Link para o artigo original: https://www.man.com/insights/2026-credit-outlook

Where are the real pressure points in credit markets, and where can investors find opportunities in the year ahead?

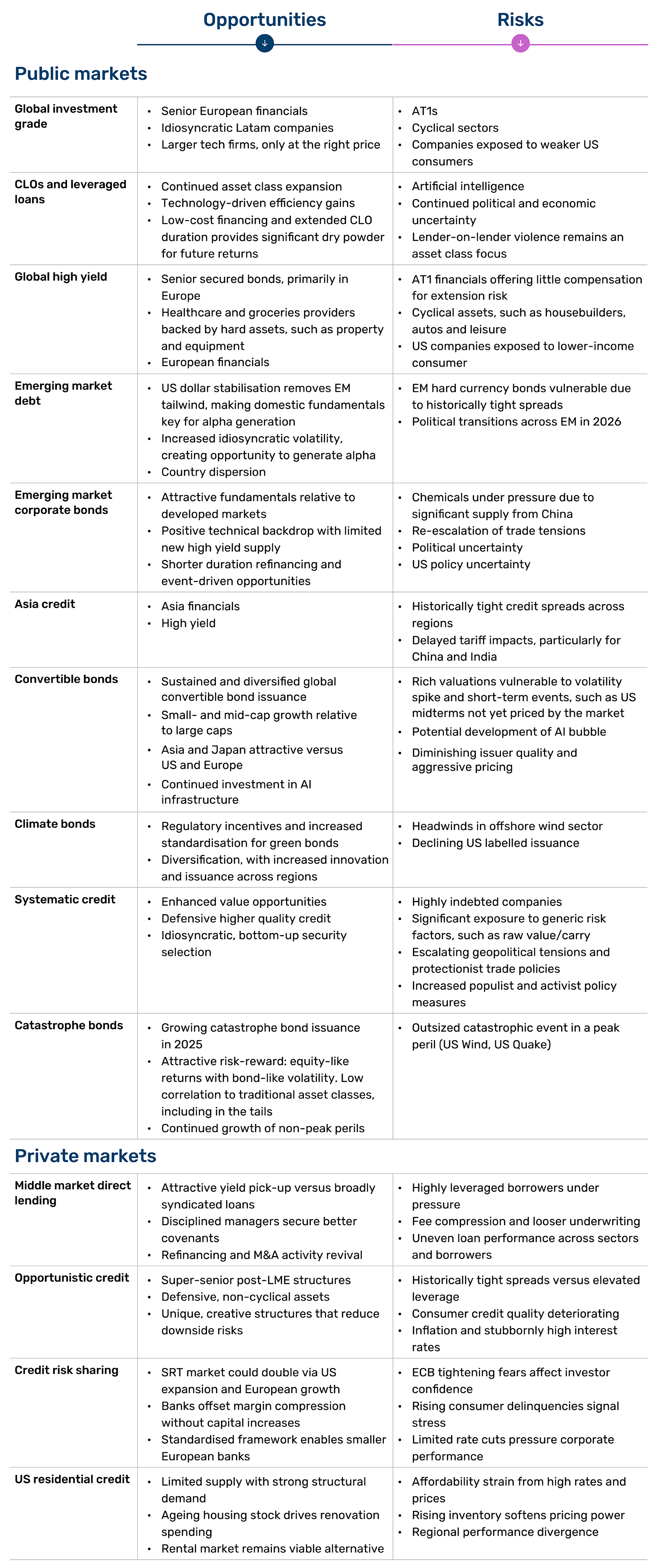

In focus

After a year dominated by geopolitical disruption and macroeconomic uncertainty, markets have recently fixated on a different concern: private credit. Recent high-profile defaults and fraud allegations have underscored the critical importance of distinguishing between credit market segments. Notably, the broadly syndicated loans at the heart of these cases operate with markedly different underwriting standards, documentation practices and lender oversight compared to core middle-market direct lending.

An equally important consideration is the timing of these events. Questionable structures typically emerge during economic booms, when underwriting discipline weakens and capital flows freely. They unravel during downturns, when the refinancing lifeline that sustained them dries up. Does this foreshadow broader stress in 2026?

Public credit markets have round-tripped

A glance at public credit markets, at least, would suggest not. Despite pronounced volatility throughout 2025, public credit markets have largely round-tripped – ending up close to where they began. Global high yield spreads currently stand at 304 basis points (bps) over government bonds, virtually unchanged from 305 bps on 1 January, despite widening around tariff uncertainty. Earnings multiples have exhibited a similar pattern: falling significantly in April before making a steady recovery. While spreads are not cheap across many areas of public credit, all-in yields remain healthy and fundamentals do not point to an imminent default cycle, barring a material deterioration in growth or employment.

Figure 1: Global high yield spreads are close to where they began

Problems loading this infographic? – Please click here

Source: Bloomberg, ICE BofA Indices – HW00 Index. Spreads are represented as option-adjusted spread for the ICE BofA Global High Yield Index over government bonds. As of 30 November 2025.

Figure 2: Earnings multiples have also made a steady recovery

Problems loading this infographic? – Please click here

Source: Bloomberg, as of 6 November 2025.

