per billion (ppb), or parts per trillion (ppt); 1 ppm for a given gas means, for example, that there is one molecule of that gas in every 1 million molecules of air. The second is its lifetime—how long it remains in the atmosphere. The third is how effective it is at trapping heat. This is referred to as its global warming potential, or GWP, and is a measure of the total energy that a gas absorbs over a given period of time (usually 100 years) relative to the emissions of 1 tonne of carbon dioxide.

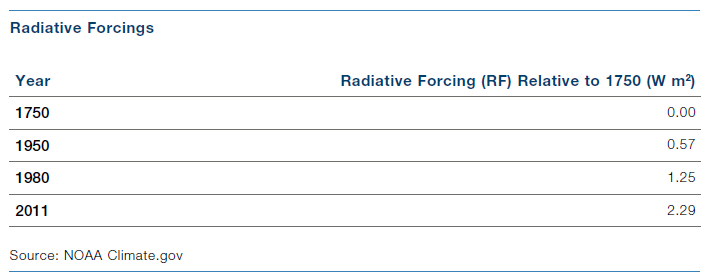

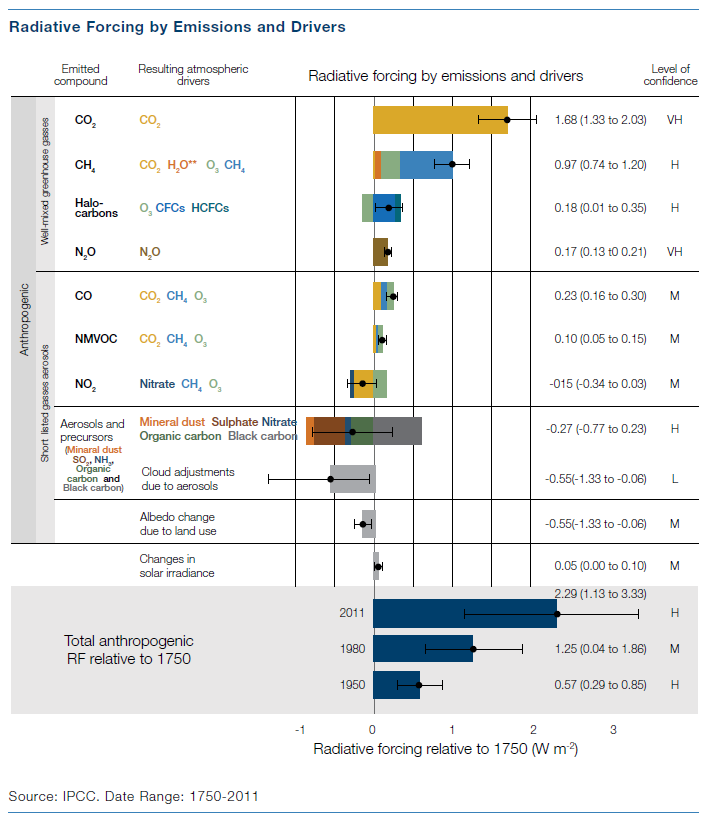

To establish patterns of climate change, scientists look at what is known as radiative forcing. There are natural forcings – changes in the sun’s energy output, the Earth’s orbital cycle, volcanic eruptions – and, increasingly, there are humancaused or anthropogenic forcings – the release of gasses that increase the amount of energy within the Earth system. Each greenhouse gas has its own radiative forcing and the combination of these forcings is largely responsible for global heating. Since the Industrial Revolution, radiative forcing has increased dramatically, a reflection of the impact of anthropogenic activity.

The table below shows the impact of different forcings on overall climate and the level of confidence with which each of these impacts can be stated.

1.3 Building Climate Models

-

How to understand the findings of climate models.

-

Why do climate models take so long to run?

- The grid-based design of climate models.

- Different types of climate model.

It should be pointed out here that climate models are not a precise science; they do not show facts but rather indicate potential directions for climate. The further into the future they look, the less certain they are. This uncertainty sits behind many of the misapprehensions and issues surrounding climate models. If we understand them properly it is as indicators of change and potential paths of travel, which, in combination with other forecasting models and research, will give a range of possible outcomes for global temperatures and other climatological changes.

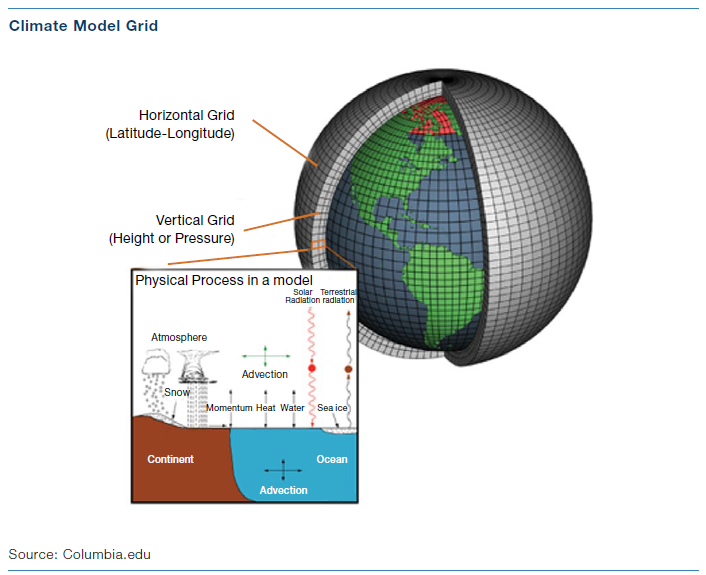

When building models climate scientists draw on a number of objective physical principles that underpin the Earth system regarding the transfer of energy and matter. These include Newton’s First Law of Thermodynamics, which says that energy cannot be created or destroyed, but only changed from one form to another; the Stefan-Boltzmann Law, which shows that the natural greenhouse effect maintains global temperatures 33C higher than they would otherwise be; and the Navier-Stokes equations of fluid motion, which characterise the speed, pressure, temperature and density of gases in the atmosphere and the water in the ocean.

These physical equations are converted into code in computer models, generally written in the somewhat archaic programming code Fortran. A single climate model can fill 18,000 pages of printed text. There are more than 40 global climate models currently in operation and they work by separating the Earth’s surface into a 2- or 3-dimensional grid of cells, usually between 600km and 100km in longitude and latitude (although, due to the curvature of the Earth, these will be smaller at the poles and larger at the equator). These grids are layered both horizontally and vertically across the surface of the Earth, down to the depths of the oceans and into the atmosphere.

The model then calculates the state of the climate in each cell, establishing disparate elements such as pressure, temperature, humidity and wind speed. For processes that happen on scales that are too small to be captured by the grids (such as convection) the model uses ‘parameterisations’ to fill in these gaps.(2) These are essentially approximations that simplify each process and allow them to be included in the model. More recently, scientists have experimented with using different shapes for these grids, including cubed spheres and icosahedral grids. As a general rule, increasing the spatial resolution of a model by a factor of two will require around ten times the computing power to run the model in the same amount of time.

Every model is a series of compromises between accuracy and the amount of computer power/time required to run the model. The size of each individual grid is only one element that can be altered to provide a more accurate/swifter result. Once the grids have been laid out, the next stage is to calibrate the frequency with which the model calculates the state of the climate system – this is known as the ‘time step’ process. Depending on the aims of the climate model, each time step can be set at minutes, hours, days or even years. Smaller time steps give more accurate results, but at the expense of requiring greater computer power.

Once climate models are constructed, they are hindcasted, running the model backwards against recorded data to test for accuracy. Scientists are then able to adjust the models based on how closely they mirror observed data. Once a model performs well in hindcasting, its results are assumed to be valid, and it is then used to create simulations of future climate scenarios.(3)

1.4 Climate Scenarios

-

How do scientists and policymakers use climate models to inform climate scenarios?

-

How should we seek to understand climate scenarios and pathways?

- How do climate scenarios drive carbon budgets?

Forecasting climate is a science, but it’s also an art. Any climate model is only as good as the scenarios it works with – these scenarios can be thought of as narratives around the future path of human development. This means that scientists need to estimate the growth of populations, the way land is used, the evolution of economies and, crucially, the extent to which technology will help humans to mitigate the impact of detrimental gas release.

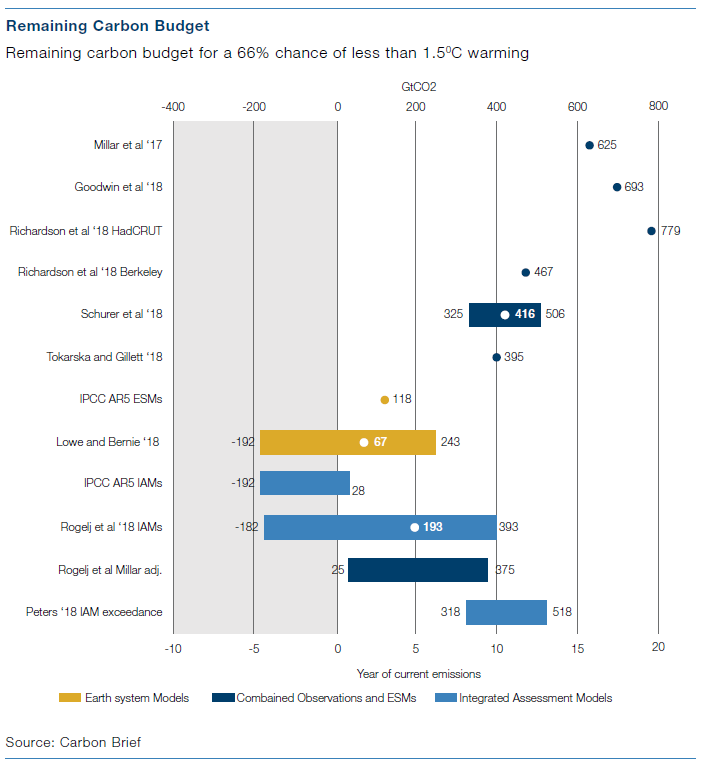

In 2000, the Intergovernmental Panel on Climate Change (IPCC) issued its Special Report on Emissions Scenarios (SRES), constructing four scenario families to describe a range of possible future conditions. Referred to by letter-number combinations such as A1, A2, B1, and B2, each scenario was based on a complex relationship between the socioeconomic forces driving greenhouse gas and aerosol(4) emissions and the levels to which those emissions would climb during the 21st century. Climate scientists used this data to produce estimates of how much CO2 the world can continue to emit and still keep global average temperature rise to no more than 1.5°C, 2°C or 3°C above pre-industrial levels. These are known as carbon budgets.

For each temperature limit the IPCC produced three specific budgets, each corresponding to a different probability of staying below that limit: 66%, 50% and 33%. The chart below, from Carbon Brief, shows how many years are left of current emissions before we breach the 66% budget of a 1.5°C rise, according to a variety of different models.

In a 2017 paper in the journal Nature Geoscience entitled ‘Emission budgets and pathways consistent with limiting warming to 1.5 °C’, the University of Exeter’s Richard Millar and a group of fellow academics attempted to establish as definitively as possible the remaining global carbon budget that would keep temperatures below the 1.5°C level. The findings of the study were highly controversial, in that they suggested a much greater budget than had previously been considered, with around 15 years of current usage left (this was 5x higher than previous IPCC estimates). While many took issue with Millar’s findings at the time, subsequent studies have largely supported the view that we may have more carbon budget than has been suggested by IPCC models. However, even taking into account Millar’s more optimistic estimates, there is still a vanishingly small window in which we have an opportunity to limit the damage of climate change.