A weakening consumer

We see some cracks emerging, however. US real wage growth has slowed across all sectors except healthcare, eroding consumers’ purchasing power. The bigger risk we see, heading into 2026, is a slowdown in the wealth effect, compounded by persistent inflation. US consumers have enjoyed a substantial wealth boost driven primarily by home prices and equity markets. But given the froth in equity valuations and potential downward pressure on house prices in 2026, we expect consumers – particularly in the lower income deciles – to face continued pressure, likely resulting in slower consumption growth.

Figure 3: Slowing wage growth across sectors

Problems loading this infographic? – Please click here

Source: Bureau of Labor Statistics, employment by industry, monthly changes. Data as of August 2.025

Figure 4: Record levels of household wealth driven by home prices and equity ownership

Problems loading this infographic? – Please click here

Source: Bloomberg, based on data from 30 September 2019 to 30 June 2025. Wages based on ECI SA Index (Bureau of Labor Statistics Employment Cost Civilian Workforce QoQ SA); home prices based on FHFA (Fannie Mae) US House Price Index SA, S&P 500 based on SPX Index (price only) and inflation is US CPI Consumers index.

US regional banks remain under pressure

This environment has sharpened our view on financials. While we maintain a constructive outlook on European financials, the easy gains are gone after two years of strong performance and increasingly crowded positioning. The best opportunities have shifted to small- and mid-cap issuers, where valuations remain attractive and M&A activity could serve as a catalyst for outperformance.

By contrast, we remain cautious on US regional banks. Elevated exposure to commercial real estate presents a persistent headwind, compounded by potential weaknesses in broader loan portfolio underwriting. Notably, total criticised assets – loans or investments that regulators have determined to have a higher-than-normal risk of non-repayment or default – have been trending steadily upward and now sit well above 2020 levels, signalling deteriorating credit quality that warrants close monitoring. In general, the US is expensive and could be the epicentre of volatility should we see signs of slowing growth.

Figure 5: Rising problem loans in US banks

Problems loading this infographic? – Please click here

Source: Bloomberg, as of 30 September 2025.

What is our data telling us?

Our participation in significant risk transfers (SRTs) – which allow banks to reduce regulatory capital burdens and transfer some portion of credit risk to outside investors – provides an additional vantage point on credit market health. There, we have observed a modest uptick in defaults within leveraged finance, alongside increased pressure in the chemicals space. While risk premiums in industrial cyclical sectors have been relatively muted, intensifying competition from Chinese supply is creating new pressure points. Data also points to weakness in large-cap leveraged finance opportunities, as shown in Figure 6.1

What we find particularly striking amid these pressures is resilience in small- and medium-size enterprise lending. Specifically, European companies focused on domestic services have continued to operate strongly despite recent volatility.

Figure 6: Large corporate transactions are deteriorating more than SME and mid-corporates

Problems loading this infographic? – Please click here

Source: Man Group database. Based on Man Group’s proprietary analysis and portfolio experience. As of November 2025.

Positioning for 2026

Looking ahead to 2026, we are optimistic about absolute yield levels in credit markets, but continue to believe all-in spreads at index levels look less attractive. This environment favours unconstrained approaches that search for value, rather than broad market exposures, particularly as many sectors remain vulnerable to significant widening should growth slow.

We believe three strategies merit consideration. First, focus on niche areas of private credit such as SRTs and core middle-market direct lending, which may sidestep concerns now percolating in broader markets. Second, for investors keen to capitalise on volatility, an allocation to opportunistic credit – which should thrive as volatility grips public and private markets – makes sense at this juncture. Finally, long-short credit strategies offer another avenue to build in some downside protection at cheaper prices given lower implied volatility.

In brief

This information herein is being provided by GAMA Investimentos (“Distributor”), as the distributor of the website. The content of this document contains proprietary information about Man Investments AG (“Man”) . Neither part of this document nor the proprietary information of Man here may be (i) copied, photocopied or duplicated in any way by any means or (ii) distributed without Man’s prior written consent. Important disclosures are included throughout this documenand should be used for analysis. This document is not intended to be comprehensive or to contain all the information that the recipient may wish when analyzing Man and / or their respective managed or future managed products This material cannot be used as the basis for any investment decision. The recipient must rely exclusively on the constitutive documents of the any product and its own independent analysis. Although Gama and their affiliates believe that all information contained herein is accurate, neither makes any representations or guarantees as to the conclusion or needs of this information.

This information may contain forecasts statements that involve risks and uncertainties; actual results may differ materially from any expectations, projections or forecasts made or inferred in such forecasts statements. Therefore, recipients are cautioned not to place undue reliance on these forecasts statements. Projections and / or future values of unrealized investments will depend, among other factors, on future operating results, the value of assets and market conditions at the time of disposal, legal and contractual restrictions on transfer that may limit liquidity, any transaction costs and timing and form of sale, which may differ from the assumptions and circumstances on which current perspectives are based, and many of which are difficult to predict. Past performance is not indicative of future results. (if not okay to remove, please just remove reference to Man Fund).