There were subsequent updates to the IPCC SRES, each being named an Assessment Report and concentrating on a different subset of the factors driving climate change. The most recent of these, AR6, was released in 2021. Alongside AR6, we also saw the latest iteration of the Coupled Model Intercomparison Project (CMIP), a multinational effort to improve the accuracy of climate models by comparing outputs from multiple different models.

Different types of Climate Model

Most climate models can be separated into four distinct types: energy balance models, intermediate complexity models, and general circulation models.

Energy balance models are the simplest and oldest form of climate model. They forecast climate changes using Earth’s energy budget. Forecasters look at elements including surface temperatures from solar energy, the albedo effect (reflectivity), and natural cooling as the Earth emits heat back out into space. Essentially, scientists calculate the difference between the amount of energy coming into the atmosphere and the amount going out. This establishes changes in heat storage. These models are essentially one-dimensional (or even zero-dimensional, meaning that they treat the Earth as a homogenous whole).

Radiative Convective Models simulate the transfer of energy through the height of the atmosphere – for example, by convection as warm air rises. Radiative Convective Models can calculate the temperature and humidity of different layers of the atmosphere.

Intermediate complexity models are similar to energy balance and radiative convective models, but they include Earth’s geographical structures in their calculations: land, oceans, and ice features. These geographical features allow intermediate complexity models to simulate large-scale climate scenarios such as glacial fluctuations, ocean current shifts, and atmospheric composition changes over long timescales. Intermediate complexity models describe the climate with less spatial and time-specific detail, so they are best used for large-scale and lowfrequency variations in the earth’s climate system.

General circulation models are the most complex and precise models for understanding climate systems. These models essentially combine the two previous models to take into account information regarding the atmospheric chemistry, land type, carbon cycle, ocean circulation and glacial makeup of the isolated area. These models tend to use smaller grids in order to give more accurate forecasts. Because of this, and the greater complexity of the data processing required, general circulation models can take several days to several weeks to run.

Chapter 2 AR6

Key Points

-

-

-

-

-

Assessment Report 6 is the IPCC´s most recent update, indicating how far the world still has to go to control global heating.

-

The tone and substance of the report marked a significant change from previous reports, being both more certain and more severe in the degree to which humans are implicated in global heating and the need to take urgent action to redress it.

-

Shared Socioeconomic Pathways (SSPs) seek to give a narrative to climate pathways, showing how we reach outcomes, both positive and negative.

-

-

-

-

August 2021 saw the release of the IPCC’s Assessment Report 6, with significant press and public attention generated around the key findings of the report. The Secretary-General of the UN, António Guterres, called the report a ‘code red for humanity.’ AR6 saw a distinct change in both tone and substance of the IPCC’s communications. The headline was clear – there is no longer room for doubt about humanity’s role in global heating and time is running out for meaningful action to be taken. In the words of the report, ‘It is unequivocal that human influence has warmed the atmosphere, ocean and land. Widespread and rapid changes in the atmosphere, ocean, cryosphere and biosphere have occurred… Global surface temperature will continue to increase until at least the mid-century under all emissions scenarios considered. Global warming of 1.5°C and 2°C will be exceeded during the 21st century unless deep reductions in CO2 and other greenhouse gas emissions occur in the coming decades.’

Other key takeaways are:

-

A greater understanding of the regional variability of climate change; granular pictures of changes in temperature, precipitation and sea level rises in different locations globally.

-

Sea level rises have been established as likely averaging 0.5-3m by 2100, although this may increase to between 3-7m.

- The report quantifies climate sensitivity as between 2.5 °C and 4 °C for each doubling of carbon dioxide in the atmosphere.

- Extreme weather events are very likely to increase globally and particularly in specific regions such as the Sahel, India and South American monsoon areas.

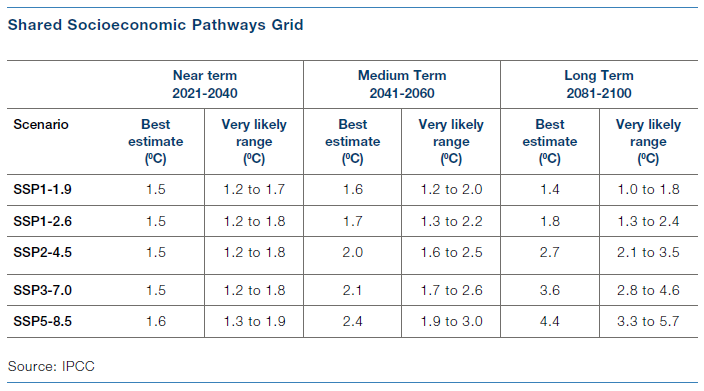

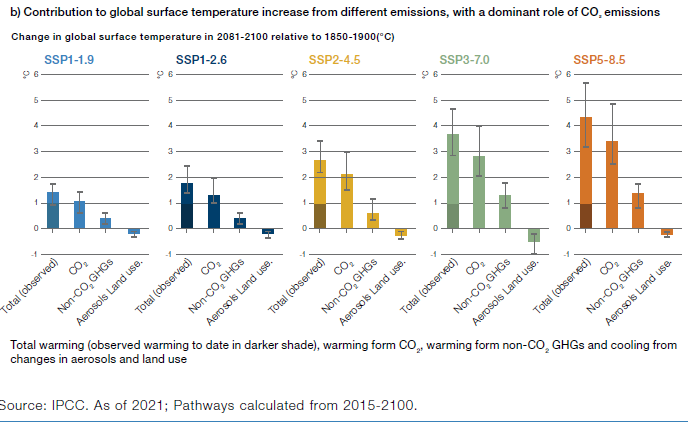

AR6 adjusted scenario modelling to take into account both the greater visibility of data and improvements in technology – both the modelling capabilities of computers and the various technologies helping to drive the world towards a lowercarbon future. Previously, the IPCC used two distinct forms of climate scenario, Representative Carbon Pathways (RCPs) and Shared Socioeconomic Pathways (SSPs). SSPs chart socioeconomic pathways whereas RCPs measure physical forcing. In previous assessment reports there was a matrix of SSPs and RCPs. For example, there could be an SSP2/RCP4.5 or SSP3/RCP6.0 world. In recognition of the fact that it is impossible to separate socioeconomic activity from the forcings associated with this activity, the IPCC has now retired RCPs and focuses solely on SSPs.

SSPs give a best estimate and range of very likely outcomes for global heating in three distinct time periods – 2021-2040, 2041-2060, 2060-2100. SSP 1-1.9 is the pathway associated with maintaining temperatures below the crucial 1.5-degree level.

SSPs seek to provide narratives that explain the potential path of carbon emissions from a societal and economic standpoint, taking into account both concrete elements such as population density and GDP per capita and more nuanced, abstract ideas, like the extent to which countries are prepared to work together to tackle climate change, whether technology is able to address global heating and how much the move to a green economy is able to prompt a levelling-up of less developed nations. SSPs also employ a more sophisticated and nuanced understanding of the interplay of different emissions, with a greater focus placed on the role of methane in global heating as well as the mitigating impact performed by aerosol emissions(5). This interplay of the two dominant environmental crises of recent years – global heating and ozone destruction – is complex and nuanced, as can be seen from the chart below.

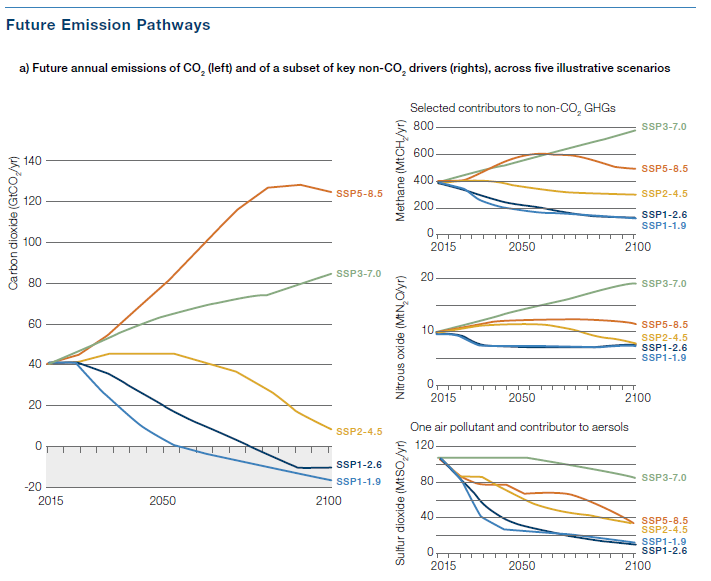

The SSPs provide a more detailed and yet intuitive picture of the paths of global heating associated not only with emissions but crucially with the geopolitical and economic backdrops against which these emissions are released. The chart below shows the emission pathways associated with these SSPs.

The IPCC is now working to pull together a Synthesis Report, which will represent the final element of the AR6 process and will be released in September 2022. This Synthesis Report will bring together all the different aspects of AR6 and will seek to provide further guidance on the action needed to address climate change. The first section of the Synthesis Report, ‘Current Status and Trends’, covers the historical and present period. The second section, ‘Long-term Climate and Development Futures’, addresses projected futures up to 2100 and beyond. The final section is ‘Near-term Responses in a Changing Climate’, considers current international policy timeframes, and the time interval between now and 2030-2040. The Synthesis Report will be viewed in draft at the United Nations Climate Change Conference (COP26) in Glasgow in October and November 2021. We should expect the release of this report to garner significant coverage and further sharpen the pace and intensity of action on climate change.

The next iteration of the IPCC’s process, AR7, will be released in 2028.

Chapter 3 The Paris Agreement

Key Points

-

-

-

-

-

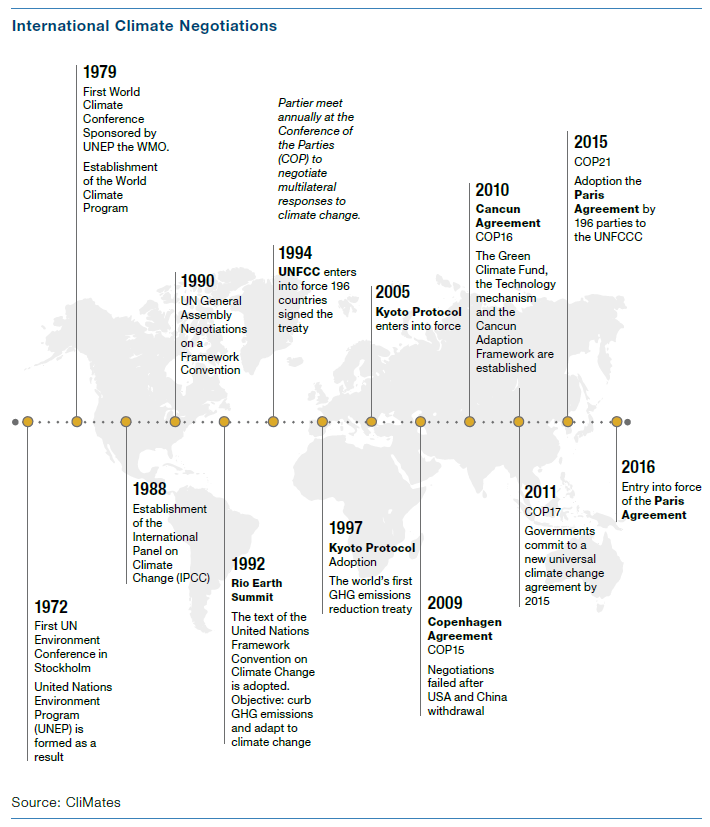

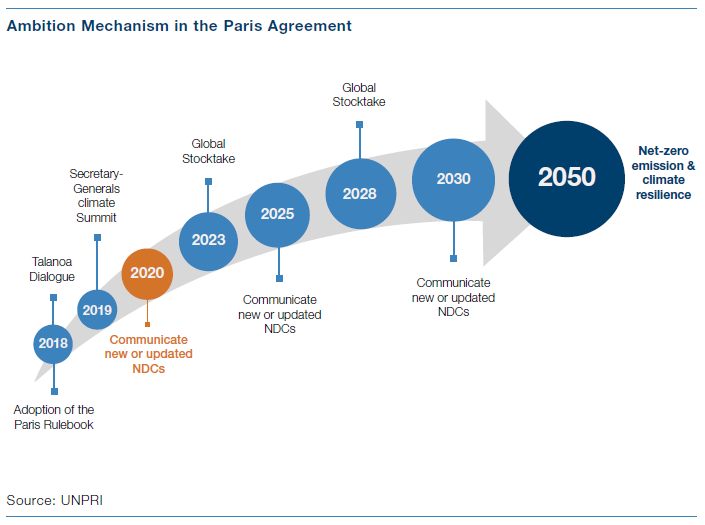

The Paris Agreement was signed in December 2015 by 196 countries at COP21.

-

It is the most widely-accepted and binding global climate agreement to date.

-

It has significant implications for the fianacial services industry.

-

-

-

-

Looking at the Shared Socioeconomic Pathways scenarios for climate change modelling, one thing is immediately clear: addressing the challenges of climate change requires globally coordinated action. It will not be enough for developed nations to go it alone, or for there to be any consideration of markedly different approaches to tackling the crisis. Paris provided a clear blueprint for coordinated global action and yet it also highlighted the challenges facing the international community when it comes to the unique issues presented by climate change. As the SSPs make clear, it’s impossible to disentangle the specific goals of carbon emission reduction from other socioeconomic challenges, such that any attempt to address climate change must necessarily also take into consideration the global imbalances of wealth and development that mean that different countries are at different stages along the path to dramatically reduced carbon emissions and are each more or less able to bear the cost of transitioning.

Serious efforts to limit global heating began with the Rio Earth Summit in 1992, followed by the Kyoto Protocol of 1997. The latter issued legally-binding obligations for developed nations to reduce their carbon emissions in the years 2008-2012. The Doha Agreement covered the years 2012-2021. The US did not ratify the Kyoto Protocol, while Canada renounced it in 2012. All 37 other ‘Annex 1’ countries that ratified the Protocol met their obligations – essentially the EU and EEA, Australia, New Zealand, Ukraine and Japan.

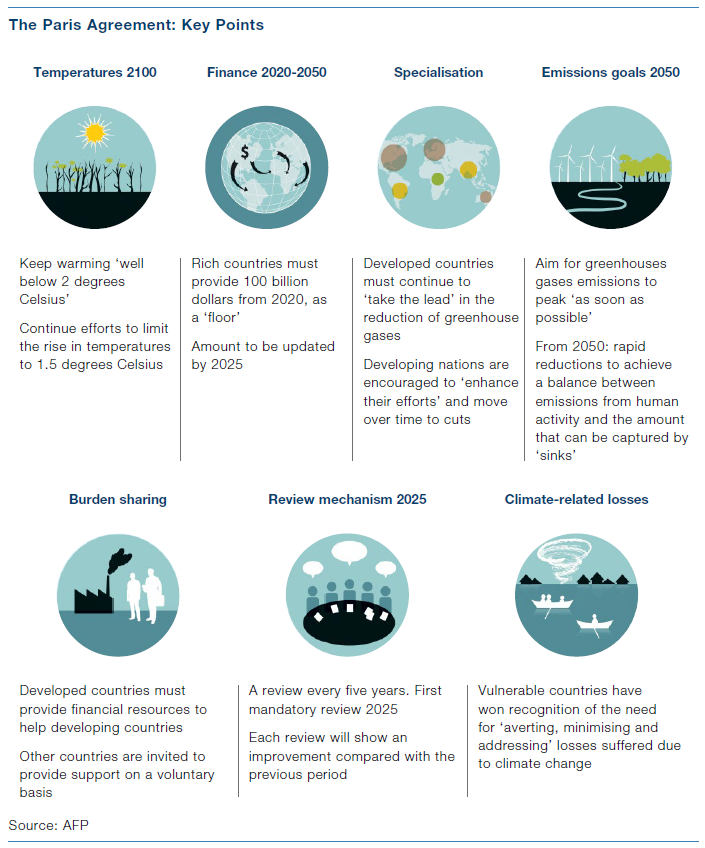

The Paris Agreement is the fruit of decades of work by governments and nongovernmental agencies to establish a roadmap towards a future in which global heating is kept below levels which would be severely damaging to the planet as a whole. It is a legally binding international treaty that was adopted at the COP 21 in Paris, on 12 December 2015 and entered into force on 4 November 2016. The goal of the agreement is to limit global warming to ‘well below 2, preferably to 1.5 degrees Celsius,’ compared to pre-industrial levels. In order to achieve this longterm goal, countries have agreed to begin to move towards carbon neutrality as swiftly as possible, with a general goal of achieving a climate-neutral world by 2050. While the US briefly withdrew from the Agreement under the Trump Presidency, it has now re-ratified, meaning that the vast majority of the globe now falls under the aegis of the agreement (only Iran and Turkey remain outside the accord as far as major polluters go).

3.1 The Mechanics of the Agreement

-

Nationally Determined Contributions (NDCs) were submitted by countries in 2020, showing the path each intended to take to achieve compliance with Paris Agreement goals.

-

There remains some way to go for many countries in order to meet the requirements of the Paris Agreement.

- There is an ‘ ambition mechanism’ built into the NDCs, such that targets will become more testing as time goes on.

The mechanism for achieving this goal is a series of increasingly aggressive 5-year plans, each of which has been scrupulously designed using the best available science with the aim of transforming the global economic and social landscape. Countries were required to submit their Nationally Determined Contributions (NDCs) in 2020, outlining how and when they will reduce greenhouse gas emissions in line with Paris Agreement goals. The NDCs also outline the steps each country will take to adapt to the challenges of a warmer world.

Alongside the NDCs, countries had to set out non-binding development plans that establish priorities and strategies for ensuring that emissions are kept low over the long-term.

The NDCs will be monitored via a series of ‘Global Stocktakes’ every five years that measure the extent to which goals are being met. Article 13 of the Paris Agreement articulates an ‘enhanced transparency framework for action and support’ that establishes harmonized monitoring, reporting, and verification (MRV) requirements. Both developed and developing nations must report every two years on their mitigation efforts, and all parties will be subject to technical and peer review.

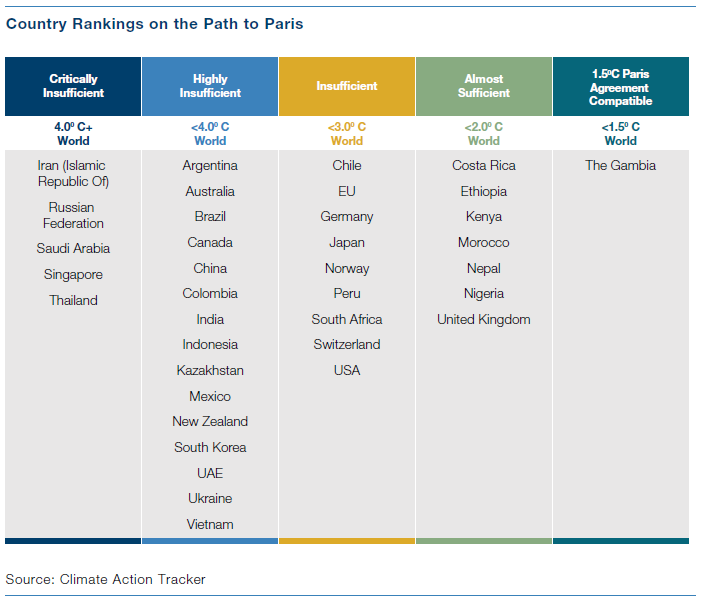

Different countries have approached the NDC process in different fashions. It’s important to note that, according to the Climate Action Tracker, only two countries’ NDCs are currently adequate to meet the 1.5-degree target – The Gambia and Morocco – while six countries – India, Bhutan, Philippines, Kenya, Costa Rica and Ethiopia – hit the 2 degree target. At the other end of the scale are countries like Turkey, who have not ratified the Agreement, and Russia, Saudi Arabia, Ukraine, and Argentina, whose NDCs are viewed as woefully insufficient.

It’s important to recognise the accretive and ratcheting nature of the NDCs, and the in-built (some would say optimistic) momentum that is anticipated to develop as the path to 2050 progresses. As it stands, the pledges made by countries in the Paris Agreement will not keep global heating below 1.5 degrees (or even, for that matter, 2 degrees)(6), but it is hoped that the ambition mechanism will see an increasing level of impetus twinned with further technological advances to drive more substantial gains in the latter years of the timeline.

3.2 Green Finance in the Paris Agreement

-

Financial services will have a key role to play in the move to a zero-carbon world.

-

The Paris Agreement is crucial in that it recognizes the need for developed nations to help less-developed nations meet their Paris Agreement goals.

While the Kyoto Protocol only addressed developed nations, the Paris Agreement’s greatest challenge and – thus far – greatest success has been in bringing on board less developed nations. As such, developed nations have had to agree to support those less wealthy states who are both less able to pay for the transition to carbon neutrality and often more exposed to the depredations of a warmer world.

Developed nations have initially agreed to provide $100 billion each year to less developed nations to help them meet the cost of transitioning to a low-carbon future. This figure will be re-assessed (and likely increased) in 2025. The financial side of the Paris Agreement will largely be channelled through the UN’s Green Climate Fund, although there are a number of other private and non- governmental organisations that will help disburse the funds. One of the key areas of debate here is in how funds are spit between mitigation and adaptation. There has thus far been a heavy preference for spending money on mitigation, such that there has been significant focus in recent years on encouraging adaptation planning, particularly for those less-developed nations most at risk from climate change.

From green bonds to climate-related securitisation and factoring, the financial services industry will play a central role in helping countries structure and finance the transition to a zero-carbon world. There will be increasing interaction between public and private institutions as the cost and requirements of decarbonising become clear.

The question of who pays for climate-related environmental damage was a central part of the Paris Agreement negotiations. Even in the event that global heating is kept below the 1.5-degree level, there will still be significant heating in certain regions and more regular and severe extreme weather events. Previously loss and damage had been viewed as part of adaptation, but it is now recognised as a separate pillar of the Paris Agreement. Already agreed is a $420m climate risk insurance fund provided by the G7 and the design and implementation of a Climate Risk and Early Warning Systems (CREWS) Initiative. The Agreement has further undertaken to adapt the Warsaw Mechanism, a model for addressing loss and damage that expired in 2016, better to reflect the disproportionate burden borne by less developed nations when it comes to climate risk.

While the later chapters of this paper will explore the specific investment implications of the move to a carbon-neutral world (and the concomitant considerations of the economic repercussions of the inevitable global heating), it’s worth noting that the Paris Agreement is already having a material impact on corporations (and their investors). In the first case of its kind, Milieudefensie et al vs. Royal Dutch Shell in May 2021 saw the oil company, the world’s 9th-highest corporate polluter, stand trial in The Hague for the limited nature of its climate pledges (Shell had stated in 2014 that it believed that the Paris targets were unattainable and did not plan to change its business model away from oil and gas; with the adoption of the Paris Agreement, Shell set a handful of limited emissions reduction targets).

In its ruling, the court found Shell’s current sustainability policy to be insufficiently ‘concrete’, and that its emissions were greater than that of most countries. Due to these factors, the court ordered that Shell must reduce its global emissions by 45% by 2030 compared to 2019 levels; the reduction targets include emissions from its suppliers and buyers. The court declared the order provisionally enforceable, meaning that the order has immediate effect, even if one of the parties appeals the ruling (which Shell has said that it intends to do).

Chapter 4 Corporations, Regulation and Climate

Key Points

-

-

-

-

-

Companies will increasingly face significant regulation related to climate change.

-

What climate pledges have been made and how will companies be held to these pledges?

-

What are the various scopes of emissions that will be monitored?

-

-

-

-

Corporations are increasingly finding themselves pressured from a variety of different angles when it comes to sustainability. We will outline later in the paper our thoughts about stewardship and activism, but it’s worth briefly considering this from the company’s point of view. Firms are not only having to deal with a shareholder base that is both increasingly vocal in the face of backsliding on ESG targets and increasingly unwilling to invest with firms that do not prioritise sustainability and other non-financial goals; governments are also imposing ever-stricter regulations on corporations, and it is clear that, in particular, firms domiciled in Scandinavia, Benelux and Germany are having to meet ever-more-stringent emissions standards from local regulators. Furthermore, there is international pressure on firms that are seen to be polluting less developed nations in carrying out their operations. Finally, and perhaps most importantly, public opinion now seems to be firmly on the side of sustainability, and there are more avenues than ever to let a company know publicly that you disapprove of its methods. An example of a successful campaign waged largely on social media and in the press is the move to limit deforestation by palm oil corporations. While it’s a battle that is far from won, US food giant Cargill recently pledged to ensure none of its plantations contributed to deforestation.

We are increasingly seeing corporations making the kind of climate pledges that we traditionally saw from countries. Where these pledges are limited or not sufficiently robust, companies have been put under pressure from both regulators and shareholders. This has particularly been the case for the oil and gas industry, where we have seen the Shell case mentioned above and also significant pressure brought to bear on Exxon. It’s clear why this is the case: the products (in a broad sense) of just 100 private and state-owned fossil fuel companies were linked to 71% of global industrial greenhouse gas emissions since 1988.

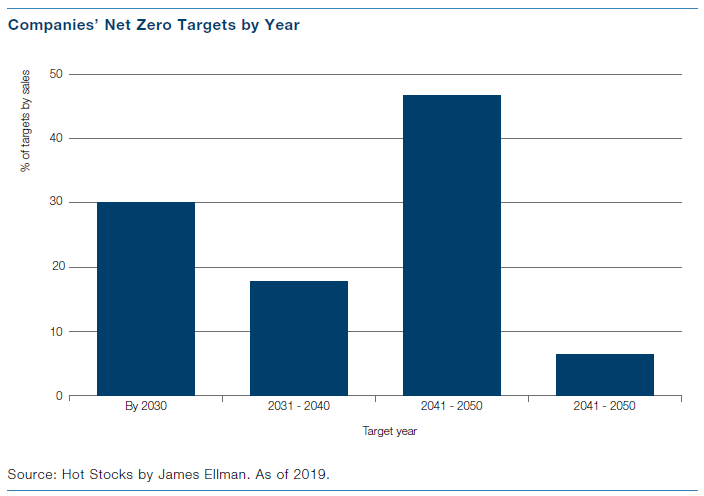

It is not only the oil and gas industry that is under pressure, however. From fast fashion retailers to mining companies to agriculture, companies are having to radically rethink their business models in the wake of the rise of the sustainability movement. According to a recent paper by the University of Oxford called ‘Taking Stock’, around a fifth of the world’s largest 2,000 firms have made some form of net zero pledge, a figure that has risen significantly in the past few years. Of these, the majority are 2050 targets, with an increasing minority targeting 2030.

Tech companies have perhaps some of the most far-reaching goals. Last year, Microsoft pledged to be ‘carbon negative’ by 2030, meaning it would remove more carbon from the atmosphere than it emits. By 2050, it aims to have compensated for all of its historical emissions through carbon removal projects. Apple says its products and supply chain will be carbon neutral by 2030 and Google has committed to be powered exclusively by renewable energy by 2030 and claims it has already wiped out its carbon footprint by offsetting emissions.

Large numbers of companies, including consumer-facing firms such as Ikea, PepsiCo and Levi’s, are also signing up to the Science-Based Targets initiative (SBTi), which helps companies calculate emissions targets aligned with the Paris agreement ambition of 1.5°C. More companies have signed up in the first half of 2021 than in the whole of 2020. An SBTi analysis of 338 large companies with science-based pledges found they had reduced combined emissions by 25% between 2015 and 2019.

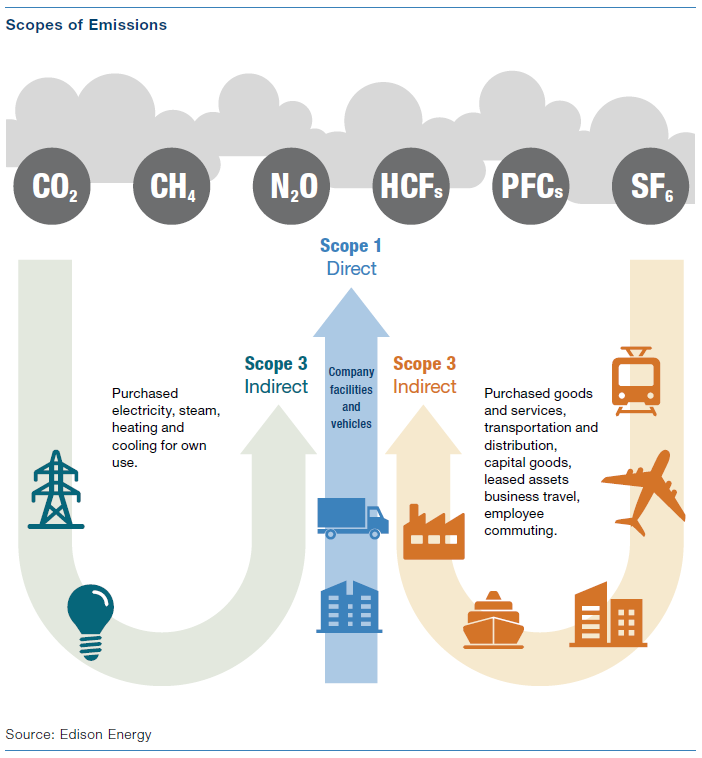

Often, you will hear reference to different Scopes of emissions in discussions of environmental regulation. Greenhouse gas emissions have been categorised into three groups or ‘Scopes’ by the most widely-used international accounting tool, the Greenhouse Gas (GHG) Protocol. Scope 1 covers direct emissions from owned or controlled sources. Scope 2 covers indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed by the reporting company. Scope 3 includes all other indirect emissions that occur in a company’s value chain.

Part 2

Investing in a Warming World

The world is getting warmer; even if we act now, we must still prepare for a hotter world.

This will have significant implications for investors as they consider the future asset mix of their portfolios.

Companies will have to think about both the physical and transition costs they will face, as well as understanding which assets they currently carry on-balance sheet that may be rendered valueless by climate change.

Introduction

If there was one message that rang clear from the IPCC’s AR6, it was that we must as a planet prepare for temperature rises. Even should we manage to achieve the most ambitious targets of the Paris Agreement, there will still be global heating to contend with, and this heating will be unevenly distributed across different regions. The AR6 report indicated that all regions should prepare for rising temperatures, heavy rainfall and drought. If we manage to keep to around 1.5-degree warming from pre-industrial levels, we will still see rising seas and growing deserts, will still see some areas of the planet become more or less uninhabitable. Arid areas in the tropics from India to Arabia to the Sahel will see temperatures rise on average by 5-7 degrees annually. India, for instance, will see average temperatures rise from 30 degrees to 35 degrees. Within the country, this divergence will be even more extreme, with some areas seeing temperatures regularly exceeding 40 degrees. And this is the best-case scenario.

Using the IPCC’s Shared Socioeconomic Pathways and applying SSP 1-2.6, by which global mean temperature increase stabilises around 1.8-2C by end of century, we see a picture of global temperatures that is both more troubling and more divergent. While some parts of the world will benefit from these rising temperatures – meaning that, for instance, sea freight will be able to pass to the north of Russia, dramatically reducing journey times from Northern Europe to Japan; parts of Canada and Russia that were previously too cold for viable economic activity will be habitable – most of the planet, and particularly less developed nations, will suffer. Once we reach more extreme climate pathways, temperature rises are widespread and uncontrolled, bringing with them catastrophic weather events and drought.

It may seem that 1.5 or even 2 degrees of warming does not sound hugely significant. We experience temperature fluctuations far larger than this in the course of a single day. But it’s important to point out that temperatures during the last ice age, when the polar caps crept down to cover all of Ireland and Poland, as well as large swathes of Britain and Germany, temperatures were only 6 degrees lower than they are now. A small change in mean temperatures can make an enormous difference. The heatwave that struck the Pacific Northwest in the summer of 2021 was statistically impossible without the 1.2 degrees of warming we have experienced.

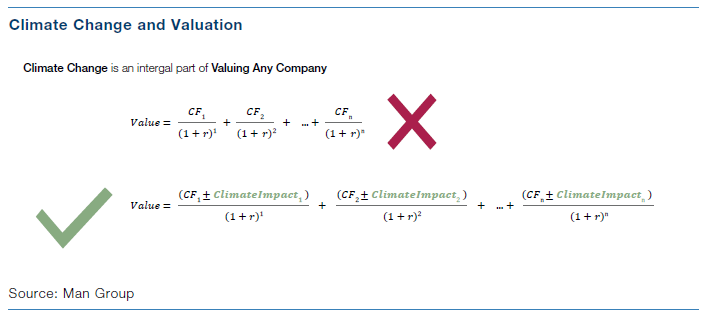

We believe that investors should be preparing their portfolios for a warming future. This is not to say that we should give up on efforts to mitigate climate change: far from it. Rather, we believe that it ought to be possible to fashion an investment strategy that is both ethical, sustainable, and future-proofed against the inevitable impact of global heating. We are only at the very beginning of what will be a multicentury narrative surrounding the intersection of asset management and climate change. If we as an industry are going to survive and thrive in this new era, we need to recognise that even if we manage to achieve all our aims in terms of cutting carbon emissions, we will still have a warmer world at the end of this century than we had when most of the models and concepts that dominate our investment practices were originated. We need to know what impact a changing climate will have on the firms we invest in and how we can act to shape our portfolios so that they are prepared for what lies ahead. Climate change will henceforth be an integral part of valuing any company.

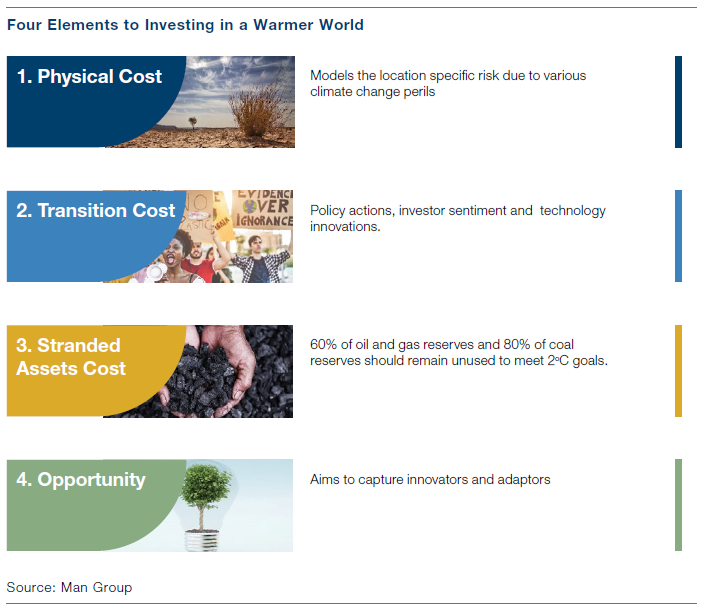

We will discuss in this part the impact of operating in a warming world on the way investors should think about asset selection in their portfolios. However, unlike in the previous chapters in this paper, we will not look at specifically green or sustainable investments, but rather at the way that global heating will necessarily shape the business models of all corporations in all countries. We will consider four areas in particular:

-

Physical Cost: the way companies are impacted by climate change will largely be a function of where they operate. Those firms whose operations are based in areas that will see either a significant increase in temperatures or a significant increase in extreme weather events will have to factor the cost of these increased risks into their business models.

-

Transition Cost: companies will have to meet the cost of transitioning to a lowcarbon economy. For some, this will be manageable, for others, it will require a wholesale alteration of their business models. Companies will have to meet increased regulatory demands and there will be an increased cost of capital for those companies falling behind in the move to net-zero.

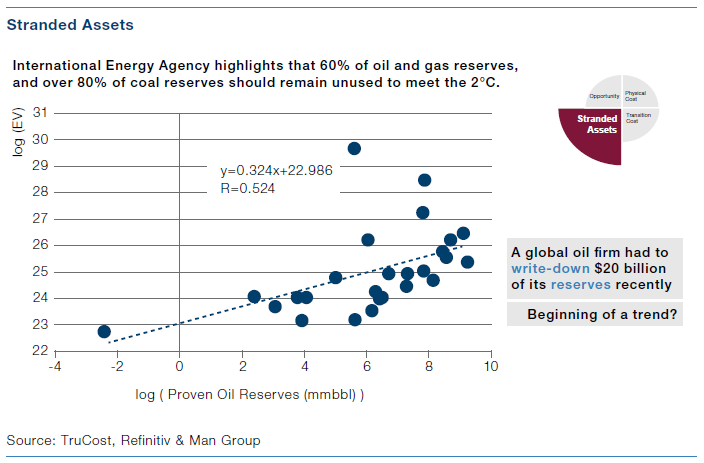

- Stranded Assets Cost: the balance sheets of many of the world’s energy companies, utility firms and mining companies are currently carrying assets whose valuations do not correctly reflect the impact of climate change. We have said above that global heating must now be thought of as a vital component of company valuation and this is an area that we believe will see increasing focus as we move through the next decade. 60% of oil and gas reserves and 80% of coal reserves will remain unused if we are to meet climate goals of maintaining warming below 1.5 degrees.

- Opportunity: while some firms will struggle and even disappear because they fail to adjust to the realities of global heating, others will thrive. We view opportunities as arising from a variety of locations here – both green securities (which we have covered above), but also companies in legacy sectors whose management teams rise to the challenge of transitioning to low-carbon business models, and firms operating in areas that will see benefits from global heating, such as shipping firms able to use new routes and those based in regions of Russia and Canada that were previously too cold for economic activity to flourish.

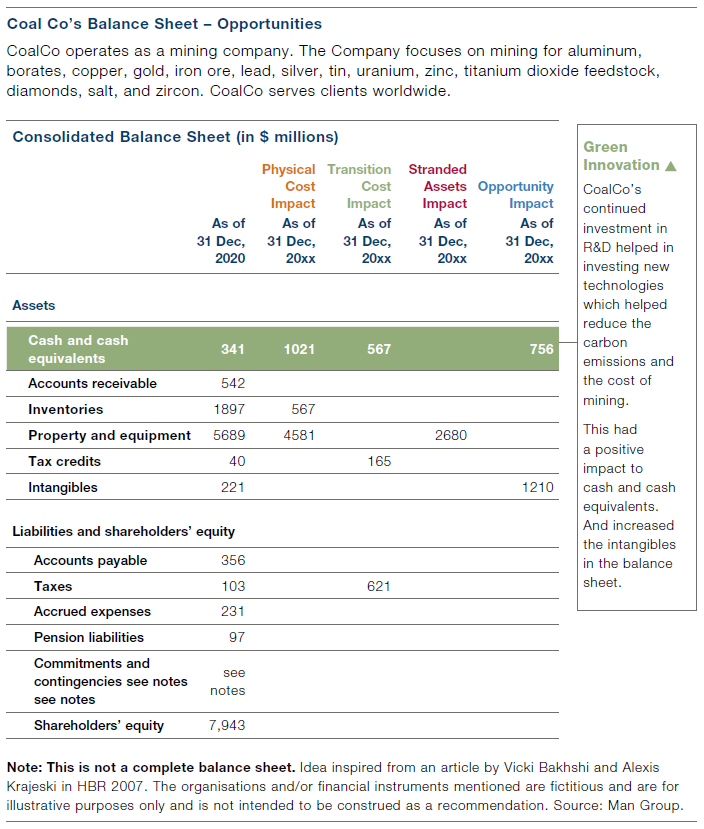

For each of these areas, we will illustrate our thoughts with the example of CoalCo, a fictional coal mining company. This will permit us to explore in detail the ramifications of the move to zero- carbon on a (fictional) firm caught in the crosshairs of the green revolution.

One final comment when it comes to the material and analysis presented here: we believe it’s crucially important that the real cost of climate change is clearly established and visible to the markets. This narrative is something that the TCFD pushes hard: that once markets come to understand the potential costs of climate change, they will recognise that the cost of mitigation is relatively low in comparison. This idea is outlined at length in an excellent paper by Johannes Stroebel and Jeffrey Wurgler of the NYU Stern School of Business entitled ‘What Do You Think About Climate Finance?’ In the paper, the researchers interviewed 861 finance professionals, economists and other practitioners to establish current thinking on the financial industry’s response to climate change. One element of the paper that is of particular relevance here is the fact that respondents believed by an overwhelming margin that current asset prices underestimate the real cost of climate change and that global warming poses an existential threat to the investment industry.

Chapter 1 Physical Cost

Key Points

-

-

-

-

-

Physical cost consists of revenue and operational risks.

-

The cost to a company is dictated by what industries and regions they operate in.

-

Climate change will deepen global inequalities and reduce global GDP.

-

-

-

-

The Physical Cost of the move to a zero-carbon world is calculated by looking at the way that several location-specific drivers feed into a company’s operations. We might think of these drivers as two separate classes of risk – revenue risk, which calculates the change in GDP growth for each company’s key markets and how these will impact demand, and operational risk, which will look at how various elements of a warmer world will impact a company’s business practices. This combines the condition and supply of the labour force, the demand for, and cost of, energy, and the impact of extreme weather events on a company’s operations.

1.1 Revenue Risk

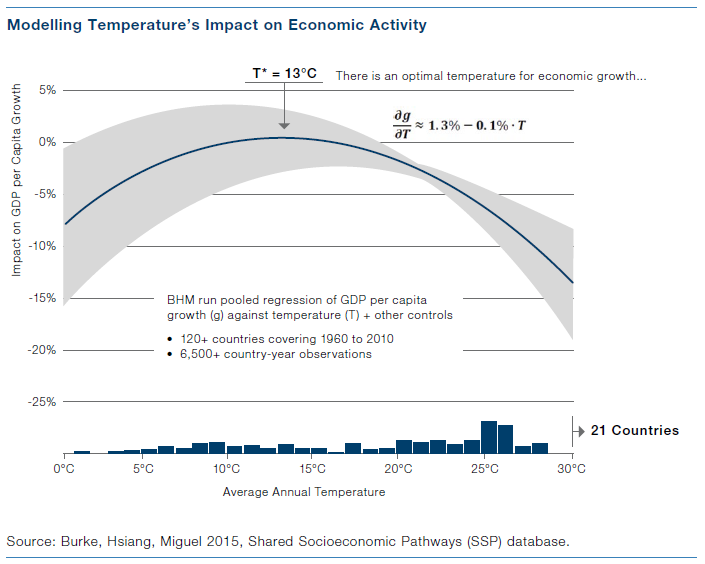

The chart below shows how economic activity changes under a variety of different temperatures. We put together this chart inspired by a paper in Nature by Burke, Hsiang and Miguel at Stanford’s Department of Earth Sciences entitled ‘Global Non-Linear Effect of Temperature on Economic Production.’ The chart illustrates that there is a ‘sweet spot’ temperature for economic activity – around 13 degrees – with productivity gradually declining as temperatures rise or fall from this point. Hsiang et al’s paper makes clear that this relationship holds for both developed and less developed nations and has been backtested to 1960 across agricultural and non-agricultural activity. The paper was the first to establish an unequivocal linkage between temperature and economic activity and concluded that ‘unmitigated’ global warming would reduce global GDP by around 23% by 2100 and would significantly widen income inequality, with developed nations seeing less impact than less developed nations due to the unequal distribution of rising temperatures.

The most compelling analysis of the relationship between GDP growth and temperature comes from a paper by Burke et al. in Nature entitled ‘Global nonlinear effect of temperature on economic production.’ This paper contends that, across both developed and less developed countries, productivity declines significantly at high and low temperatures. The relationship, they claim, is globally generalizable, unchanged since 1960, and apparent for agricultural and nonagricultural activity in both rich and poor countries. These results provide the first evidence that economic activity in all regions is coupled to the global climate and establish a new empirical foundation for modelling economic loss in response to climate change. The paper suggests that, given continued unmitigated climate change, global incomes are likely to decline by around 23% by 2100 as a result of the relationship illustrated in the chart above. What is clear is that, given the current distribution of the global population and presuming that the data above hold true, rising temperatures may lead to either a significant reduction in productivity or mass migration away from places that have become uninhabitably hot to more temperate regions away from the equator.

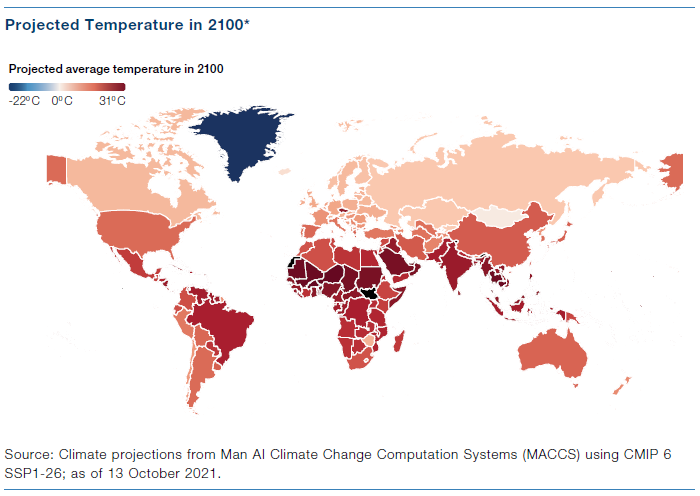

The three maps below are constructed using the SSP1-2.6 pathway, by which global mean temperature increase stabilises around 1.8-2C by end of century. The first map shows that, as discussed above, global average temperatures will continue to rise precipitously and unevenly, with heating concentrated in the tropics.

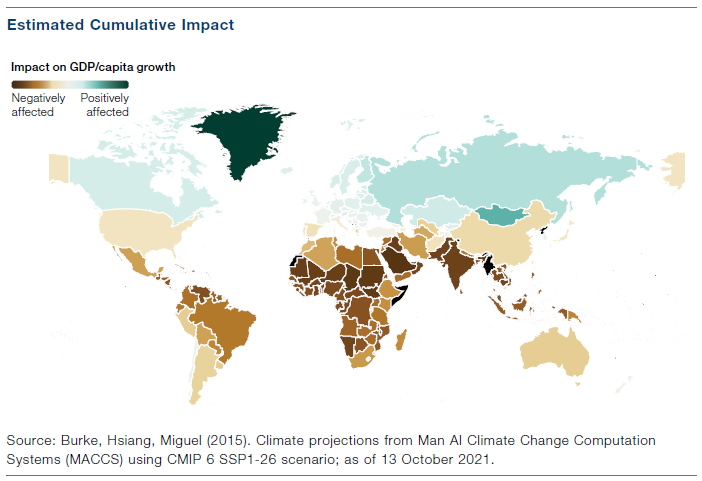

The next map shows the expected economic impact that global heating will have on different countries globally in 2100, again presuming the SSP1-26 is followed. This ranges from a 80%+ drop in GDP/capita in countries including Kuwait, UAE, Saudi Arabia and India to a markedly positive impact for countries including Finland, Russia and Canada. The clear message here is that inequalities between less developed and developed nations will be accentuated by the impact of global heating. We have already witnessed the early signs of civil unrest and even revolution that such inequalities foment – this was the story of the Arab Spring, and arguably the story of ISIS and Boko Haram. There is the potential for more and more extreme incarnations of this kind of violence should such inequalities persist and intensify.

Beyond this relatively high-level analysis, we are able to refine our estimates of revenue losses and costs due to climate change by downscaling climate models – effectively refining them to render them more granular so that we can assess risk on a local scale, even looking at the impact of climate change and consequent natural disasters on an asset-level basis. Using econometrics, we transform the localised, downscaled climate models into assessments of the revenue and cost implications for the companies we are surveying.

1.2 Operational Risk

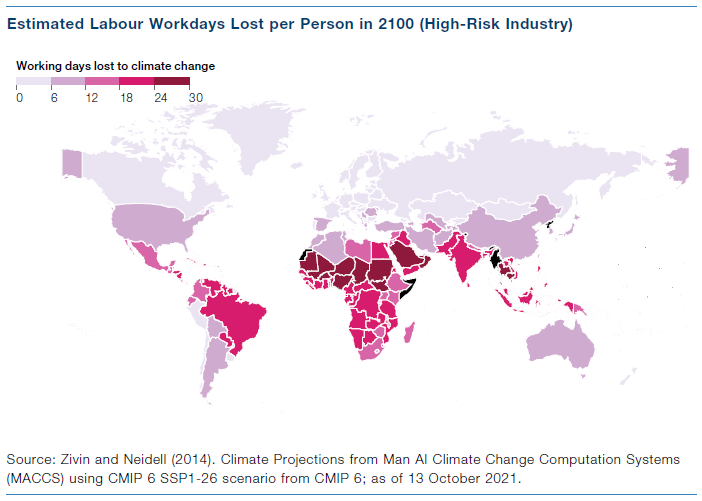

When it comes to the direct impact on corporations, we can view it as both a demand side problem and a cost problem. The map above shows the extent to which firms will see demand drop in those areas whose GDP shrinks dramatically because of global heating. The map below shows the other side of this coin: the minutes lost per person per day for firms in high-risk industries in 2100. We define high-risk industries as being: fishing, agriculture, forestry, manufacturing, utilities, mining and transportation. While those in northern climes will see little change in the efficacy of their workforces, the impact for companies operating in the Sahel, Bangladesh, Arabia and South America will be far more significant – remember that this includes the effect of increased extreme weather events as well as global heating.

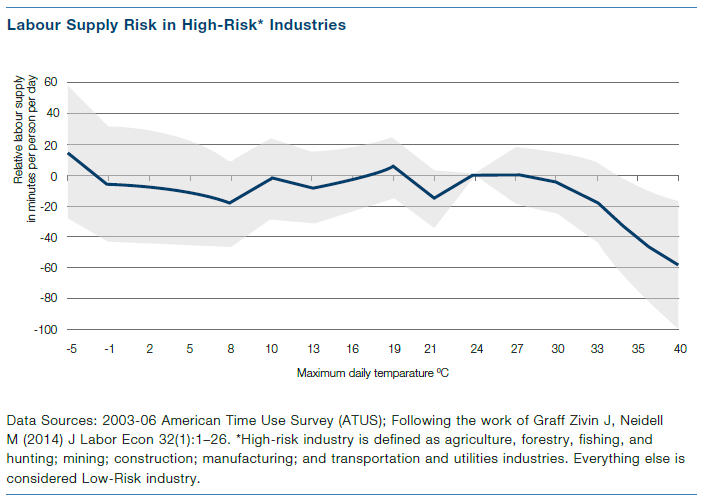

The chart below illustrates how the supply of labour changes under different temperatures. This analysis draws on the work of the American Time Use Survey and the paper ‘Temperature and the Allocation of Time: Implications of Climate Change’ by Graff Zivin and Neidell in the Journal of Labor Economics. It shows that – as indicated in our findings above – there appears to be a series of sweet spots for economic activity in the mid-to-high teens, while productivity declines precipitously once temperature rise above 30-degrees.

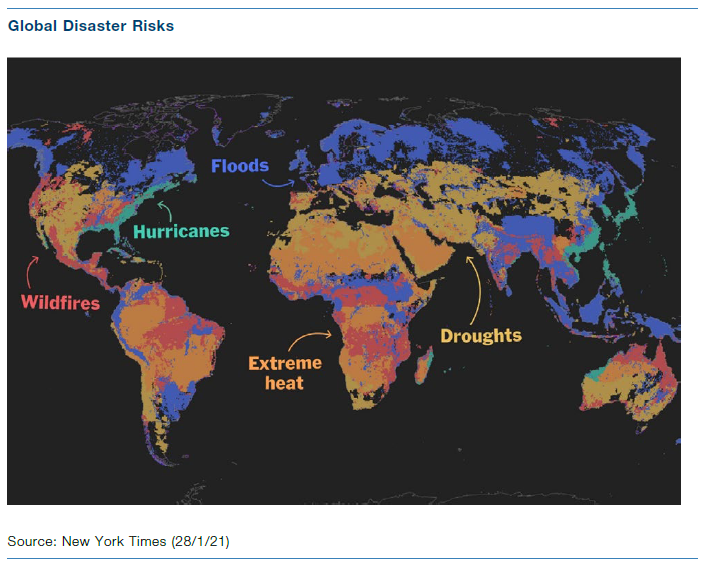

We have so far spoken only about the operational implications of rising temperatures. Of course, there is also the increasing cost of natural disasters, which will strike with greater frequency and cause greater damage. Insurance costs will rise precipitously and there is likely to be widespread migration away from low-lying coastal areas. Different regions have different risks, as the map below illustrates. It is necessary for investors to map these risks onto the companies in their portfolios as well as factoring in greater insurance costs in the future.

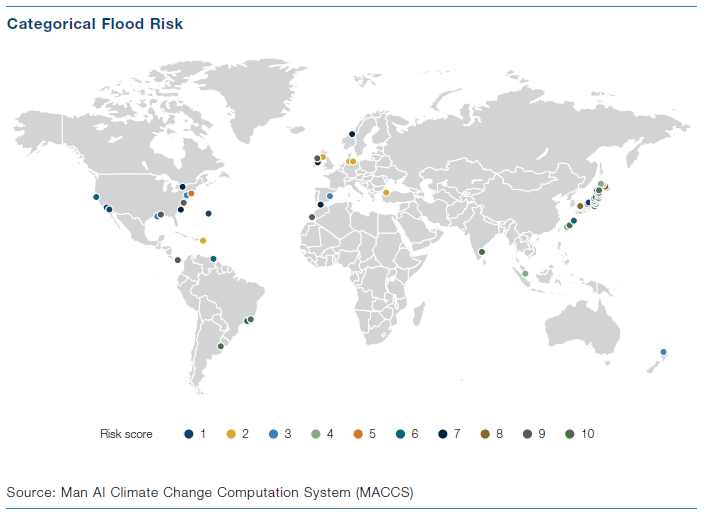

To turn to CoalCo, we use proprietary models to assign a risk score to each of its global locations for each respective disaster risk. In the map below, we show flood risk scores for the company, illustrating how certain areas will see greater costs associated with floods than others. Once we have combined these various risk scores we are able to assign an overall score to CoalCo’s operations and estimate the potential losses from the impact of natural disasters.

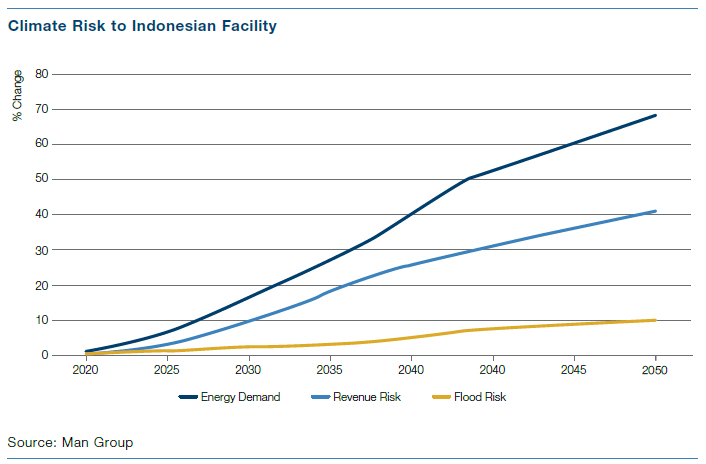

We can drill down further here, looking at companies on a facility-by-facility basis. While this may be viewed as overkill for minor portfolio positions, where investors want to take a meaningful stake in a company, it is important to understand the range of exposures that each firm has to climate risks. Different locations will face different risks and these risks will be mitigated in different ways. It is also possible to map a company’s risk levels to the particular SSP that you expect to transpire, meaning that you can have a range of potential climate-related liabilities depending on the overall level of global heating that takes place. We might focus in on CoalCo’s Indonesian operations(Noting that Indonesia is at such high risk of flooding that it is moving its capital because of flood risk.). These operations are situated in Batam on the Riau Islands, just outside of Singapore.

We can model the risk of this specific facility using granular climate models and company data. As the chart below shows, flood risk to this facility is relatively manageable, but there will be significantly greater energy demand as temperatures rise (largely from the cost of cooling the facility and the increased cost of energy) and significantly greater revenue risk given the loss in GDP .

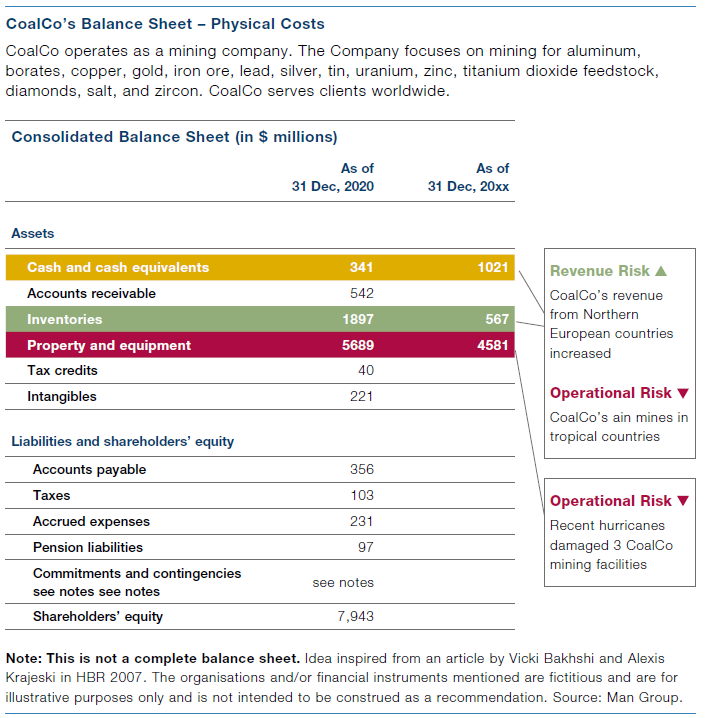

Now we consider the Physical Cost impact of climate change on CoalCo’s balance sheet. CoalCo happens to derive most of its revenue from Russia. As such, the firm will benefit as Russia’s economic activity increases. This translates to an increase in cash and equivalents for the firm. At the same time, many of CoalCo’s mines are in tropical regions where it has faced increased costs from higher energy demands, more frequent extreme weather events and a shortage of labour. This has had a negative impact on cash and has also seen a write-down of the PP&E line item as mines have been damaged by hurricanes.

Chapter 2 Transition Costs

Key Points

-

-

-

-

-

The move to net zero will mean that all companiesface some costs, whether to meet regulatory disclosure targets or to finance new technologies.

-

Transition costs will be highest for those in legacy industries.

-

Firms that do not embrace the move to net zero may find the cost of doing business becomes prohibitively high, for instance securing insurance or banking services.

-

-

-

-

The Transition Cost element of our analysis attempts to capture the impact of the move to a low-carbon future, capturing the risk to business from policy and regulatory actions, technological innovation and obsolescence, reputational issues and the change in investor behaviour as capital is allocated away from polluting firms and towards those who successfully rise to the challenge of net zero. The easiest way to estimate a company’s transition risk is via its carbon intensity. This gives an idea of how much the company has to change in order bring itself into compliance with emission reduction goals.

2.1 Charting Corporations on the Path to Net Zero

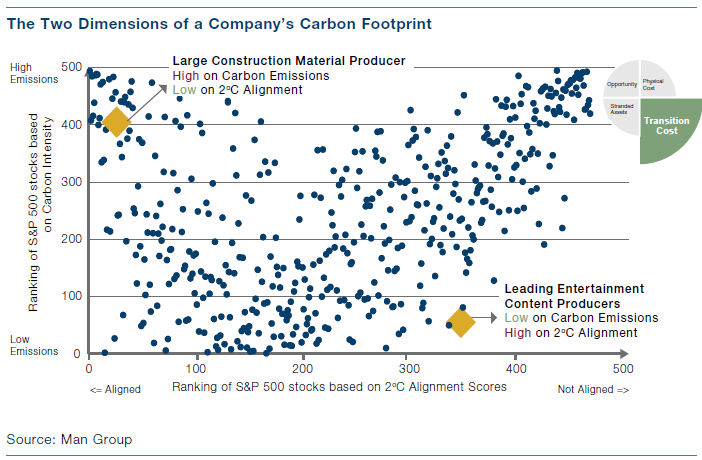

It goes without saying that companies begin their path towards net zero from different starting places, and that therefore the cost of transition is different based on how far the company needs to travel from its current business model to reach net zero. The chart below shows the two dimensions we use to track where a company is on its journey to net zero.

We have scored the S&P 500 according to two different elements. The first is what their current emissions are. This is obviously largely a facet of which business they are in. We then look at how closely-aligned they are to the emissions reductions required by the Paris Agreement. To do this we use data provided by the Science Based Targets Initiative. This is a partnership organization between the CDP (Carbon Disclosure Project), the United Nations Global Compact, the WWF and others, that has come up with a framework to determine the extent to which each industry must reduce their emissions if we are to achieve the Paris Agreement. The SBTI data looks at both the realistic measures firms in an industry might take to reduce their emissions and what lower-carbon alternatives there might be to their business models, before allocating each firm a series of emissions targets.

The top left point of the graph below represents a ‘Large Construction Material Producer’ which necessarily emits lot of carbon and hence scores very highly on the carbon emissions dimension. But we don’t have any alternative for cement yet, hence, in order to support the economy we have to allow cement companies to keep emitting. Therefore, notwithstanding the higher emissions, from an alignment angle this company scores amongst the highest in the S&P500 (note a lower score here represents better alignment).

On the other hand, let’s look at the example of a ‘Leading Entertainment Company’ on the bottom right. The company emits very low carbon but still doesn’t score well on the alignment angle because compared to its industry trend and based on what it could realistically achieve it is still emitting more than it ought to be emitting.

So transition costs are a function of both the current level of emissions and the potential for alternatives/reduction in carbon usage of each company’s current business model.

Transition costs can manifest themselves in a variety of different ways. It is, for instance, more difficult for heavily-emitting firms to secure insurance, given the greater risk profiles of their businesses. Seventeen major firms including Chubb, Generali, Swiss Re, Axis Capital, QBE, and Allianz have announced that they will limit insurance provided to energy firms because of climate concerns. AXA has announced that it will cease providing coverage to any new oil pipelines, coal plants, and tar sands projects. As the company’s CEO, Thomas Buberl, put it: ‘A +4°C world is not insurable.’

It’s also harder for such firms to get even basic banking services. HSBC, for instance, recently announced that it will no longer finance the construction of offshore petroleum projects in the Arctic, tar sands developments in Canada, or most coal-fired power plants. Other large banking institutions such as ING, BNP Paribas, Wells Fargo, Morgan Stanley, Legal & General, JPMorgan, Deutsche Bank, and the World Bank have announced similar policies regarding their relationships with fossil fuel companies.

It’s important to draw a distinction between 1.5-degree alignment and carbon intensity as measures of a company’s vulnerability to transition risk. Different firms will be in different positions as far as a number of elements extraneous to the mandates of the Paris Agreement. These include the stringency of local regulations and government interpretations of pledges – note that the Netherlands pursued Shell even though other energy firms are far less aligned; on the other hand, Australia has been consistently unwilling to penalise coal producers. There are also second-order impacts like investor sentiment and pressure from employees, suppliers, customers and other stakeholders. In order to achieve a rounded picture of transition risks, it’s important to consider not only where a firm lies in relation to its declared goals, but also to the second order pressures that it faces from its wider ecosystem.

One final point worth noting here: it may seem at first glance that we will therefore be predisposed to invest in companies who are less likely to face pressures from government, investors and their wider stakeholders. This is obviously a perverse situation and we remedy it by increasing the physical costs associated with these companies. This recognises the fact that transition risk and physical cost are to some extent mutually exclusive; that is, if a government cracks down on a company’s emissions it will face near-term costs to meet regulations but potentially be less impacted by overall climate change; conversely, firms who aren’t penalised may benefit in the near term but suffer more serious long-term consequences.

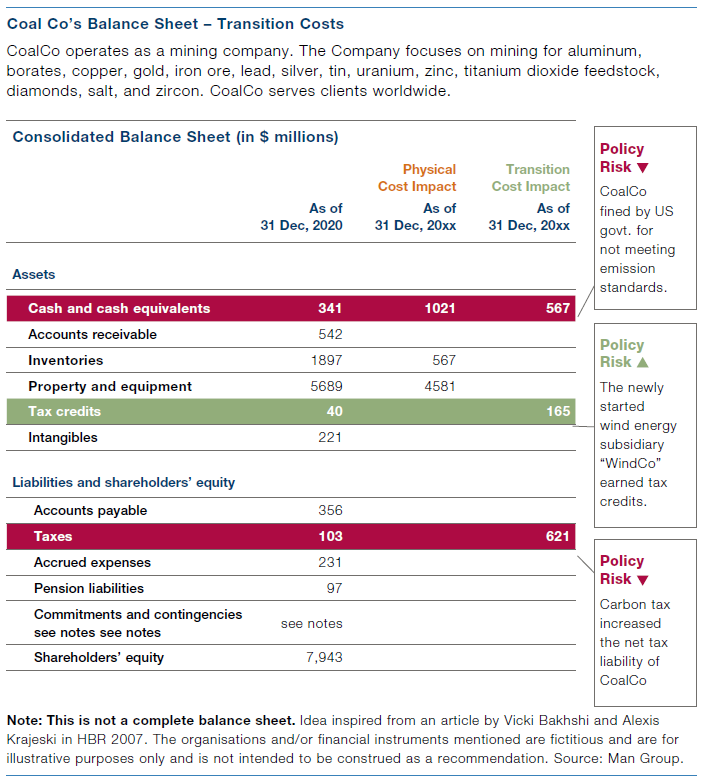

Let’s turn now to our fictional CoalCo, for whom transition costs will necessarily be high given its business model. We can see here the impact of policy and regulation on the company. The firm was fined for failing to meet emissions targets, reducing its cash and equivalents. It also had carbon tax liabilities, although these were somewhat offset by tax credits earned by its newly-launched subsidiary, WindCo.

Chapter 3 Stranded Asset Costs

Key Points

-

-

-

-

-

Stranded assets are most visible in the energy sector, where many reserves may never be tapped.

-

Companies will need to think realistically about the valuation of their assets in the light of climate change.

-

-

-

-

Reserves are a core element of energy company valuations, as shown by the chart below. This is notwithstanding the fact that the International Energy Agency has estimated that 60% of oil and gas reserves and over 80% of coal reserves should remain unused in order to meet Paris Agreement targets. It’s clear that there is something here that is not adding up, and either investors are betting that the move to net zero will be slower and less successful than current policy targets suggest, or they are over-valuing energy companies, which recently had to write down of $20bn of reserves globally.

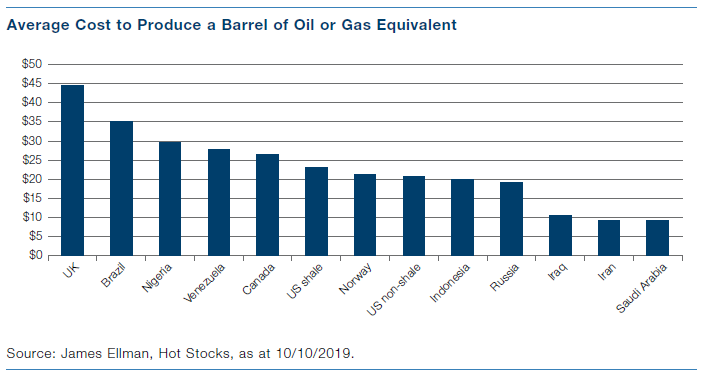

If hydrocarbon asset stranding does take place, it will either be driven by regulatory fiat – governments imposing limits on production and consumption of hydrocarbons – or technological change – leaps forward in renewable energy rendering oil, gas and coal uneconomical. As the chart below illustrates, energy firms in the West have a higher cost of extraction than their OPEC/Russian state-owned peers. This dynamic is key when it comes to understanding how energy firms fare in the move to a low/zero-carbon future. If fossil fuel reserves are stranded due to regulation, it is possible that the Western companies with their higher production cost locations may suffer the most pain. In contrast, if hydrocarbon asset stranding takes place due to technological change and cost reductions in the price of renewable power systems, then volume-oriented US companies may have time to deplete most of their reserves while national oil companies in such places as Saudi Arabia and Iran will wish they had pumped more and faster.

The likeliest outcome is a combination of the two elements, with regulation driving technological innovation in renewables, a scenario that would see both Western energy companies and their state-owned peers suffering equally.

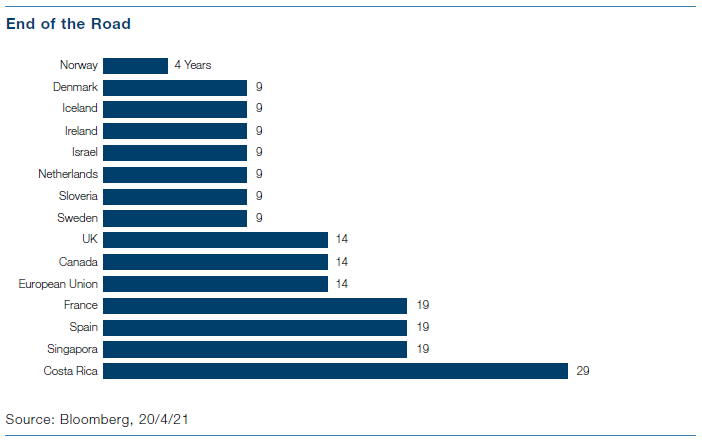

We have spoken so far about the energy sector as this is where the stranded asset issue is both most obvious and most potentially costly. But there will be stranded assets in almost all industries as the world moves towards a zero-carbon future. For instance, the chart below illustrates the years until various states will ban the sale of new cars with internal combustion engines. The transition to electric vehicles will necessarily leave stranded assets in its wake, both in terms of the cars themselves and the facilities used to manufacture them.

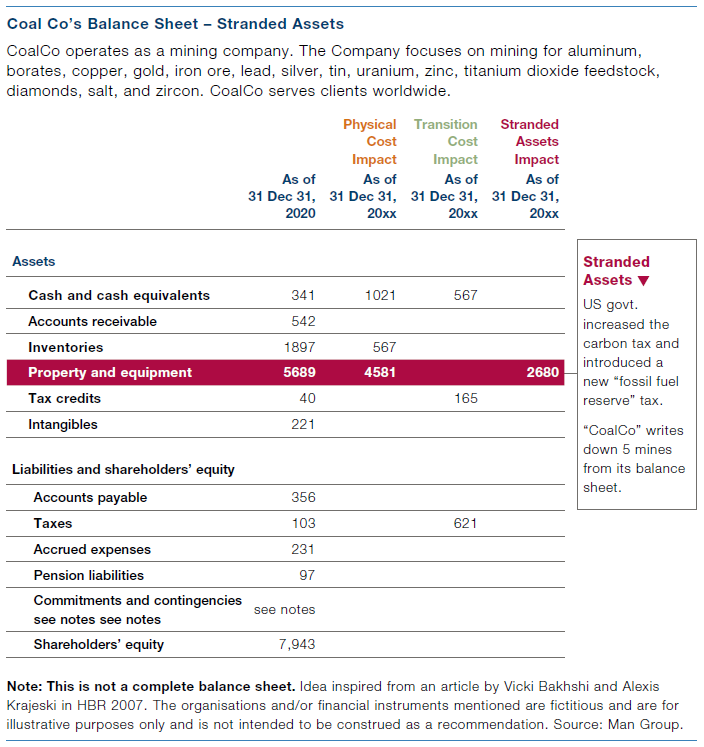

Let’s now return to CoalCo and see how stranded assets impact our fictional balance sheet. The answer is not good. In our putative example, the US government increased carbon taxes and imposed a new ‘fossil fuel reserve’ tax, which rendered five of the company’s mines uneconomical. These mines were then closed and written down to zero, a move reflected in the PP&E line in the company’s balance sheet.

Chapter 4 Opportunity

Key Points

-

-

-

-

-

The move to net zero presents companies with opportunities as well as risks.

-

Forward-thinking management teams will position their business to benefit from the changing corporate landscape.

-

-

-

-

Of course, as a careful read of earlier sections of this paper makes clear, the move to net zero presents management teams with as many opportunities as it does challenges. We will therefore finish this section with a consideration of the possible benefits that will accrue not only to those green economy firms able to seize this historical moment, but also to those traditional firms whose management teams are forward-thinking enough to position their companies for the zero carbon economy.

It’s clear that there will be numerous firms operating in renewable technology, electric transportation and carbon capture who stand to benefit from the move to a zero-carbon economy. And yet we are currently in a situation of extraordinary frothiness in all green sectors as companies battle to establish themselves and investors seem willing to support even the most half-baked green strategies. We spoke above about the necessity of clear-eyed consideration of the risks and opportunities associated with investing in green technology. We would also urge investors to recognise that not all firms operating in apparently non-green industries ought to be excluded from portfolios as a matter of course. Some energy companies have aggressively embraced the transition to renewables, while there are other companies who responded positively to investor criticism of sustainability practices and have substantially improved their climate performance as a result.

To give examples of firms that have responded positively to some of the challenges of climate change, we might firstly cite Ikea, the world’s largest furniture retailer. Ikea had been criticised for the short (shelf) life of many of its products and the firm’s place in an economic system which prioritised novelty and waste over durability and restoration. In response, the company took a variety of steps to radically alter its business profile. It has meaningfully reduced its virgin wood consumption by switching to recyclable loading pallets, is moving to sell only energy-efficient LED lightbulbs, and has invested in a renewable power production to meet its total energy consumption. Ikea now owns more than three hundred wind turbines and has installed seven hundred thousand solar panels on its buildings.

Kimberly-Clark is one of the world’s largest personal care companies with brand leadership in many product areas including Cottonelle toilet paper, Kleenex facial tissue, Kotex tampons, and Huggies disposable diapers. It has received significant negative publicity in the face of its impact on the environment, with several NGOs calling it out for poor sustainability. In the face of this pressure, Kimberly-Clarke embarked on a number of environmental initiatives in recent years. These included reducing its water use by more than two million cubic meters, diverting 95 percent of its manufacturing waste from landfills by utilizing recycling technologies, reducing its GHG emissions by 18 percent, and sourcing all of its virgin wood fibre from certified sustainable forest providers.

Looking longer term at the opportunities presented by the impact of climate change, we might focus in on construction companies who will benefit from the radical reshaping of the built environment as populations move away from the sea and towards higher ground. There is also the necessity to rebuild in the wake of storm and wildfire damage. Similarly, we might see an increase in infectious diseases as a result of increased flooding and storms, meaning that healthcare companies stand to benefit. Both of these eventualities remain too far out to influence current portfolio construction, but we would urge investors to begin thinking along these (admittedly sobering, not to say depressing) lines sooner rather than later.

Finally, let us turn to CoalCo, a company whose future might have seemed bleak with the coming of the green revolution. In fact, the investment the company’s investment in research and development related to renewable technologies and minimising the carbon emissions of its activities meant that it saw an increase in cash and equivalents and intangibles on its balance sheet.

Chapter 5 Portfolio Management in a Warming World

Key Points

-

-

-

-

-

Investors should think of both opportunities and risks in the move to net zero.

-

Climate is now part of a suite of metrics applied to company valuation.

-

This is not only about equities: all asset classes will be impacted by climate change.

-

-

-

-

The next Part of the White Paper charts the rise of sustainable and ESG investment and the emerging Climate+ investment class. Many of these strategies seek to harness the opportunities inherent within the transition to net zero, but investors also need to recognise the full spectrum of risks that come from climate change and take steps to hedge these risks as best as possible. The key question we have sought to answer in the preceding chapters is whether, and to what extent, climate change will impact the earnings of the firms in which we invest, whether this be in a positive manner – opportunities in green technology, the economic viability of previously frozen areas, new and more efficient shipping lanes – or, and this will be the majority of cases, negatively – whether through falling GDP in many areas, the rendering of large areas uninhabitable due to extreme temperatures and consequent labour issues, or the cost of natural disasters and higher insurance fees.

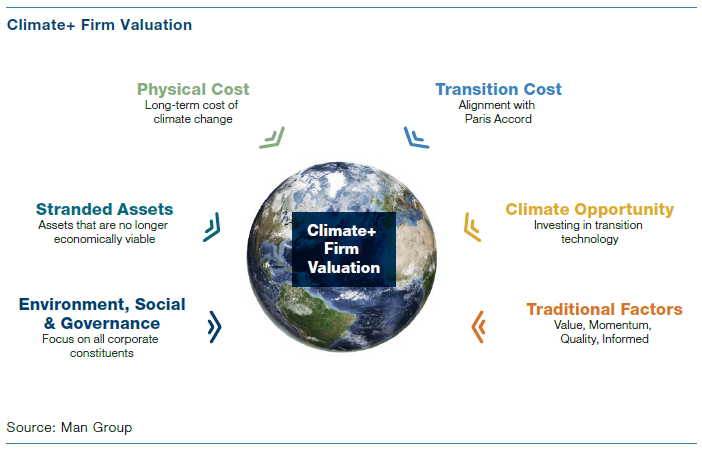

We view the climate change framework presented above as a kind of a puzzle – each model in it is trying to capture one aspect of the various ways in which a firm’s earnings will be impacted by a warming world. The graphic below shows how we combine these various elements, alongside more traditional factors and ESGrelated metrics to come up with a climate positive valuation of a firm.

One thing is clear when we move from traditional valuation models, through the newer ESG models, to climate models that have very little historical data to validate them: we are in new territory here and quantitative models rely on backtesting to generate consistent outputs. This means that we have to be very careful when calibrating and verifying climate models, making sure that those we use are based on strong fundamental hypotheses.

A warming world is a reality that must be accepted and negotiated by companies and their customers alike. Even in the best-case scenario of temperature rises being maintained at less than 1.5 degrees below pre-industrial levels, there will still be global heating that is unevenly distributed across the world. We are currently at 1.2 degrees of warming and are already seeing significant impacts from climate change in more frequent and deadly natural disasters. We must also remember that there is a lag between climate change and its impact, meaning that certain consequences will only be visible in the decades to come. Even with 1.5 degrees of warming, we will see some areas become almost uninhabitable, while others will see benefits accruing from the rise in temperatures. The whole structure of the global economic landscape will change, with demand falling in aggregate and precipitously in certain regions. Certain companies will thrive while others will find demand falls dramatically and assets they had valued on their balance sheets according to the rules of the old world order are suddenly worth far less than they expected, or even that they have become worthless. Innovation presents both opportunities and costs, with the likelihood that energy and mining firms in particular will face much higher risks and greater volatility of earnings as we move towards the century’s mid-point.

Asset owners need to think about how this radically altered landscape impacts the companies and securities in their portfolios. While we have largely focused on equity investors in this part of the paper, it’s clear that global heating will have implications across companies’ capital structures and across multiple asset classes. One only needs to look at the divide that has opened up in prices in Miami between properties at sea level and those above sea level. This kind of discrepancy will be played out in the coming years across all asset classes as it is increasingly recognised that a warmer world will ask questions of investors that they simply have not had to think about before. We hope that the ideas in this section of the paper are a useful starting place for those considering this vast and complex transition.

Part 3

Sustainable Investing and ESG

ESG has become the dominant movement in contemporary asset management.Climate is only one element of the E in ESG.

Is ESG a factor?

What securities are best from an environmental perspective?

Introduction